I have a client at a large financial services firm who I have worked with for many years. We used to exchange stories about our children who are somewhat similar ages. We talked about their sporting activities, what was happening at school and, eventually, what colleges they were choosing for their next phase.

Recently I had a hard time getting hold of this client and eventually learned the family is struggling to care for an elderly family member with dementia. The situation morphed into a discussion about how “normal” it is in our industry to talk about raising our family — struggles with children, concerns about college planning, different personalities and so on. And how “not normal” and almost taboo it can be, to talk about the challenge of dealing with an elderly relative, especially when dementia is part of the situation.

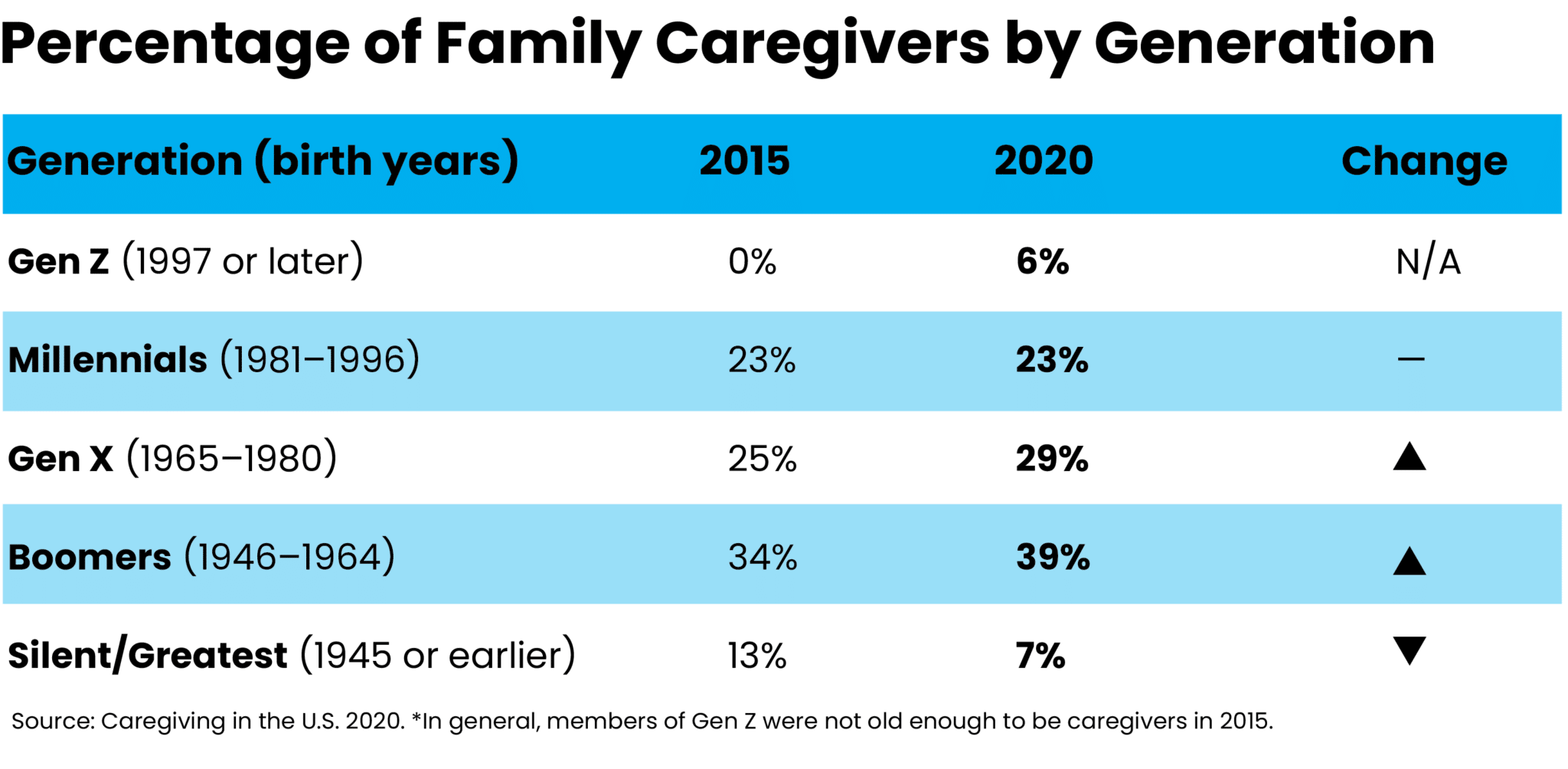

Yet statistics for the five-year span 2015-2020 show an enormous spike in caregiving by those whom you, as advisors, are likely working with to help manage their retirement:

For example, baby boomers comprised almost 40% of all family caregivers in 2020. Now, four years later, and with Covid having taken its toll, this number could likely be even much higher. Meanwhile, millenials, who are actively trying to save money, and Gen Xers, who are combining the cost of raising their own families with saving for retirement, are taking on a large load, too.

