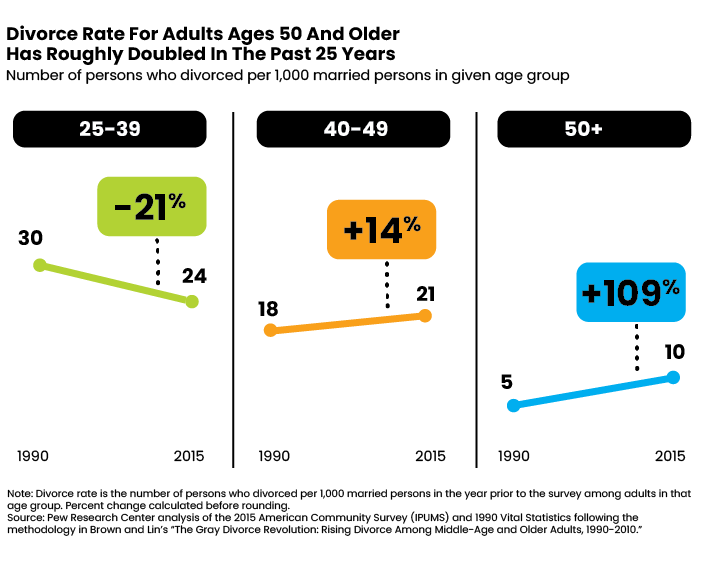

Although divorce rates overall have dropped in the last 30 years, many more people 50 and over are getting divorced today than in 1990. Older people cutting the knot can face very different and more complex financial issues than younger couples who part ways.

I recently spoke with advisor Kimberly Foss, who specializes in helping clients get through and plan how to manage their finances after a divorce, about recurring issues and new trends that she’s been seeing among older divorcing couples.

The No. 1 issue among women who are 65 and older is whether they’ll have enough money to sustain themselves going forward, says Foss, CFP, founder of Empyrion Wealth Management, with offices in Roseville, Calif., and New York City. “A lot of them were not the primary income producer and were raising the children mostly,” Foss notes.

But Foss and advisors like her are also seeing a new trend: Financially successful older women who remained in careers through their adult lives and are getting divorced. In some of those cases, the wives may be the ones paying support.

“I have a client who divorced in her later 50s. Her husband said he was not employable, and he was approaching 65. Because of his age, my client ended up paying $5,000 a month for five years. It was a second marriage for both of them, and they were only married for eight years,” Foss said.

“And you know, he did make really great money, but it was only in the last couple of years that he wasn’t working to the capacity that he was working before,” she continued. “He was a top salesperson making a quarter million dollars a year, but he was tapped out. And the judge ruled that he would get five grand a month for five years.”

Foss is working with another client, a doctor who is 60 and going through a contentious divorce. “She made most of the money in the family, but she is still very concerned about will she have enough? Will she have to pay child support or alimony?”

The doctor realized she could not navigate the financial complexities alone, and selected Foss after an internet search and interviewing three other advisors. The doctor already had a divorce attorney, but Foss helped her build out the rest of the team she needed, including a competent CPA who is providing input on how the assets should be split. The couple has to sell their house, so the doctor needs another place to live with her two teenage sons. Foss found a seasoned real estate agent and mortgage broker for the client to help her navigate the California housing market. Foss also aligned the doctor with a good psychologist, as well as a different one for her sons who specializes in children.

“The sad thing is, after 25 years plus of marriage, she basically saw through what he really is,” Foss said. “He went through the gamut of at least 10 different occupations over 25 years, everything from an insurance agent to an actor, and they moved around the country because of what he wanted to do and, for the sake of the kids, stayed together. She wants the divorce and I’m pretty sure he never thought that she would ever do that. And when she did it, of course, the real person in him came out. Basically, his financial lifeline is being cut off. And now it’s really getting ugly.”

Foss notes that advisors who work with divorcing clients need to discuss the emotion that is driving their clients’ decisions. “That’s the first thing I look at. If you’ve been with someone 25 or 30 years, you’re going to have some emotion. You have to address the deep-seated issues. A big one is whether they asked for the divorce or it was handed to them. If they asked for the divorce, they’ll still be emotional, but they’ll feel more in control. If it was handed to them, the fear factor has to be addressed.”

Many clients need to be able to accept and grieve the ending of the marriage – they need to honor the past but not “live” there, Foss says. That can be a difficult transition, she noted. People tend to dwell on what they could have done differently, and if they had children together, they most likely will still be intertwined for the rest of their lives. “You still are going to have grandkids; you’re still going to have maybe some family gatherings together.”

Most advisors are intuitive enough to address their client’s fears, Foss believes. “If you don’t address those real fears, she’s going to be paralyzed, and she won’t be able to make choices and make decisions.”

It’s important for advisors to think about how to be responsive and address the needs of such clients, but it’s also important for advisors to think about how they will get paid for their efforts. Advisors often structure contracts where they will get the assets to manage after the divorce is final, Foss notes. But what about all the time and effort that’s put into emotional support, coaching and finding other professionals before you have any assets to manage? Foss says some advisors set a retainer for those services while some charge on an hourly basis.

“You need to be very clear about how you charge,” she stresses. If you don’t charge for that upfront work and the assets don’t end up coming in, the advisor might not get paid.

Even when advisors charge an upfront retainer, they should specify that if the work becomes more time-consuming, or if there’s a change in scope, the retainer will be adjusted. Foss notes most divorcing clients she takes on are near the end of that process, although she’s handled divorce issues for existing clients, too. “In those cases, I do know there’s enough assets to hit my minimum and compensate me for the time I’m putting in before the divorce is settled.”

Dorothy Hinchcliff is publisher of Rethinking65. Please reach out to her at dhinchcliff@rethinking65.com with your ideas for contributions to www.rethinking65.com.

“And you know, he did make really great money, but it was only in the last couple of years that he wasn’t working to the capacity that he was working before,” she continued. “He was a top salesperson making a quarter million dollars a year, but he was tapped out. And the judge ruled that he would get five grand a month for five years.”

“And you know, he did make really great money, but it was only in the last couple of years that he wasn’t working to the capacity that he was working before,” she continued. “He was a top salesperson making a quarter million dollars a year, but he was tapped out. And the judge ruled that he would get five grand a month for five years.”