The economic debate in this election year has centered on the costs of proposed policies. Politicians have been trying to put the cart before the horse, as they make plans to spend money before being certain that the money will be available.

The debate on this front has been particularly active in Europe, where rules on national budgets underpin the monetary union. Tensions over how those rules should be applied have simmered frequently since they were first adopted, but they may be on the verge of boiling over.

The first Stability and Growth Pact (SGP) was adopted in 1997. It established caps on annual government deficits and aggregate public debt for countries using the euro. The Pact has been updated and amended several times, most recently late last year. We expressed concern about the most recent edition in this January commentary.

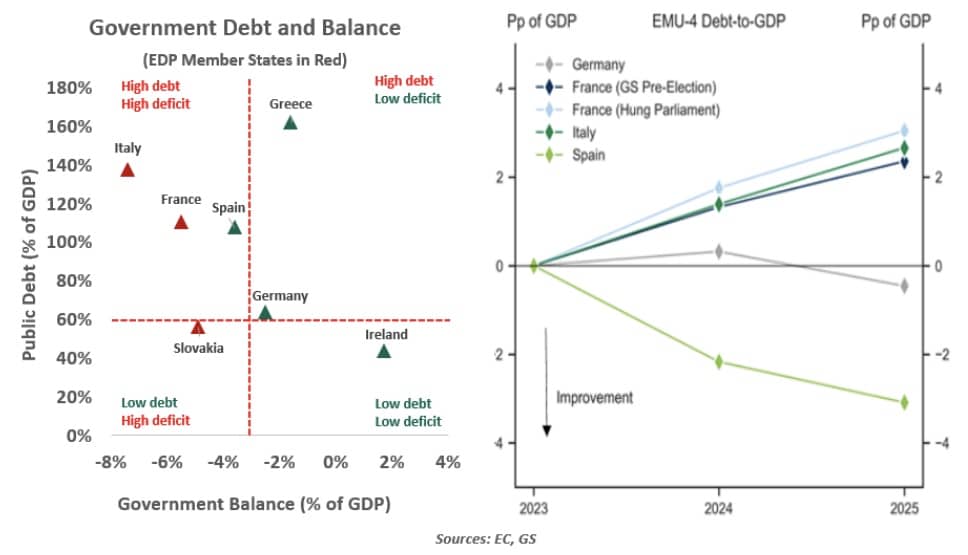

The reformed rulebook retains the two goals of maintaining public debt below 60% of gross domestic product (GDP) and deficits below 3% of GDP. However, it allows a slow but steady pace of deficit and debt reduction over four to seven years, with the longer option available if a country undertakes reforms and investments that are in line with the bloc’s strategic priorities.

The SGP calls for the European Commission (EC) to enforce the standard. The vehicle through which this is achieved is called an Excessive Deficit Procedure (EDP), which initiates a timetable for countries to get their fiscal positions back within guidelines.

The EC can also levy penalties if a country fails to take corrective action. This step has never been taken, given the potential for adverse political and economic reactions.

It didn’t take long for the new pact to be put to the test. The EC recently took the first step towards placing seven countries into an EDP. Among the seven was France, which drew a lot of attention because of the sheer size of its economy, deficit and debt.

The EC decided to exempt Spain from the disciplinary step, despite the country exceeding the fiscal limits. Deficits and debt there are to follow a downward trajectory, as per a recent European Commission forecast, which allowed some lenience.

For France, the announcement couldn’t come at a worse time. President Emmanuel Macron’s gamble to call snap elections has backfired, pushing the country into a period of uncertainty. The deeply divided government that will soon be seated has sparked renewed concern about the sustainability of French public finances.

