Macro Environment Argues for Near-term Equity Market Volatility

September data reveals a return to net optimism in sentiment, which, if maintained, has historically been beneficial for global equities. (Ned Davis Research)

Some of the timelier data we follow, particularly survey-based data, is giving some early signs that downside momentum in the global economy is stabilizing.

Global recession risk also remains low.

But our indicators show that markets may need to see a little more evidence of macro improvement before getting bullish

In our second half global economic outlook publication published in June, we anticipated a more moderate outlook in the latter half of the year. As anticipated, our outlook has come into fruition, with various indicators, including PMIs and LEIs, showing weaker momentum starting in the early summer.

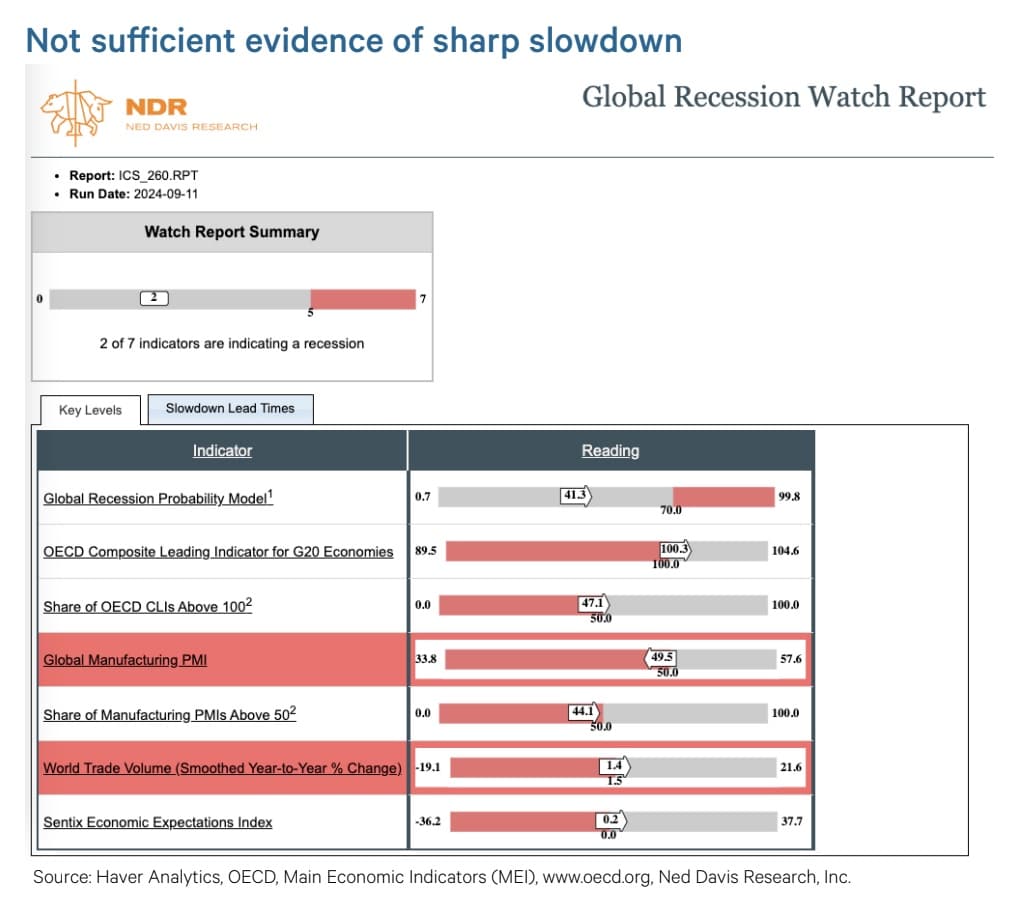

But some of the timelier data we follow, particularly survey-based data, is giving some early signs this downside momentum in the global economy is stabilizing. Moreover, our Global Recession Watch Reports, which aim to identify much sharper slowdowns in global economic activity, continue to show little risk. This is important because these down cycles are more than often associated with cyclical bear markets in equities.

