Americans gearing up for retirement are anxious about their ability to pay for long-term care insurance, yet nearly 80% do not have a plan in place.

That finding is among the results of the latest Retirement Income Literacy Study carried out by The American College of Financial Services.

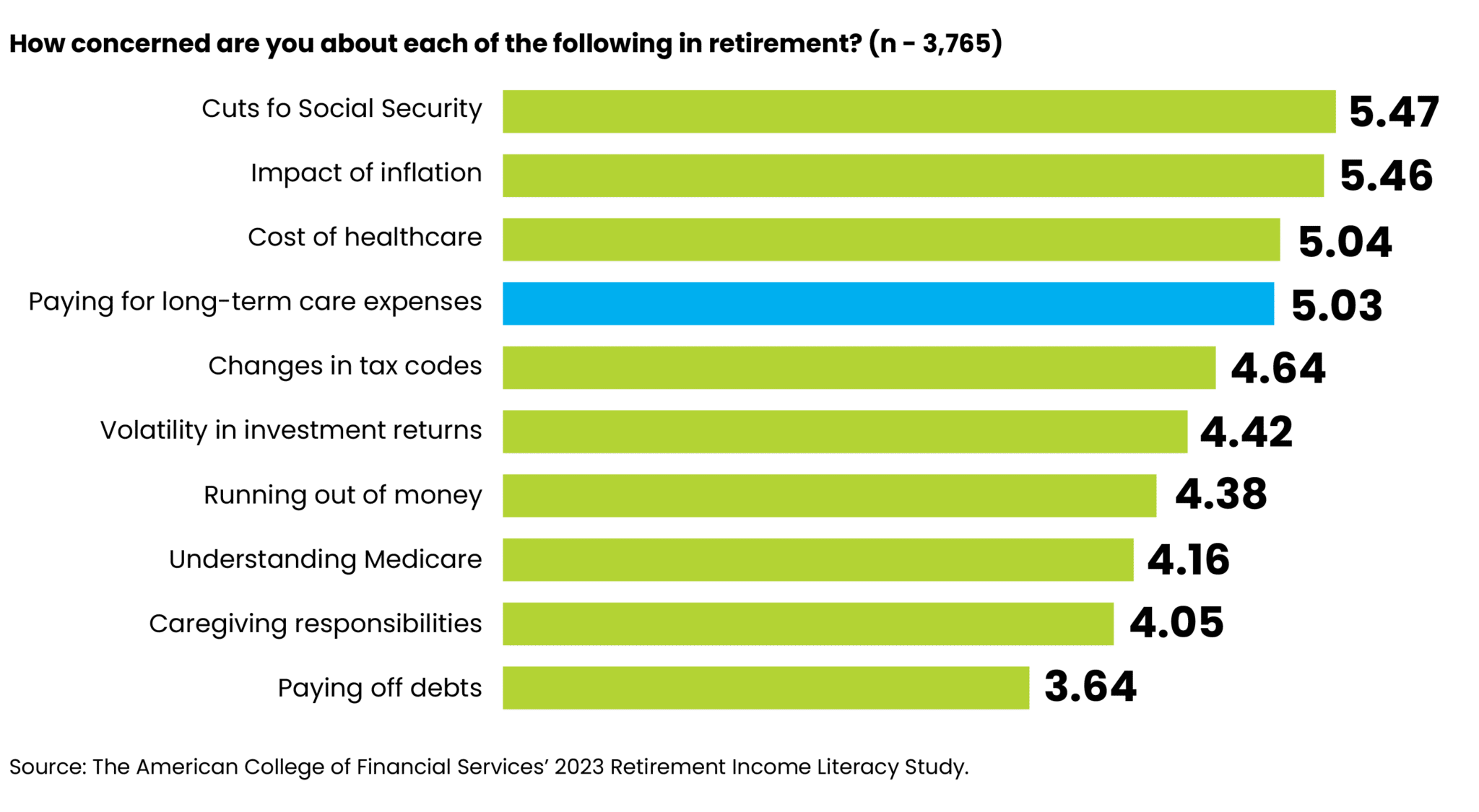

The college’s 2023 survey showed that paying for long-term care expenses was one of respondents’ top concerns, coming in fourth behind worries about cuts to Social Security, the impact of inflation, and healthcare costs.