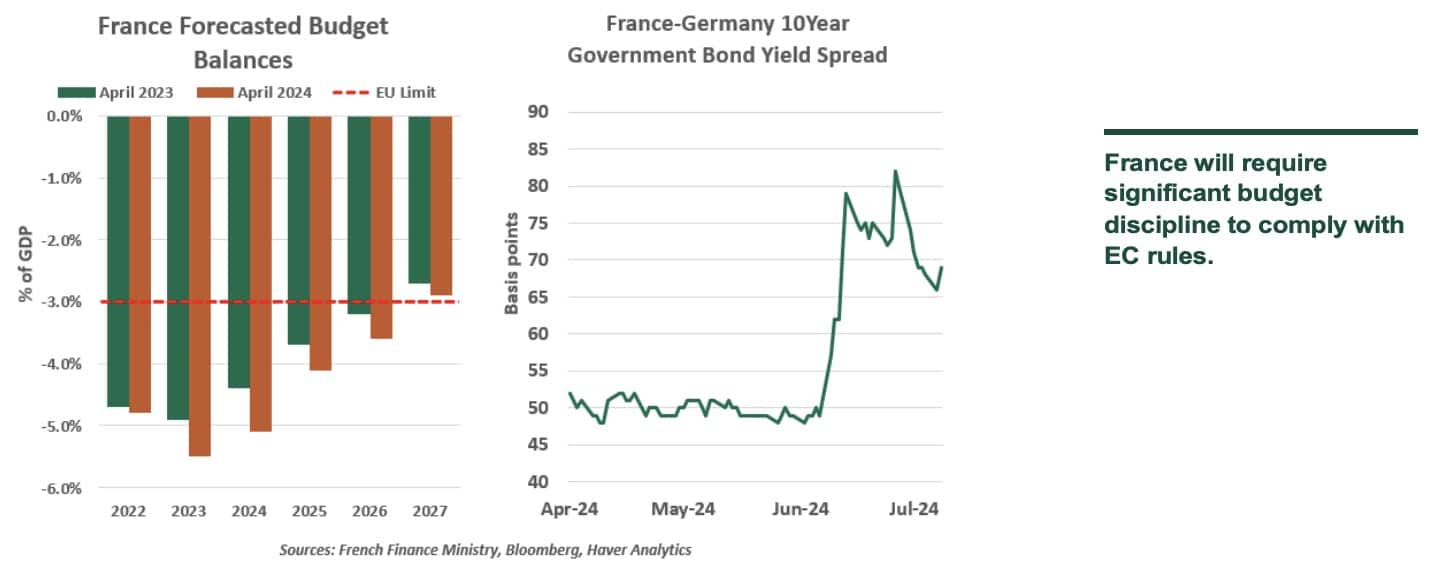

Public debt in France is projected by the EC to rise from 110% of GDP in 2023 to almost 114% of GDP next year. In May, global ratings agency S&P downgraded the country’s credit score for the first time since 2013, amid the deteriorating budget position.

The new French assembly will struggle to pass economic and fiscal measures, leading to fiscal slippage relative to prevailing guidance. Attempts to form a so-called “Rainbow Coalition” of several parties will require significant compromises, mostly on fiscal consolidation.

Macron is facing calls to roll back the 2023 pension reforms, increase spending on public services, cap the prices of essential goods, and raise the minimum wage. Proposed increases in taxes for high earners will not be enough to offset the potential increase in expenditures.

A newly formed government will be tasked not only with implementing the 2024 budget, but it will also have to present a 2025 budget by October to the European Commission. The outgoing government guided towards reducing the deficit from 5.5% of GDP in 2023 to 5.1% of GDP this year and 4.1% next year, which were necessary to reassure financial markets.

Some would argue that a slower pace of deficit reduction will reduce the drag on growth in France, but it is also worth stressing that an expansionary fiscal policy will raise concerns of sustainability of public debt. This would cause financial conditions to tighten, thereby weighing on growth. Already, the spread of French bond yields to German bond yields has widened considerably.

The exact size of required fiscal correction for France will be known by the fall when the government prepares next year’s budgets. A deficit reduction of at least 0.5% of GDP is mandated by the new European fiscal policy.

Financial market volatility has not raised an alarm at the European Central Bank (ECB) yet. But a failure to enact the required fiscal measures will render countries in EDP ineligible for the ECB’s emergency bond-buying program – the Transmission Protection Instrument. This would hinder the central bank’s ability to intervene and prevent further widening of spreads.

A major dilemma for European governments is that fiscal space is constrained, growth needs a push and the continent is threatened by war on its Eastern border. Security, energy transition, and technology all require investment. But there is also no politically easy way to find the fiscal space to address the challenges that Europe faces without triggering financial stability risks.

The initiation of EDPs will not help Europe unite to confront the economic and geopolitical challenges of the day. Unfortunately, a mechanism intended to foster growth and stability may produce the opposite outcomes.

Digital Discontent

Editor’s Note: This is an updated version of a piece we originally published in 2017, well before the hype surrounding artificial intelligence (AI) gathered momentum. The material is even more poignant today than it was seven years ago.

The first computer I ever used was a monster. I have no idea how they got the device up to the second floor of my grade school (which was more than 80 years old and had no elevator), and the lights in the library flickered every time we turned the thing on. To bring the machine to life, we had to dial a number on an adjacent telephone, wait for a tone and then plunge the receiver into a set of suction cups.