While all of this is constructive news, our macroeconomic indicators calling equities suggest that markets need to see a little more evidence of improvement before getting bullish. This suggests choppiness in equities in the near-term, but in the context of a continuation of the cyclical bull market in equities.

Nascent improvement

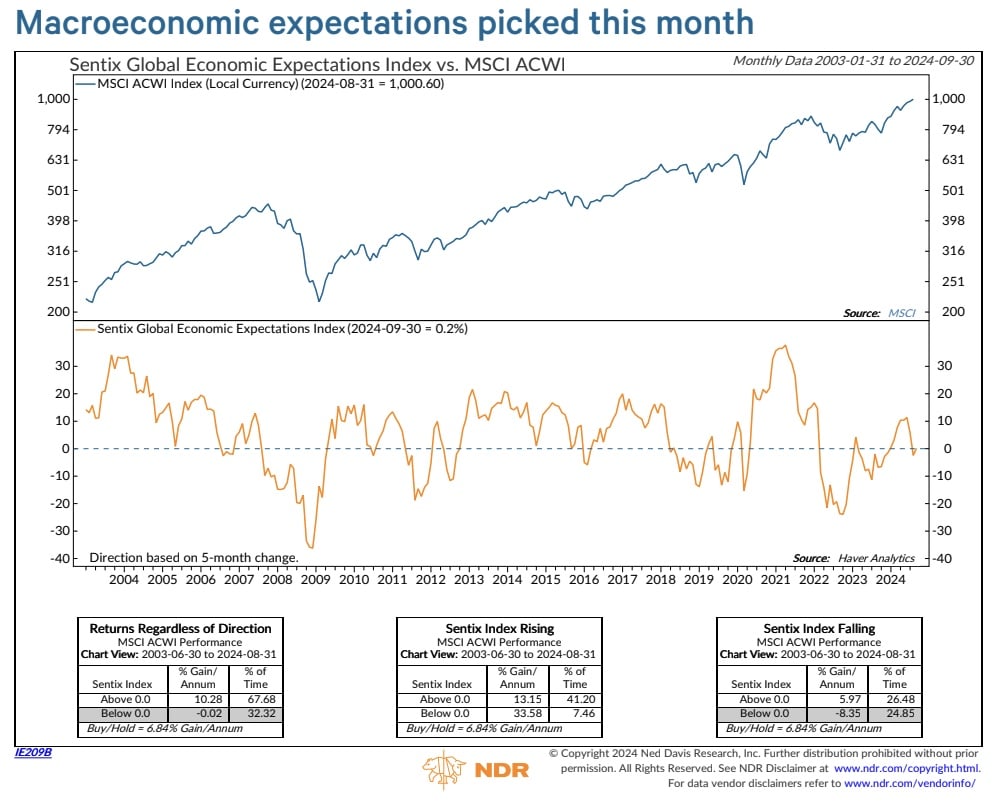

The Sentix global macroeconomic expectations index, an investor sentiment survey of future economic conditions, has had a great track record in identifying global macroeconomic cycles with a lead time.

As shown in the chart above, the index peaked in June, eventually moving into net

pessimism territory in August, a negative condition for global equities.

However, data for September saw sentiment jump back into net optimism. If sustained, this has historically been positive for global equities.

