Although both men and women can face a “financial vortex” of competing responsibilities during their working years that can hinder their retirement savings efforts, women are more impacted by these obstacles, according to a new study from Goldman Sachs Asset Management.

In addition to being more likely to take time out of the workforce to provide childcare and eldercare, a greater percentage of women also reported that their ability to save for retirement was impacted by too many monthly financial expenses, financial hardships (including home repairs), saving for college (for themselves and others), and paying down existing loans and credit card debt.

Some key findings from Goldman’s Retirement Survey and Insights Report, “Navigating the Financial Vortex: Women & Retirement Security”:

More women (50%) than men (35%) said their retirement savings are behind schedule; 24% of women and 14% of men said they are “very behind schedule.”

Fewer women (47%) than men (64%) said they feel on track or ahead of schedule for retirement.

Among working women, only 14% said they were “very confident” they’d achieve their retirement goals, compared with 27% of working men. More women (33%) than men (19%) reported concern that they won’t be able to meet their retirement goals.

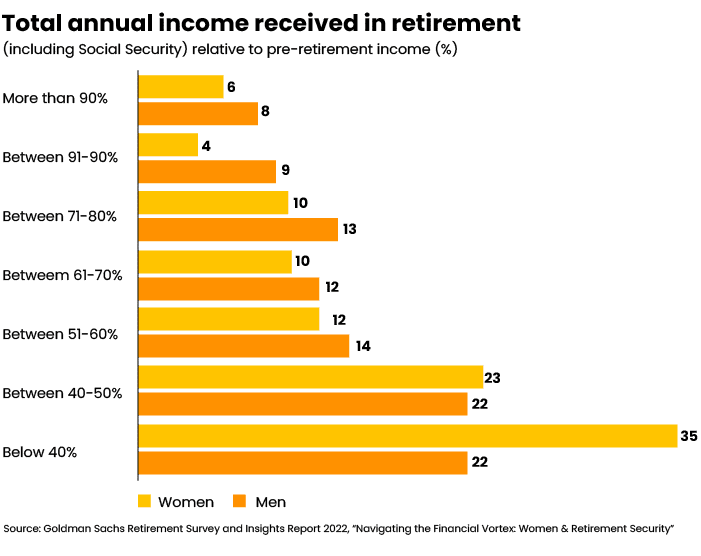

Among retired women, 58% reported receiving 50% or less of their pre-retirement income, including Social Security, compared with 44% of men. Only 20% of women reached 70% of their pre-retirement income, compared to 30% of men.

The top concerns that working women reported in preparing for retirement were “having sufficient savings” (51%), “inflation” and “leaving a steady paycheck” (48% each) and “healthcare needs” (41%). In comparison, just 38% of men reported being concerned about “leaving a steady paycheck.”

More women forced to retire earlier

The study also found a notable difference in when and why men and women retire. While 50% of men said they retired earlier than planned, this percentage was much higher (61%) for women. The 66% of women who retired for reasons outside their control often cited health reasons (29%). Other common reasons: to take care of family (16%) or their job was no longer available (15%). Only 15% of women, compared with 25% of men, said they retired because their savings were sufficient to fund their retirement.

Stepping out of the workforce to care for children or elderly family members can significantly impact retirement savings. Two four-year gaps (one mid-career and one later) can reduce retirement savings up to 35%, the Goldman report noted.

Goldman’s model assumes the retirement saver contributes 8% of their salary with 5% employer contributions from age 25 to age 65, with a 6% annualized portfolio return. It also assumes the employee leaves the workforce for caregiving responsibilities from age 31 to 34 and again from age 62 to 65, resulting in an early retirement.

“Women more often than men are forced to work part-time, spend time out of the workforce to care for young children and elderly family members, and juggle other financial priorities during their careers,” Candice Tse, global head of Strategic Advisory Solutions at Goldman Sachs Asset Management, said in a news release. “This can make their journey to retirement more difficult and incredibly personal.”

The report noted, too, that American women on average live three years longer than men, citing data from the Social Security Administration.

Winging it

Goldman’s study also examined the emotional toll of managing one’s finances, an approach embraced by 69% of the women and 63% of the men surveyed. Among the women going it alone, 63% reported stress or anxiety, compared to 52% of men, and more women (31%) than men (20%) called it “very stressful.”

“These statistics reveal the deeply human nature of the decisions that at times require women to prioritize family, caregiving or health-related issues over their financial futures,” said Jennifer Huisking, vice president at Goldman Sachs Personal Financial Management in the release. “For these women, financial confidence comes from having clarity about their financial resources and acting where they have control. A financial advisor can help them take a full inventory of what they earn, spend, save and owe, and create a plan to define their priorities and move towards the outcomes they seek.”

The topics for which women responded that they wanted guidance or advice included understanding how long savings would last (34%), how to adjust retirement saving if it’s not on track (33%), retirement saving strategy (e.g., how much to save) (32%) and generating retirement income (32%).

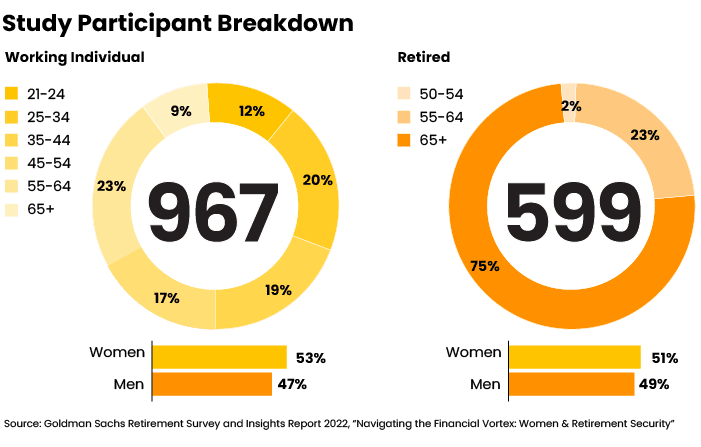

Goldman’s study surveyed 1,566 individuals in July and August 2022, including 967 working individuals across generations (including baby boomers) and 599 retired individuals age 50 to 75.