Interestingly, the first thing I ever did on that contraption was play Mancala, a game invented by Bedouins thousands of years ago using sand pits and stones. The computer defeated me the first few times, but then I began to recognize patterns in its play that made its moves easy to anticipate. After I began to beat it consistently, I rapidly lost interest because the opponent was overly robotic.

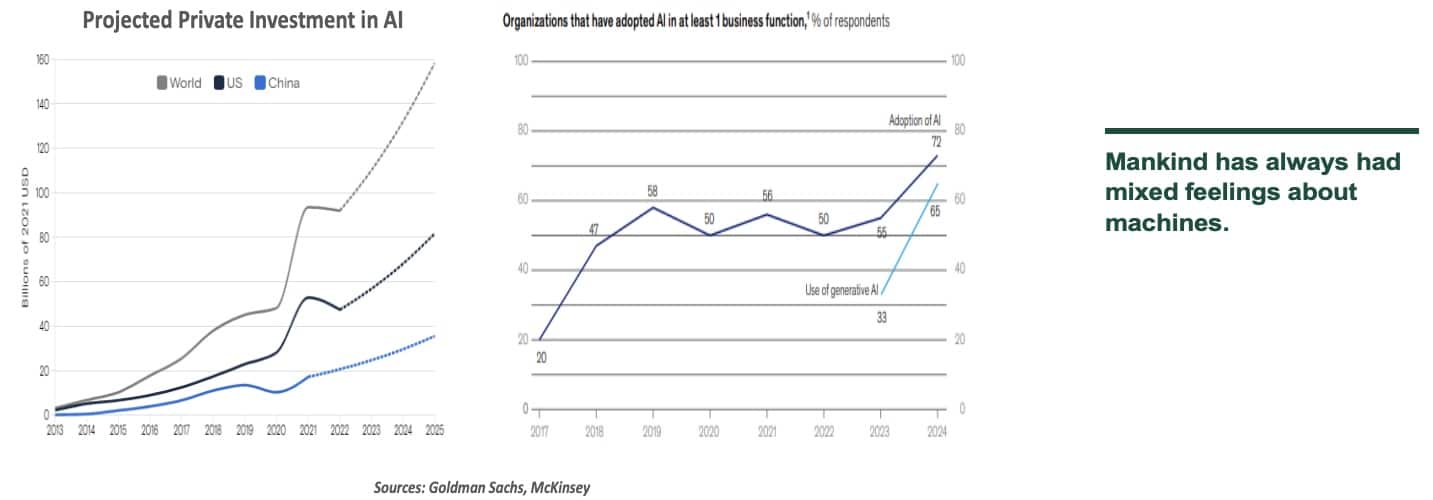

That vintage computer seems as primitive today as the idea of playing games in the sand was back in the 1970s. Computers have become much more powerful, and they are able to learn from their experiences; today’s software plays chess and Gomoku better than top grandmasters. With artificial intelligence now trained on commercial applications, many are wondering what other things machines might eventually do better than people. And that prospect is creating economic unease around the world.

The transition from man to machine is a long-running industrial theme. Two hundred years ago, steam-powered mills began replacing human weavers (prompting destructive retaliation from the Luddites). In the 1800s, the advent of automated reapers disrupted agriculture. In the last century, robots took deep root on the factory floor. And, most recently, artificial intelligence has started to transform a number of professions.

Economic theory suggests workers should welcome technological advances, not fear them. Anything that makes labor more productive raises its value, which generally results in better pay, more leisure time, or both. At a time when global productivity growth has been slow, the press for additional efficiency should be seen as a good thing.

Despite the inexorable march of innovation, employment has continued upward. When change occurs, it is fairly easy to identify the jobs that might be at risk but more difficult to identify the ones that will arise to take their places. But those new opportunities have always appeared, and market economies adapt to embrace them. Thirty years ago, few would have foreseen that thousands of people would be working on cybersecurity, gene-based therapies or driverless logistics. But all are growth fields today.

Further, the developed world has a demographic problem. Postwar generations are transitioning into retirement, birth rates are low and global attitudes towards immigration are under review. With labor force growth slowing to a crawl, advancing automation would seem to be an elegant solution. The example of long-haul logistics is often cited here: driverless transportation could compensate for substantial impending retirements from the ranks of truck drivers and train engineers.