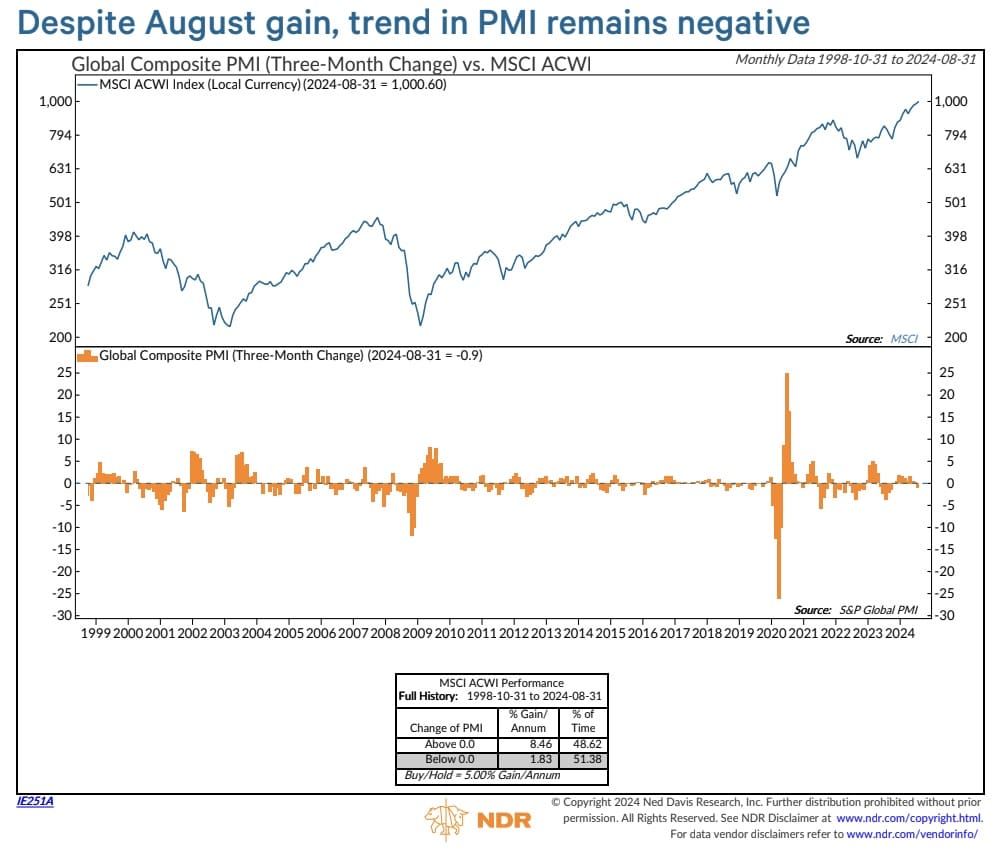

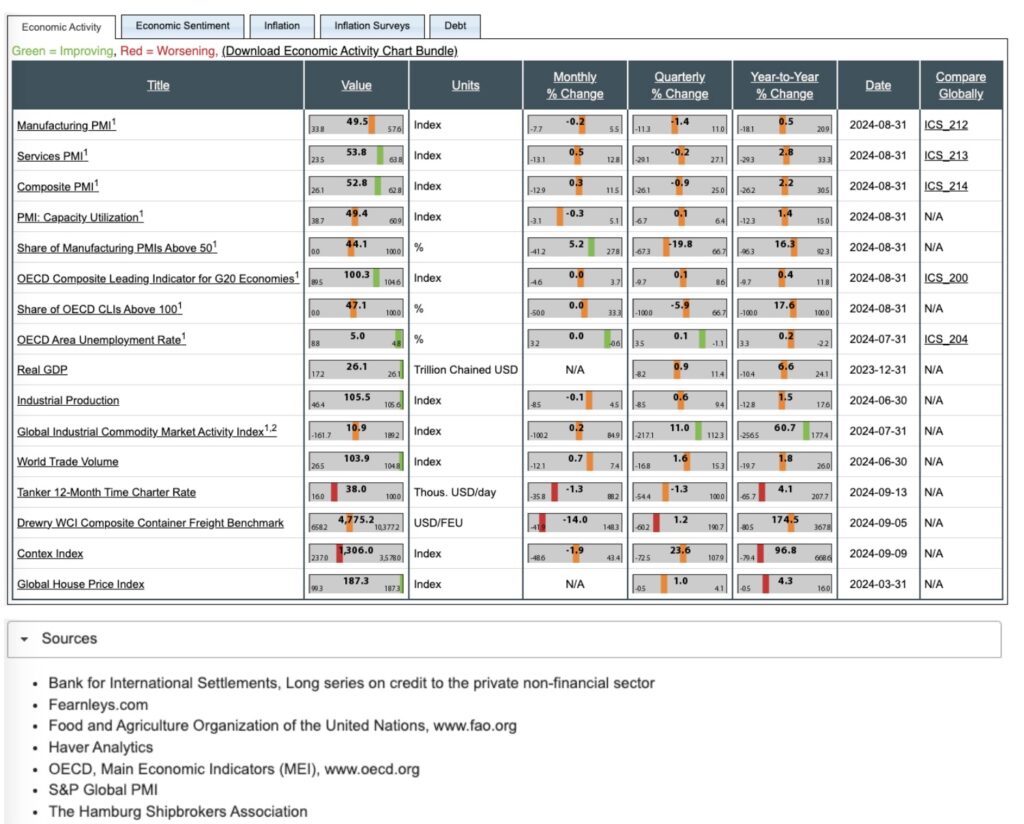

The August global PMI data, discussed in last week’s Global Focus, also noted an acceleration in global growth following a couple of months of weakness, with leading

indicators within the report suggesting more upside in the months ahead.

But as shown in the chart at above, the overall trend of the global composite PMI over the past three months has been weak, which is consistent with less upside in global equities. Markets will likely need