“This underscores the significance of the anxiety many have about affording care in their later years, specifically this falls fourth in line,” said Kaylee Ranck, director of college research. She made the observation during a webinar, “From Policy to Practice: LTC Insurance Trends and Planning Strategies When Benefits are Used,” the college presented on July 23.

The survey of 3,765 Americans aged 50 to 75 aimed to measure financial literacy in 12 retirement-related knowledge areas among individuals approaching and or in retirement age.

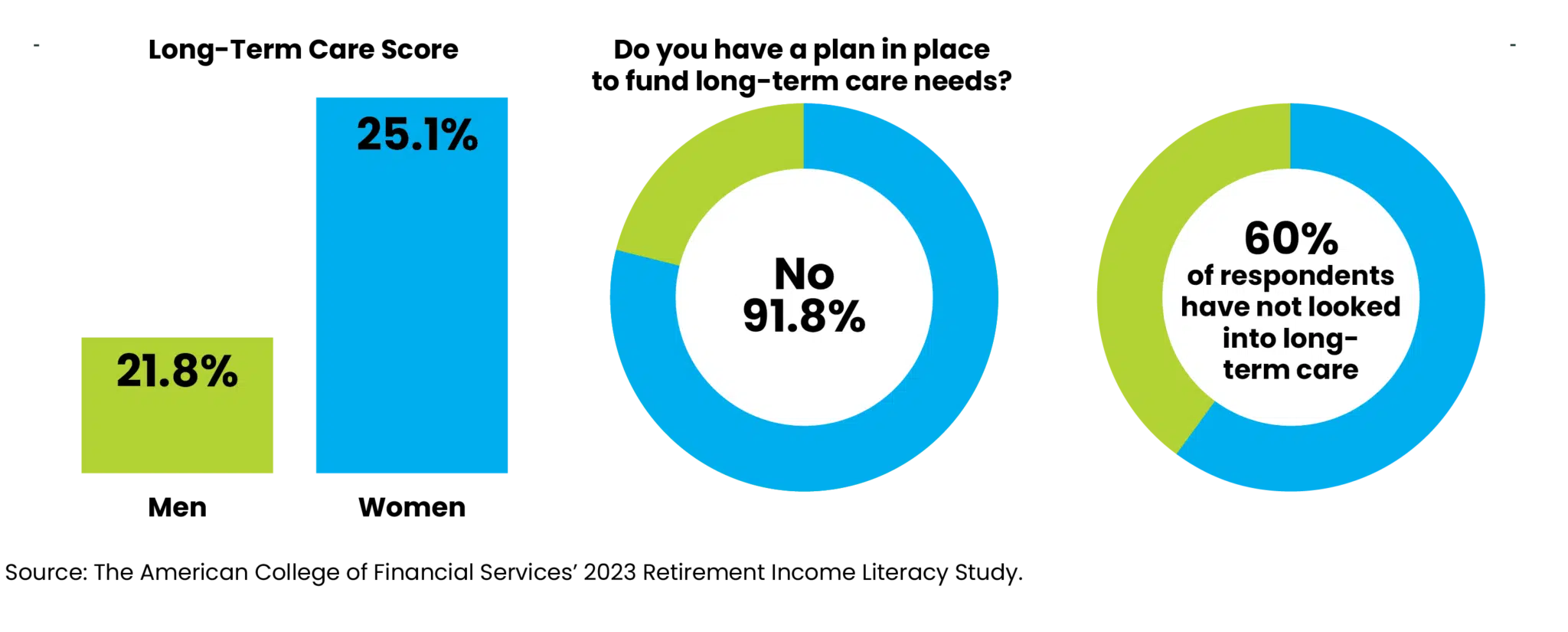

The survey showed that 60% of respondents have not looked into long-term care policies or don’t know whether a plan would be useful. Also, 78.9% do not have a long-term care plan to fund any long-term care needs, Ranck said.

“We found that really there’s a misunderstanding among consumers about whether or not they’re going to actually need long-term care,” she added. For example, the survey showed that 44% state they are “not likely, or not likely at all” to need long-term care, while only one in five could correctly identify that 70% of the population is going to need assistance with the activities of daily living at some point.