Nonetheless, there seems to be significant apprehension about current advances in AI. The science seems to be moving ahead rapidly, affecting work across a broad range of industries. The race to disrupt has captured the imagination of venture capitalists, but strikes fear into the hearts of the masses

It has been traditionally assumed that human beings would transition from repetitive work to more cerebral work as automation took deeper root. Programmers would provide instructions to the machines, technicians would monitor their performance and analysts would interpret the immense amounts of data collected in the process.

But advances in artificial intelligence have enabled machines to analyze outcomes, communicate in natural language and direct their own actions. Interestingly, many different kinds of programming are being done by AI. Extrapolating on these developments, observers have created lists of jobs that will become obsolete (in whole, or in part) in the coming decades.

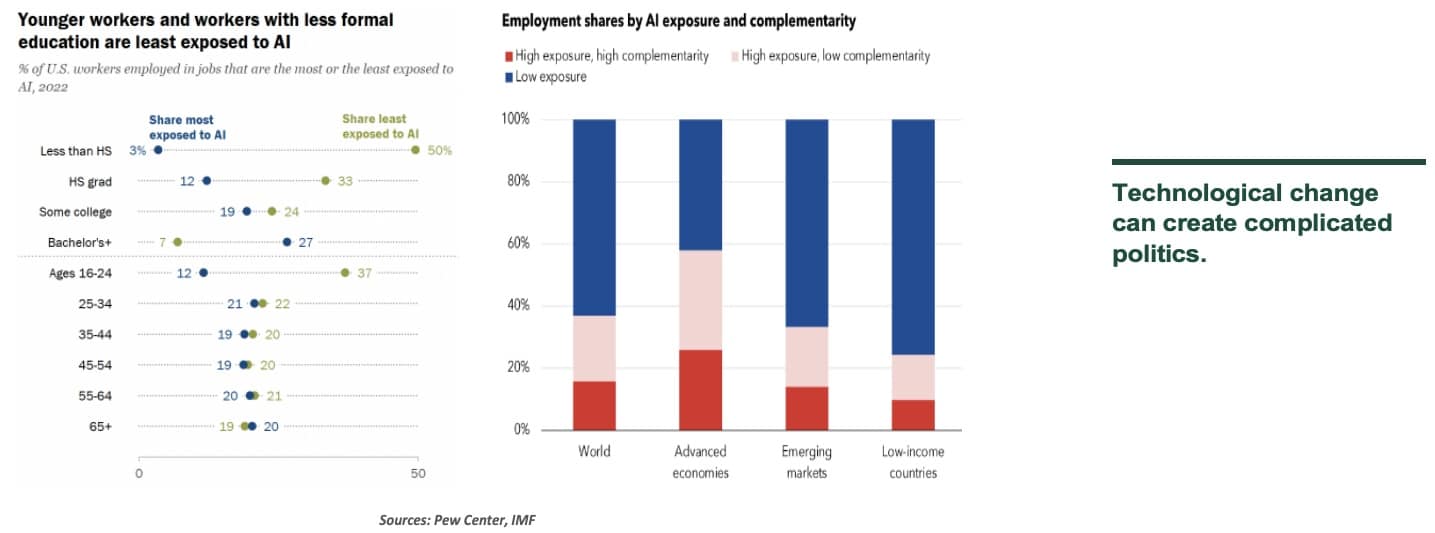

This evolution turns previous waves of automation on their heads. More educated workers in developed countries are most vulnerable this time around. Fields like finance, engineering and the law are among those most exposed. Workers with more education are more at risk.

Questions also surround who will reap the rewards of the impending transformation. AI is forecast to usher in a new era of productivity growth, which should raise the marginal value of labor. But there is some concern that the value unlocked by the new technology will be concentrated in the hands of a few companies and individuals, and not the population at large.

Add in concerns about the use of AI by cybercriminals, and you have the makings of broad-based anxiety. And this feeling can affect what people do within polling places

While today’s threats seem pressing and proximate, it could be many years (or even decades) before we see broad-based worker displacement. New concepts require long periods of testing and adoption before they reach full potency. Some may prove too costly, while others may be hindered by social or regulatory restrictions.

To assuage concerns, some have proposed curbs on the application of AI and restricting its access to sensitive data. But history suggests that it is better to embrace progress than hinder it. There is certainly more work to do in many societies to sustain equality of opportunity, but few would recommend a policy of banning backhoes so that people can go back to digging foundations with shovels.

Nonetheless, I am hedging my bets. Futurists suggest there is a 50% chance that economists will be superseded by computers, but less than a 1% chance that dentists will. Goodbye, Keynes, hello, cavities.