to see more than one month of rising momentum to gain confidence in the global growth picture.

Similarly, the breadth of the manufacturing PMIs also showed the first month-to-month improvement since May. But our analysis finds that we need to see more than one month of gains for our equity indicator to turn bullish.

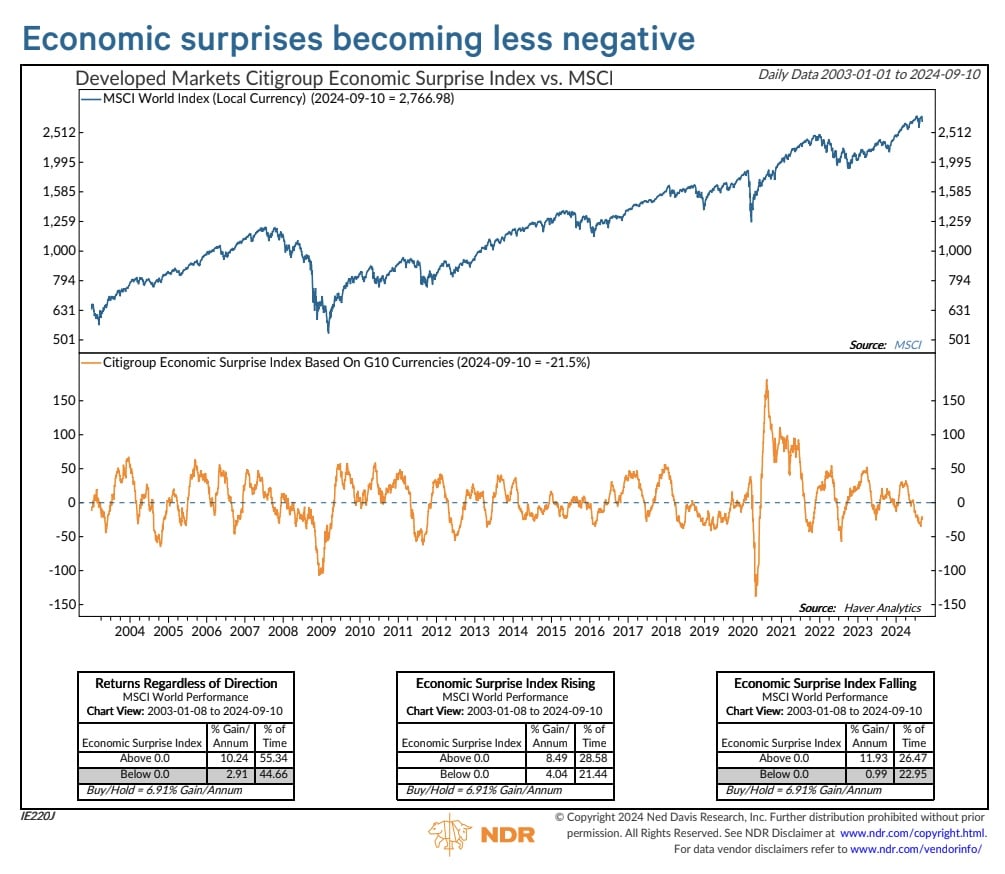

Another significant development in the second half of this year has been a lack of

positive economic surprises. As shown in the chart at above, the Citigroup Economic

