DoubleLine Takes a Look at Agency MBS Market Heading Into 2025

In a new research paper, DoubleLine's Kunal Patel, CFA, and Analyst Alex Shvartser share their outlook on the Agency mortgage-backed securities (MBS) market for the new year, reviewing past performance and future possibilities under different economic scenarios.

As 2025 kicks off, DoubleLine presents its assessment of the Agency mortgage-backed securities (MBS) market and provides an update on where the asset class has been and where it could be headed. As DoubleLine has highlighted in the past (in May 2023 and October 2023 pieces) the Agency MBS market has experienced elevated spreads relative to history over the past few years. While excess returns of Agency MBS have been strong since the last updates – 163 basis points (bps) from May 2023 through December 2024 and 174 bps from October 2023 through December 2024 – there is more room for mortgages to rally.

Executive Summary:

Since the beginning of the Federal Reserve’s hiking cycle in 2022, and resulting higher interest rates and interest rate volatility, Agency MBS have experienced some of their lowest returns in history.

The factors that have been headwinds for Agency MBS over the last few years could turn into tailwinds, and there are reasons for optimism about the potential for strong future Agency MBS performance.

While the Agency MBS market still sits at relatively elevated spread levels, there are green shoots emerging that could tighten spreads in many potential market and economic environments.

Agency MBS represent significant value over other spread products such as corporate bonds.

It was the “just okay” of times, it was the worst of times…

With apologies to Charles Dickens, it has become pretty much a cliché to note that the Agency MBS market has experienced a very challenging period over the last few years. There have been several meaningful headwinds in that period:

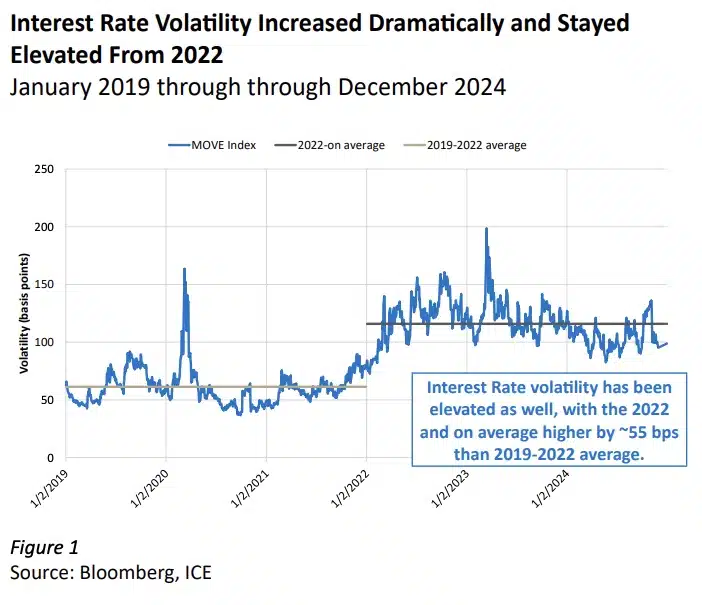

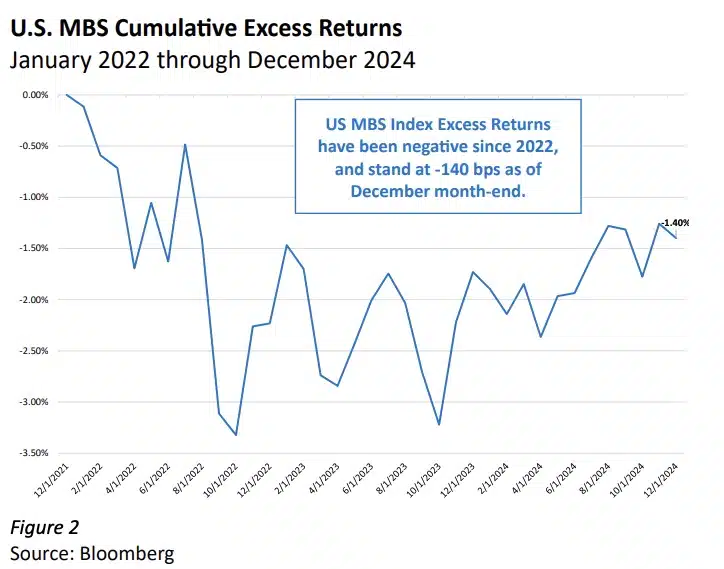

Rate Volatility: The fastest Fed hiking cycle in history started in 2022, and it dramatically increased rate volatility and drove Agency MBS spreads to historically wide levels. Because Agency MBS holders are short an embedded prepayment option, and that option can be very sensitive to interest rates, increased interest-rate volatility caused Agency MBS securities to exhibit significantly negative excess returns. Average interest-rate volatility between 2022 and December 2024 was 55 bps higher than the average between 2019 and 2022. Excess returns since 2022 stood at negative 140 bps as of December 2024. (Figures 1 and 2)