“That’s sobering, to say the very least,” said James Karthaus, assistant professor of financial planning at the college, and managing principal of Nautic Financial Group. “That’s nothing less than a crisis,” he added, noting that 70% of people 65 and older will need an average duration of three years of long-term care.

He also noted that 80% of the people receiving long-term care are receiving informal caregiving at home by unpaid caregivers. And as men die earlier, women are bearing the brunt of the caregiving burden.

Develop a Plan

Karthaus noted that a 2015 AARP study showed that 43.5 million people have had unpaid caregivers in the last 12 months. “Those numbers are staggering. The longer we wait, the worse it gets. It is like retirement planning,” he said. “People aren’t planning, and people aren’t buying policies. So we (financial planners) have got to do something about it. We’ve got to raise consciousness.”

He urged financial planners to help clients develop a plan, even if it is not funded. Social Security, pensions or annuities could help fund long-term care, Karthaus said, but these sources may not be adequate unless the person has substantial income. Other options include liquidating savings, investments, emergency funds, lines of credit, and reverse mortgages. He noted that reverse mortgages are a better product since the federal government became involved with these financial products in the 1980s.

People can also tap into state or federal government programs, such as Medicaid, which has an asset limit. Other options could be religious or philanthropic organizations, such as a home for retired military veterans.

“There are places out there we can go to. But the costs are not getting lower. They are going up at 4% a year,” he said, adding that people need to take a long-term perspective and develop solutions that involve federal, state, local, philanthropic and personal assets. “As advisors, we have to make our clients aware of this.”

Transferring the Risk

Transferring the risk is another avenue for financing long-term care. One option is long-term-care insurance, which has been around for about 35 years.

When long-term care insurance was introduced, it was a heady time because it had universal applicability, he said. But a perfect storm was brewing with the sale of a long-tail insurance product for which actuaries had no experience data, he added. That meant it would most likely be years before insurers would have to pay on claims. At the same time, insurers’ pricing was very competitive while interest rates were declining so premiums didn’t grow as insurers expected.

But regulators, thinking they were protecting consumers, didn’t let insurers raise their premiums effectively and companies later collapsed, he said. For example, in New York State, the number of companies selling long-term insurance declined from about 38 companies to about five today. “The industry took a real hit. And I think that led to a real bad taste in the mouth of clients, planners, regulators and carriers, and I think our clients are going to be hurt for it,” Karthaus said.

Now, different alternatives to traditional long-term care insurance products are being developed.

“Personal insurance is kind of going the way of the albatross,” said Karthaus, noting that companies could not recover their costs. Hybrid policies emerged around 2005. Linked to life insurance benefits, they are flexible, with inflation riders and limited cost recovery if the benefits aren’t needed.

Other options include life insurance policies with long-term care riders that have a strong potential cost recovery or cash value, such as a death benefit, if the long-term insurance is not needed. The downside is limited long-term care options and no inflation riders. There are also employer-sponsored long-term care policies, a type of group coverage that is easy to acquire and cost-effective with possibly no underwriting needed. “Probably not a lot of bells and whistles,” he added. Another option is state partnership long-term care policies that increase Medicaid qualification terms. “States are proactive in this area, and they have to be,” he added.

Federal and state-based long-term care insurance policies — group policies for federal and state employees — are another alternative. There are also public long-term care programs, which are state-sponsored programs that allow for some benefits based on years of participation. An example is the WA Cares Fund in Washington State.

Joellen Meckley, a lawyer who is executive director of The American College Center for Special Needs, said many people do not know that Part A of Medicare only pays for up to 100 days of care in a skilled nursing facility. “That’s often shocking to people. So there’s a huge knowledge gap out there,” said Meckley. “And unfortunately, it’s not just with clients. It’s also within our profession, the financial services profession. “

Costs Vary

Meckley said it is important for financial advisors to help clients choose a long-term care insurance policy, but also to guide clients when it is time to use the policy.