Surprise Index for developed economies has been net negative for most of the time

since late May. This is an indication that global economic data has on balance been surprising to the downside and associated with weaker equity market performance.

While still net negative, the index appears to have carved out a bottom in late August.

If the upside is sustained, this is also associated with fewer headwinds to global equities.

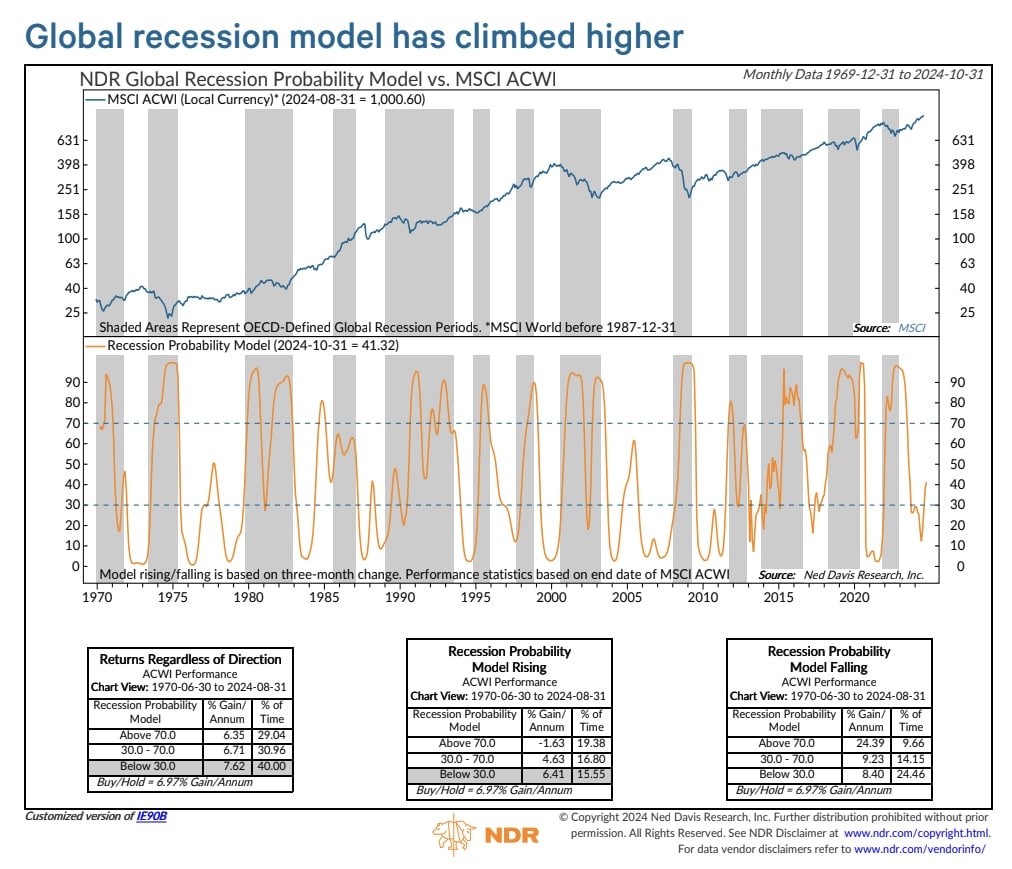

Our Global Recession Probability Model, which is designed to identify OECD-defined global slowdowns (i.e., sharp slowdowns in the global growth rate), jumped to 41% for the month of October, the highest level in a little over a year. This puts the indicator in the mid-risk zone, which is historically consistent with marginal gains in global equities.