Quantitative Tightening: The Fed ballooned its ownership of Agency MBS in response to the COVID-19 crisis, with holdings peaking at around $2.7 trillion in 2022. At the same time the Fed was hiking interest rates, it started to roll off its Agency MBS holdings via the Fed’s quantitative tightening policy, and its holdings have declined to approximately $2.2 trillion via paydowns as of Dec. 25, 2024.

Reduced Bank Participation: Banks, a traditional buyer of Agency MBS, have been going through a period of earnings volatility, higher funding costs, deteriorating balance sheets and increased likelihood of more stringent regulation after the expected adoption of Basel III Endgame measures.

2023 Bank Failures: The collapse of Silicon Valley Bank and Signature Bank resulted in large liquidations of retained Agency MBS portfolios by the Federal Deposit Insurance Corp. over most of 2023. While this was a headwind to the market initially, it ultimately had the effect of validating the liquidity available in both pass-through mortgages and the collateralized mortgage obligation (CMO) subsector of Agency MBS, thereby bringing in a wider investor base.

Inverted U.S. Treasury Curve: An inverted curve results in more securities with negative carry, inhibits CMO creation, disincentivizes banks to add Agency MBS and worsens model convexity as lower, versus higher, forward rates lead to higher projected prepayments due to more borrowers being “in the money” on their mortgages.

Very Low Realized Prepayments: Turnover – the natural prepayment behavior due to life events – and refinancing activity dramatically slowed down in the face of much higher primary mortgage rates, effectively locking borrowers into their existing mortgages.

Where Do We Go From Here?

As 2025 begins, there are reasons to be cautiously optimistic about Agency MBS performance. The economy exhibits signs of both strength and weakness, with a range of predictions from recession to soft landing being supported by various data prints. Currently, Agency MBS are priced at attractive levels in many reasonable scenarios that could take place in the broader economy.

One can think of the primary mortgage rate as the 10-year Treasury yield plus the cost that secondary mortgage investors demand for the additional prepayment and volatility risk over the 10-year Treasury bond (current coupon spread) in addition to the cost of originating the mortgage (known as the primary- secondary spread). As of this writing, the 10-year yield was 4.57%, the current coupon spread over the 10-year yield was 1.26%, and the primary-secondary spread was approximately 1.0%, adding up to a primary mortgage rate of about 6.83%. For secondary mortgage market investors, a mortgage rate rally implies either a fall in yields, such as that of the 10-year Treasury, or a tightening of the spread to Treasuries, which for new-issue mortgages would mean a tightening of the current coupon spread. In regard to the 10-year Treasury yield, any weakness in the economy should result in falling Treasury yields along the curve which should then be reflected in a broad Agency MBS rally, with longer-duration structures benefiting the most. If rates stay where they currently are, we think Agency MBS bonds can offer advantageous carry relative to other spread products.

Since the November elections, rate volatility has declined, and DoubleLine’s expectation is that it will continue to fall as both Fed policy and the post-pandemic economy continues to find their steady-state configurations. While current coupon spreads remain elevated relative to history – the average spread over the 10-year Treasury yield is less than 100 bps since 2008 – any reduction in interest rate volatility should translate to lower current-coupon spreads. This should result in an Agency MBS rally, especially in higher coupon mortgages most sensitive to such changes. A tightening current-coupon spread tends to be a tide that lifts all boats, and mortgages in the middle and lower coupon ranges should perform well in this scenario, as demand for those mortgages would likely remain strong.

Of course, if rates sell off meaningfully and yields rise, or volatility increases and current coupon spread widens, Agency MBS will likely underperform. Perhaps the biggest risk to realizing such a scenario is the Fed restarting an interest-rate hiking cycle in the face of re-accelerating inflation. While this is by no means DoubleLine’s base case, it does represent the most direct risk to Agency MBS.

