Today, many advisors are finding themselves at a crossroads. With a new administration and the Federal Reserve pausing on a rate-cutting cycle, the world of financial markets continues to shift. But here is a question many advisors are asking: Is it time to move away from the comfort of Treasury bills and seek higher returns elsewhere?

In recent years, a record amount of cash has been sitting on the sidelines. The appeal of money market funds and short-term treasuries has increased as the Fed raised interest rates, offering investors what Harbor Capital Advisors believes to be safer and attractive yields. By the end of 2024, total net assets in U.S. money market funds had reached an all-time high of $6.8 trillion1 but history tells us these cash-alternative vehicles may not stay there forever.

As the Fed eases rates, the flow of capital has followed a recognizable pattern. Past rate-cutting cycles suggest net inflows into cash alternative vehicles plateau before tapering off, with outflows typically beginning within three to six months of the Fed’s first cut. If history were to repeat itself, we could see between $929 billion and $1.4 trillion2 in excess capital to reallocate elsewhere in the market. Therefore, we believe it’s important to react quickly to the changing rate environments to potentially avoid missing out on opportunities in equities, corporate bonds and more. By proactively guiding your clients through this shift with strategic diversification, you can help position them for attractive outcomes.

Why Staying in Cash-Alternative Vehicles Could Cost You

Traditionally, bond yields have declined following rate cuts, until the current rate-cutting cycle, which has actually seen a rise. Inflation expectations can be a potential driver of this current dynamic as it could put a pause on any further rate cuts. Also, there is a new administration to think about for potential market and economic implications, making it important for advisors to remain vigilant when assessing their bond allocations.

Equities, as represented by the S&P 500, have historically delivered the highest returns over these three-year periods, with high-yield bonds delivering similar returns as the S&P 500 Index.