Readings in this zone do not necessarily mean recession is imminent. In fact, there have been numerous historical instances where the model has gone into the mid-risk zone and then back down to low risk.

Moreover, as shown in the table below, our Global Recession Watch Report, which is constructed to identify OECD-defined slowdowns, is not showing sufficient evidence of one. Our Severe Global Recession Watch Report, which helps identify outright global recessions, is showing zero evidence.

Easier monetary policy, especially by the Fed this month, could be the saving grace. Whenever the Fed has commenced a rate cut cycle, it was almost always been when our Global Recession Probability Model was already in the high-risk zone. The two rare cycles (1971 and 1989) where the Fed began easing while the model was in the mid-risk zone, eventually saw the model fall back down to low risk.

We will continue to watch all these indicators closely. Although not our base case, a break-down in these indicators will cause us to alter our assessment.

Important Information and Disclaimers The data and analysis contained in NDR’s publications are provided “as is” and without warranty of any kind, either expressed or implied. The information is based on data believed to be reliable, but it is not guaranteed. NDR DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

NDR’s reports reflect opinions of our analysts as of the date of each report, and they will not necessarily be updated as views or information change. All opinions expressed therein are subject to change without notice, and you should always obtain current information and perform due diligence before trading. NDR or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed in NDR’s publications and may purchase or sell such securities without notice. NDR uses and has historically used various methods to evaluate investments which may, at times, produce contradictory recommendations with respect to the same securities. When evaluating the results of prior NDR recommendations or NDR performance rankings, one should also consider that NDR may modify the methods it uses to evaluate investment opportunities from time to time, that model results do not impute or show the compounded adverse effect of transaction costs or management fees or reflect actual investment results, that other less successful recommendations made by NDR are not included with these model performance reports, that some model results do not reflect actual historical recommendations, and that investment models are necessarily constructed with the benefit of hindsight. Unless specifically noted on a chart, report, or other device, all performance measures are purely hypothetical, and are the results of back-tested methodologies using data and analysis over time periods that pre-dated the creation of the analysis and do not reflect tax consequences, execution, commissions, and other trading costs. For these and for many other reasons, the performance of NDR’s past recommendations and model results are not a guarantee of future results. Using any graph, chart, formula, model, or other device to assist in deciding which securities to trade or when to trade them presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves continuously or on any particular occasion. In addition, market participants using such devices can impact the market in a way that changes the effectiveness of such devices. NDR believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision and suggests that all market participants consider differing viewpoints and use a weight of the evidence approach that fits their investment needs. Any particular piece of content or commentary may or may not be representative of the NDR House View, and may not align with any of the other content or commentary that is provided in the service.

Performance measures on any chart or report are not intended to represent the performance of an investment account or portfolio, as some formulas or models may have superior or inferior results over differing time periods based upon macro-economic or investment market regimes. NDR generally provides a full history of a formula or model’s hypothetical performance, which often reflects an “all in” investment of the represented market or security during “buy”, “bullish”, or similar recommendations. This approach is not indicative of the intended usage of the recommendation in a client’s portfolio, and for this reason NDR does not typically display returns as would be commonly stated when reporting portfolio performance. Clients seeking the usage of any NDR content in a simulated portfolio back-test should contact their account representative to discuss testing that NDR can perform using the client’s specific risk tolerances, fees, and other constraints. NDR’s reports are not intended to be the primary basis for investment decisions and are not designed to meet the particular investment needs of any investor. The reports do not address the suitability of any particular investment for any particular investor. The reports do not address the tax consequences of securities, investments, or strategies, and investors should consult their tax advisors before making investment decisions. Investors should seek professional advice before making investment decisions. The reports are not an off er or the solicitation of an off er to buy or to sell a security. Further distribution prohibited without prior permission. Full terms of service, including copyrights, terms of use, and disclaimers are available at https://www.ndr.com/web/ndr/terms-of-service.

Copyright 2024 (c) Ned Davis Research, Inc. All rights reserved.