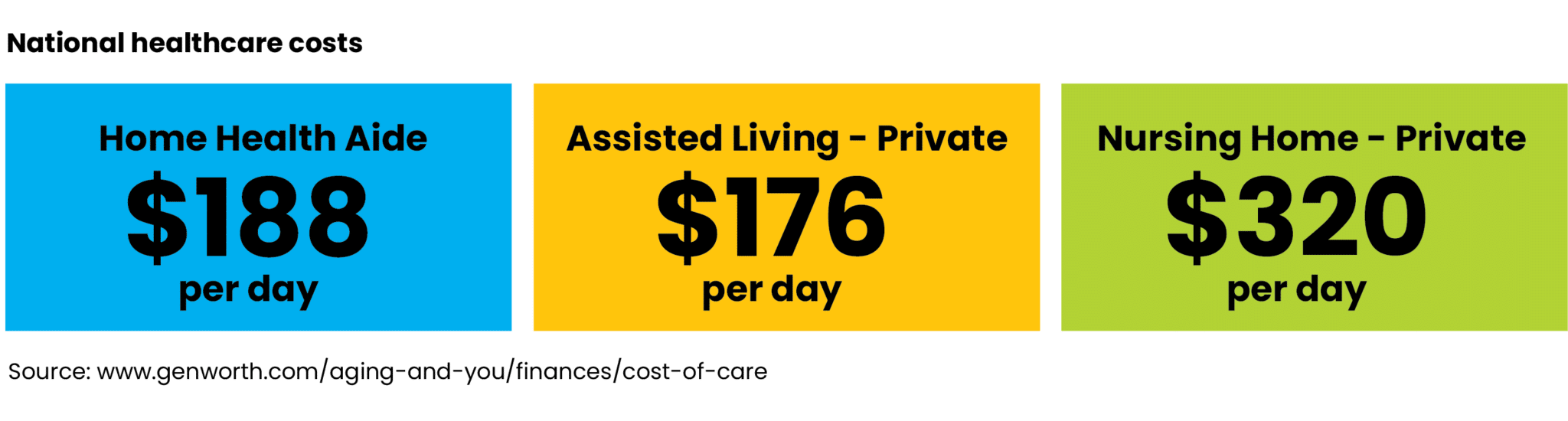

She told webinar participants that Genworth’s annual survey includes solid data as the long-term care insurer surveys thousands of providers nationally. Costs are going up every year and vary around the country. For example, the national median price for a home health aide working 40 hours per week is $188 a day. But that daily cost ranges from $160 in Texas to $217 in Colorado.

“It is absolutely critical … when you’re advising your clients … to understand what it is actually going to cost them,” she said. She also urged financial advisors to adopt a holistic planning approach for their clients that involves other professionals, such as elder care attorneys or aging life care professionals.

“This underscores the significance of the anxiety many have about affording care in their later years, specifically this falls fourth in line,” said Kaylee Ranck, director of college research. She made the observation during a webinar, “From Policy to Practice: LTC Insurance Trends and Planning Strategies When Benefits are Used,” the college presented on July 23.

“This underscores the significance of the anxiety many have about affording care in their later years, specifically this falls fourth in line,” said Kaylee Ranck, director of college research. She made the observation during a webinar, “From Policy to Practice: LTC Insurance Trends and Planning Strategies When Benefits are Used,” the college presented on July 23.

“We found that really there’s a misunderstanding among consumers about whether or not they’re going to actually need long-term care,” she added. For example, the survey showed that 44% state they are “not likely, or not likely at all” to need long-term care, while only one in five could correctly identify that 70% of the population is going to need assistance with the activities of daily living at some point.

“We found that really there’s a misunderstanding among consumers about whether or not they’re going to actually need long-term care,” she added. For example, the survey showed that 44% state they are “not likely, or not likely at all” to need long-term care, while only one in five could correctly identify that 70% of the population is going to need assistance with the activities of daily living at some point. “It is absolutely critical … when you’re advising your clients … to understand what it is actually going to cost them,” she said. She also urged financial advisors to adopt a holistic planning approach for their clients that involves other professionals, such as elder care attorneys or aging life care professionals.

“It is absolutely critical … when you’re advising your clients … to understand what it is actually going to cost them,” she said. She also urged financial advisors to adopt a holistic planning approach for their clients that involves other professionals, such as elder care attorneys or aging life care professionals.