These numbers are stunning when you think that one in five (at minimum) Americans is caring for a family member without receiving compensation for this role.

Consider what this means to you as the advisor as you plan for retirement and beyond with your clients.

Under the Radar

In many cases, your clients may not tell you about the care they are providing for their parents, siblings or other aging family members. You could also be working alongside someone in your firm who is quietly dealing with these responsibilities. The bottom line is that you could be making the best plans for retirement with your clients without realizing the secret emotional, physical and financial load they carry.

The topic of eldercare is not explored as much as it should be when helping clients plan for and rethink age 65 and beyond. In too many cases, the advisor is still focused on “the number,” which is how much the client will need on a monthly basis in retirement. It’s important to complete this worksheet with clients, and have the hopes and dreams conversation along with it. It’s helpful to get them to think about how they will spend their time and what really matters. But you are doing them a disservice if you are not asking about their possible role as caregivers. This shouldn’t be viewed from just a long-term care perspective — it should also consider smaller, shorter-term responsibilities that can consume their time and money.

My $3,500 Added Expense

Here’s an example of how the lack of discussion can get missed in budgeting/planning for retirement discussions:

During Covid, I grocery shopped for my elderly parents to make sure they didn’t leave their house. I treated them quite well and bought them prepared food that they may not have bought for themselves. Knowing they are not wealthy by any means, I wouldn’t take money for their groceries. On average, this increased my own expenses by $250 to $350 per month.

Because I hated having my parents trapped in their house, I sometimes sent them DoorDash from their favorite restaurant. This pushed my monthly number up by another $150 to $200 from time time. Over the year, I spent more than $3,500 on food for my parents. Once Covid ended, my parents went back to doing their own shopping. However, this illustrates how a simple caregiving experience can add up!

A Priceless Opportunity

Initiating dialogue on this topic is also a great way to involve the next generation to discuss what “care” might look like, what inherited traits (for example, dementia) might exist that will need to be funded, and what plans would be put in place should care be needed.

Start the dialogue by exploring the importance of being a caregiver with your clients. If they find themselves in the caregiving role, it could completely upend their well-laid plans for retirement and you don’t want to miss an opportunity to prepare them.

Additional Reading: Overcoming Common Struggles Facing Advisors

Some open-ended questions to consider with your clients while engaging in planning could include:

- What ages are your parents and what is their health today? What other relatives are older and might need care over the next one-to -10 years?

- What plans do your parents have for care if something should happen to them?

- What financial responsibilites have you, or might you, assume to help care for your relatives?

- Who is the primary caregiver in your family? How does this person interact with you (or if you are it, how do you interact with others)?

- How are decisions made about what your relatives will need as time goes on?

- What is your family philosophy around caregiving? For example, do people age-in-place or do they seek assisted living or other lifestyle options? What is your personal philosophy for care if someone needed your help?

- What have you discussed with your children about caregiving?

- What would you expect of your children if something were to happen to you either mentally or physically?

- In retirement, what role do you see caregiving playing with the rest of what you hope to do?

- What resources do you have if you need support as the caregiver, or if you become the person who needs care?

Open the Door Now

Many Gen Xers find themselves in the sandwich generation where they may be raising their children (often dealing with everything from childcare to college expenses) and trying to care for their boomer parents or Silent Gen grandparents. While the average lifespan in the U.S. has dropped over the last couple of years, the average age of the population is now older than it has ever been. This likely means that if it isn’t an issue now for your clients, it certainly will be in the next five to 15 years as they rethink retirement.

Your job as advisor is to open the door to this topic and bring it into the planning discussion. It’s typical to talk about children, and plan for the future but it isn’t as typical to talk about the role of the elder caregiver: how it could impact them and their hopes and dreams, and their portfolios.

If you are looking at today’s expenses and extralopating for retirement based on what your clients tell you they want to do, but they aren’t including current or possibly future expenses associated with providing elder care, you are likely underestimating what might be needed.

Don’t lose sight of this for your clients. Start talking to them about it now and help them bring a taboo topic into the open and include it in their planning.

Beverly Flaxington, MBA, an investment industry veteran with over 30 years of experience, runs The Collaborative, a training, coaching and consulting firm devoted to business building for the financial services industry. The firm founded and manages the Advisors Sales Academy, and won the Wealthbriefing WealthTech award for Best Training Solution for 2022, 2023 and 2024. Beverly is also an adjunct professor at Suffolk University, teaching graduate students about leadership, managerial skills and team leading. She is a Certified Professional Behavioral Analyst (CPBA) and Certified Professional Values Analyst (CPVA).