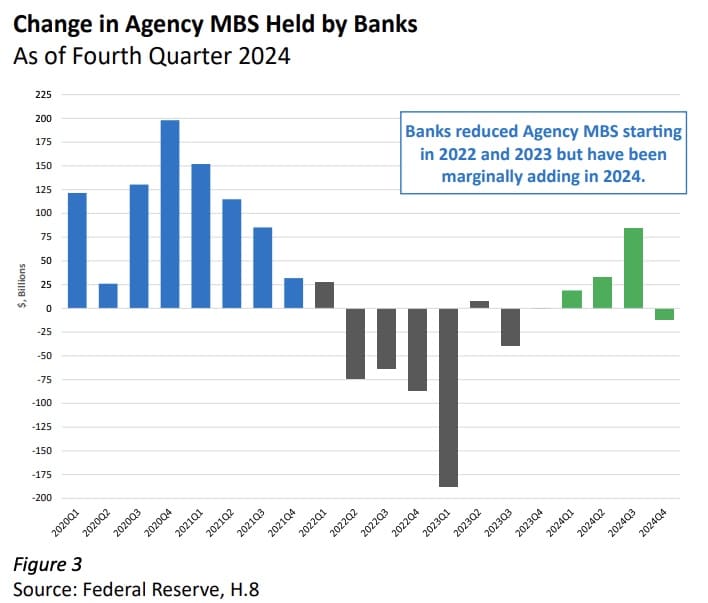

The demand for Agency MBS is slowly yet surely turning from a headwind to a tailwind, with green sprouts emerging as both banks (Figure 3) and overseas investors start to increase their holdings after a lengthy period of reduction. Money managers and other investors continue to maintain robust Agency MBS demand, and additional inflows will drive spreads tighter in the sector. DoubleLine does not expect the Fed to be a meaningful participant in the market going forward, and the Fed should continue an orderly winding down of its Agency MBS portfolio, which has already been priced in by the market.

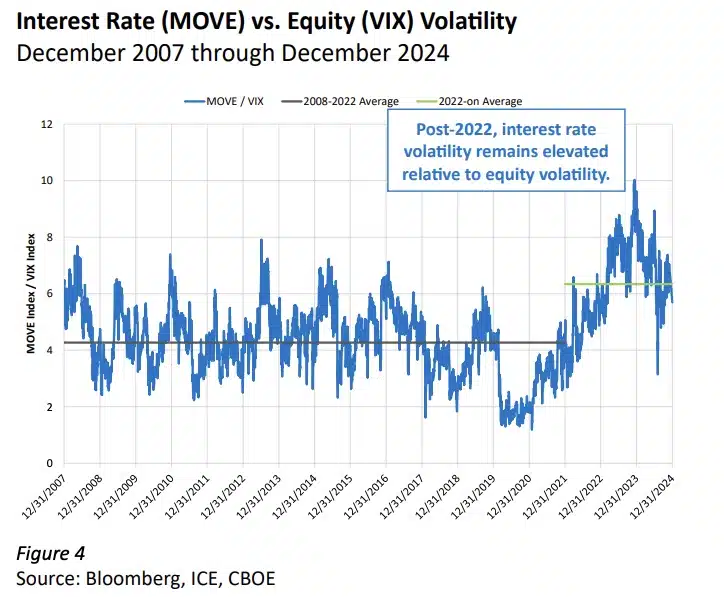

Relative to corporate bonds, Agency MBS remain cheap. While both asset classes are affected by volatility, they respond to different types of pressure. As we note above, Agency MBS are sensitive to interest rate volatility. In contrast, equity volatility is more relevant to corporate bonds. In fact, the relationship between interest rate and equity volatility – proxied by the ratio of the ICE BofA MOVE Index to the Volatility Index (VIX) – has been elevated since 2022, with the 2022-December 2024 average at 6.3 versus a 4.3 average between 2008 and 2022. (Figure 4)

