Retirement income security is in the eye of the beholder.

Retirement income security comes through allocations to a variety of guaranteed types of retirement income solutions such as Social Security, pensions and annuities.

• Social Security is guaranteed by the U.S. government.

• Pensions are backstopped by the Pension Benefit Guaranty Corp. and funding requirements.

• Annuities are backed by their respective insurance companies.

When guaranteed retirement-income solutions are either not enough, not available, or not required, investors look to the capital markets for nonguaranteed retirement-income solutions. Retirement income asset allocation to noninsurance or investment-based solutions provides retirees a complementary and diversified approach to the retirement income security that Social Security, insurance, and other guaranteed solutions aim to provide.

Given the continued expansion of workplace retirement plans, IRAs and other retirement accounts, investment and hybrid insurance types of solutions have become a growing and more critical component of overall retirement- income security. While dynamic capital markets impact the explicit account values of investments, changing market valuations and interest rates also affect the retirement income-value and decisions of all guaranteed or non-guaranteed types of investment solutions.

Fixed income funds can have a BIGG impact on retirement income security.

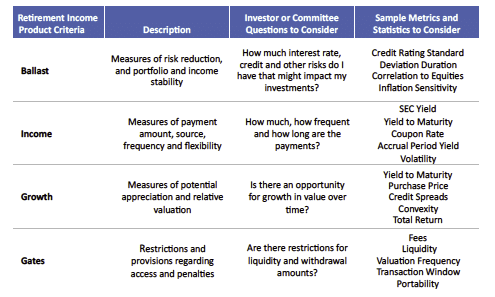

Along with an organized and documented process for retirement income solutions, fiduciaries might have a BIGG impact on investors’ on overall retirement-income security if they focus on four important qualities of retirement income products: ballast, income, growth and gates. These simple criteria allow for a product-neutral analysis of a group of metrics to consider when evaluating all nonguaranteed and guaranteed types of retirement income products.

Within the large universe of nonguaranteed, investment-based retirement-income products, fixed income mutual funds, exchange-traded funds, collective investment trusts and separately managed accounts are commonly used and widely available tools for retirement income security. There are a variety of fixed income styles and approaches to choose from, and many fixed income funds play a multipurpose role in retirement income security.

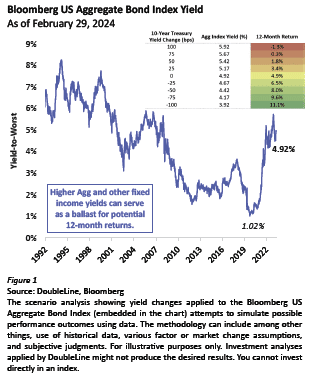

The repricing higher of yields can potentially act as a cushion should U.S. Treasury rates move higher.

Fixed income investments typically provide regular, stable income through interest payments, which can offer a predictable cash flow. This stability is particularly valuable in times of market volatility or economic downturn, as it can help offset losses from other more volatile investments like stocks. As an example, today’s higher yields across fixed income can potentially act as an even better ballast or cushion for retirement income investors should Treasury rates move higher. (Figure 1)

Income

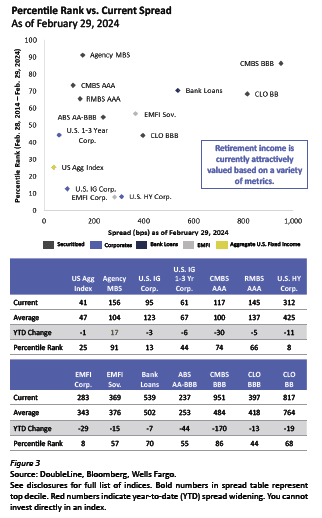

Investment grade credit broadly could offer mid- to high single digit yields.

There are much higher overall rates now available across fixed income, and this may help retirees generate higher levels of investment income. As an example, investment grade credit broadly could offer retirement income investors yields in the mid to high single digits, and lower-rated credit could offer yields in the high single digits to midteens. (Figure 2)

Growth

Credit spreads for parts of fixed income are attractive, with the potential for price

appreciation.

Additionally, there are valuation opportunities in parts of fixed income that provide the potential for capital appreciation not seen in decades. Alongside attractive valuations, many parts of fixed income are trading at discounted dollar prices, with the potential for price appreciation. (Figure 3)

Gates

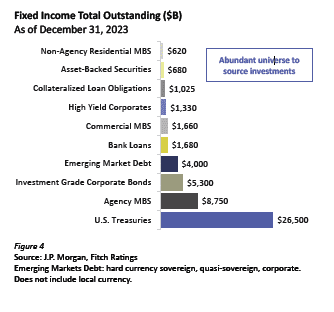

Liquidity and bond issuance remains at all- time highs across areas of high-quality fixed income.

Lastly, some retirement income products will have restrictions or provisions regarding access and other penalties. Many high- quality fixed-income strategies do not have these types of restrictions, although frequent trading is highly discouraged and not allowed. Traditional mutual funds and exchange-traded funds can meet redemption and contribution requests daily, and calm nervous investors who prefer to know that their capital markets retirement-income accounts are easily accessible. Continued growth and liquidity in overall fixed-income markets will support additional efficiency, trading and diversification for retirement income investors. (Figure 4)

Daniel Long, QPFC, AIF® is a Relationship Manager for DoubleLine. He joined DoubleLine in 2018 and responsible for client relationship management for the firm’s retirement plan clients. His responsibilities have involved working with plan sponsors, consultants and service providers to successfully operate retirement plans for employees. Mr. Long has more than two decades of experience in the retirement plan industry. Prior to DoubleLine, he has held retirement solutions roles with Goldman Sachs, RSM McGladrey, Transamerica, Neuberger Berman, ADP and PaineWebber. Mr. Long has been a speaker at various industry conferences and currently serves on a local not-for-profit board with ASPPA. He holds a BS in Business Management from Cornell University and an MBA from Northwestern Kellogg Graduate School of Management. Mr. Long is a Qualified Plan Financial Consultant.

Phil Gioia, CFA, is a Product Specialist, Macro Asset Allocation, for DoubleLine. He joined DoubleLine in 2018. He is a member of the Macro Asset Allocation team, on which he serves as a Product Specialist. In this capacity, Mr. Gioia is responsible for various aspects of DoubleLine product marketing, investment strategy updates, portfolio communications and competitive analysis, with a focus on DoubleLine’s Securitized Product strategies. He is also responsible for producing market commentary and dedicated strategy content. Prior to DoubleLine, Mr. Gioia was an Investment Product Manager for Fidelity Investments. He holds a B.S. in Financial Management and Business Administration with a minor in Accounting from Salve Regina University, and he earned a certification for the Applied Data Science Program from the Massachusetts Institute of Technology. Mr. Gioia is a CFA® charterholder and holds the FINRA Series 7 and 63 licenses.