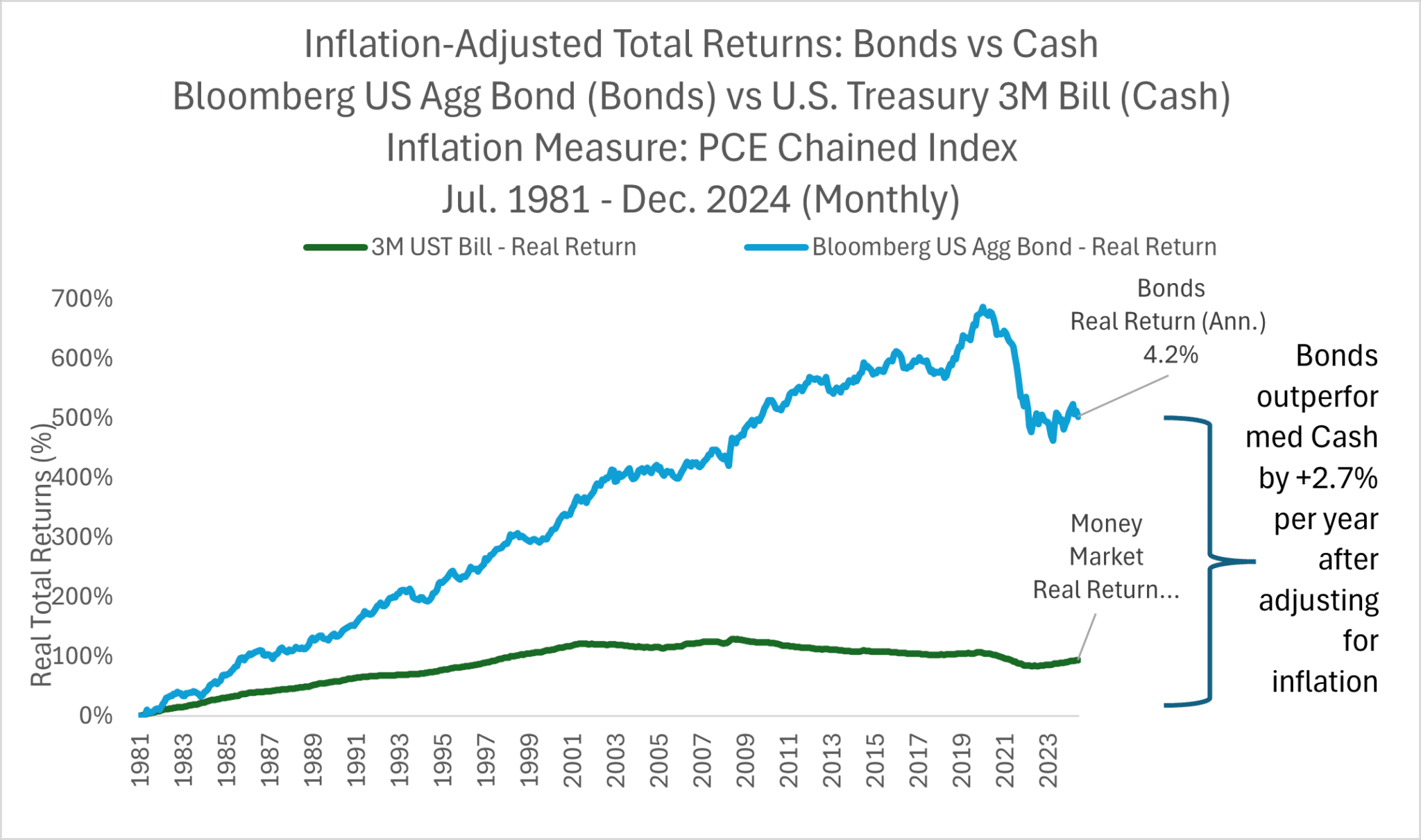

Investors often hear the phrase “cash is trash,” but history tells a different story. The chart below shows that since 1981, cash, as proxied by 3-month Treasury Bill, has outpaced inflation, delivering a 1.5% inflation-adjusted annualized return. While surprising, this reinforces the importance of liquidity for short-term needs. However, bonds have been the stronger performer. Over the same period, bonds delivered a 4.2% excess return, outperforming cash by an additional 2.7%.

Source: Morningstar Direct & Federal Reserve Bank of St. Louis. 1Personal Consumption Expenditures: Chain-Type Price Index 2017=100, Seasonally Adjusted. Performance data shown represents past performance and is no guarantee of future results.

This offers a compelling advantage in terms of both nominal and real returns for those investors who opted for an investment in bonds over cash-alternative vehicles. With inflation likely to remain high, advisors should consider guiding clients toward a balanced approach, keeping necessary cash reserves and having surplus cash positioned in investments like core bonds.

The Rise of Active Bond ETFs

Investors have also been moving into longer-term treasuries, multisector (particularly those actively managed) and credit-focused funds. The preference for active bond ETFs over mutual funds has accelerated. Though they represent just 4% of total net assets, their organic growth rate has soared to 77% since 20193. Bond ETFs appear to be the go-to for fixed income exposure, and advisors have been integrating them into client portfolios accordingly.

We believe fixed-income managers seek to focus on consistency over returns. Instead of reaching for yield or taking large bets, they often rely on disciplined bottom-up security selection in seeking to generate alpha. When we looked at core plus funds overall, we felt that successful managers didn’t take on excess market risk. In looking at our data, we viewed that their beta aligned with peers and the index. We also believe that managers across core plus funds assumed slightly less credit risk while maintaining about the same interest rate risk. So, rather than relying on aggressive credit or rate bets, we think they primarily delivered outperformance through security selection.

Systematic Investing: The Data-Driven Edge in Fixed Income

Unlike passive “smart beta” approaches, active systematic strategies use proprietary models and advanced technology to uncover relationships between data and performance, optimizing portfolio construction. With approximately 15,000 securities in the U.S. fixed income universe, systematic investing offers advisors a powerful advantage, particularly in credit markets like high yield. By merging data-driven insights with active management expertise, these strategies help enhance portfolio construction and seek to improve return potential.

The bottom line is that while bonds remain important, today’s market calls for a broader approach to diversification. By incorporating active fixed income strategies, systematic investing, and alternative asset classes, advisors have the potential to better position their clients for attractive long-term outcomes in an evolving financial world.

Elizabeth Laprade, CFA, is a senior investment research and strategy analyst with Harbor Capital Advisors.

1.2,3Morningstar Direct, March 2025; Universe is all U.S. Taxable Bond categories across both Electronically Traded Funds (ETFs) and Open-End Investment Funds (Mutual Funds) that are available in Morningstar Direct. Active is defined as funds not classified as an Index fund, while Passive are those that do qualify as an Index fund according to Morningstar Direct The views expressed herein may not be reflective of current opinions, are subject to change without prior notice. This material is for informational and illustrative purposes only.