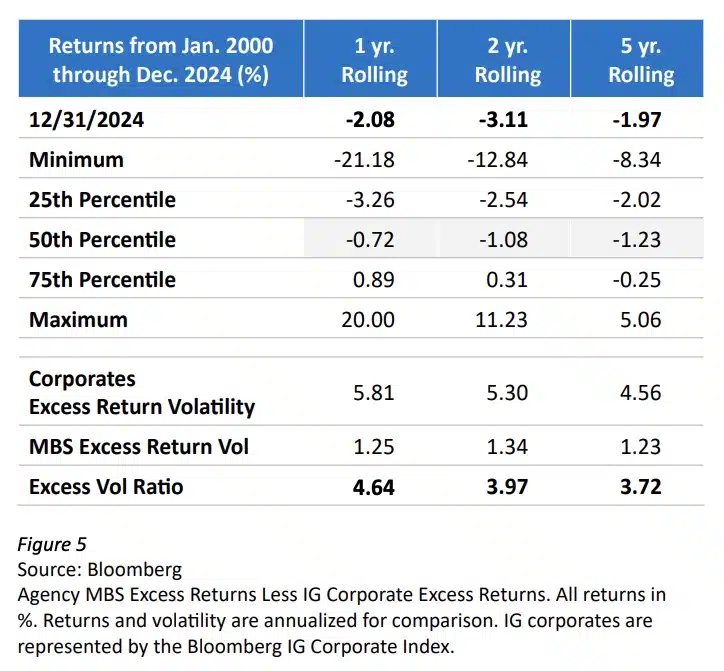

This dynamic explains why mortgages have underperformed corporate bonds in terms of excess return over the last few years relative to their historical norms. In Figure 5, we present the rolling excess return on a one-, two- and five-year basis of Agency MBS minus the excess return of investment grade (IG) corporate bonds, as measured by the Bloomberg US Corporate Index. We consider a long history of returns here, going back to 2000. Agency MBS underperform corporates because they exhibit significantly lower excess return volatility. However, compared to median performance, current levels of underperformance are extreme.

Volatility patterns should ultimately revert to the mean – either interest rate volatility will decline or equity volatility will increase (DoubleLine believes that the former is more likely). As that happens, Agency MBS and IG corporate bonds should also mean revert in terms of their performance. While the appeal of IG corporates to all-in yield investors is understandable, DoubleLine believes that exposure to Agency MBS products with virtually no credit risk, some of which offers nominal spreads of 120 bps to 150 bps, should not be overlooked.

Disclaimers

Mr. Patel joined DoubleLine in 2016 as a Mortgage Trader specializing in Agency RMBS and was later promoted to Portfolio Manager in 2021. Prior to DoubleLine, he worked as a Managing Director responsible for CMO and specified pool trading at Cantor Fitzgerald. Prior to that, Mr. Patel worked as a CMO, ARMs and Specified Pool Trader and Deal Structurer at Morgan Stanley, BNP Paribas and RBS Greenwich Capital. He holds a B.A. in Economics from Cornell University. Mr. Patel is a CFA® charterholder

Mr. Shvartser joined DoubleLine in 2020 as an Analyst on the Agency RMBS team. Prior to DoubleLine, he was with TCW as a Senior Vice President, Investment Analytics. Prior to TCW, Mr. Shvartser was a Quantitative Analyst at ICE Canyon. Prior to ICE Canyon, he was Vice President at BlackRock in the Financial Modeling Group. Mr. Shvartser holds a B.S. in Electrical Engineering from the California Institute of Technology and an M.S. in Mathematics in Finance from New York University.

Issue selection processes and tools illustrated throughout this presentation are samples and may be modified periodically. These are not the only tools used by the investment teams, are extremely sophisticated, may not always produce the intended results and are not intended for use by non-professionals.Yield to maturity (YTM) does not represent return. YTM provides a summary measurement of an investment’s cash flows, including principal received at maturity based on a given price. Actual yields may fluctuate due to a number of factors such as the holding period, changes in reinvestment rates as cash flows are received and redeployed, receipt of timely income and principal payments. DoubleLine views YTM as a characteristic of a portfolio of holdings often used, along with other risk measures such as duration and spread, to determine the relative attractiveness of an investment.DoubleLine has no obligation to provide revised assessments in the event of changed circumstances. While we have gathered this information from sources believed to be reliable, DoubleLine cannot guarantee the accuracy of the information provided. Securities discussed are not recommendations and are presented as examples of issue selection or portfolio management processes. They have been picked for comparison or illustration purposes only. No security presented within is either offered for sale or purchase. DoubleLine reserves the right to change its investment perspective and outlook without notice as market conditions dictate or as additional information becomes available. This material may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to a client’s account, or market or regulatory developments.Investment strategies may not achieve the desired results due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors. The views and forecasts expressed in this material are as of the date indicated, are subject to change without notice, may not come to pass and do not represent a recommendation or offer of any particular security, strategy, or investment. All investments involve risks. Please request a copy of DoubleLine’s Form ADV Part 2A to review the material risks involved in DoubleLine’s strategies. Past performance is no guarantee of future results.

DoubleLine Group is not an investment adviser registered with the Securities and Exchange Commission (SEC).

")