While busy managing the financial and personal needs of wealthy individuals, family offices could find themselves entangled in the intricacies of a three-year old piece of federal legislation meant to combat tax fraud, money laundering and terrorist financing.

Unbeknownst to many financial advisors, new federal reporting requirements for small businesses kicked in on January 1 of this year and could impact family offices and their high-net worth clients. The reporting requisites are part of the Corporate Transparency Act, which the U.S. Congress passed in 2021 to prevent malevolent individuals from using their ownership of U.S. entities to support illegal operations.

Missing the reporting obligations on time could whack thousands of family offices with hefty fines — and even jail time if the offense was committed intentionally. The act requires millions of small businesses to submit a beneficial ownership information, or BOI, report for each of its beneficial owners to the U.S. Department of Treasury’s Financial Crimes Enforcement Network, also known as FinCEN.

“Many trusts and estates are unaware of how this new law will impact them,” said Jonathan B. Wilson, chief executive officer of FinCEN Report Company, during a March 26 webinar titled “Family Offices and the Corporate Transparency Act.”

“Failing to file on time may result in a $500-per-day fine. And the willful failure to file, or filing false information, may be a felony,” he said.

“More people know if Taylor Swift goes out for a latte than know about the Corporate Transparency Act”

— Jonathan B. Wilson, FinCEN Report Company

“More people know if Taylor Swift goes out for a latte than know about the Corporate Transparency Act,” Wilson added.

Hefty Fines

The $500 daily fine can add up quickly as companies needing to submit these reports have a limited time to file their initial BOI reports. For qualifying reporting companies established before Jan. 1 of this year, the filing deadline is Jan. 1, 2025. Yet if they don’t file by that time, the $500 per day fine would be retroactive and kick in on Jan. 1, 2024. “That’s a lot of money,” said Wilson, adding that finding attorneys and financial advisors with the expertise to handle these reporting requirements will be challenging.

“The legal advisors that can handle this issue are relatively few and they are going to be slammed in the second half of this year,” said Wilson, who set up FinCEN Report three years ago. “Small business and family offices need to find counsel now. They also need to find a filing platform.”

Businesses created between Jan. 1, 2024 and Jan. 1, 2025 will have 90 days from either the actual notice of its formation or its public announcement — whichever comes first — to file the BOI. That means a company set up on Jan. 2 of this year, for example, must file the pertinent information by Apr. 2, 2024 or fines will start racking up.

Businesses established on or after Jan. 1, 2025, will have 30 days from notification or public announcement of their formation to submit their first report to FinCEN. The law is expected to impact about 32 million small businesses, including the country’s 7,000 to 8,000 family offices, he said.

The law outlines two types of reporting companies that will be required to submit BOI reports: domestic reporting companies, including LLCs, corporations, and other entities formed through filing with a secretary of state or a comparable office in the U.S.; and foreign reporting companies that are registered to conduct business in the United States, through filing with a secretary of state or an equivalent office.

Exempted Companies

Yet there are 23 categories of companies – such as publicly traded companies, banks, insurance companies, credit unions, investment companies and investment advisors – which are exempt from the reporting requirements. The rational for the exemptions is that these companies are already regulated in such a way that their beneficial ownership is either publicly available or known to the government in some other way, Wilson said.

“You want to get your exemptions right,” Wilson said. “You need to consult an attorney and need legal back-up. If your exemption falls through, there is the $500 per day fine.”

He told webinar participants that financial advisors will need an attorney to unwind the trust rule section and managers in family offices may find they need to amend their trust agreements. He urged advisors to review the Trust Rule in Section 380(d)(ii)(C) of the law.

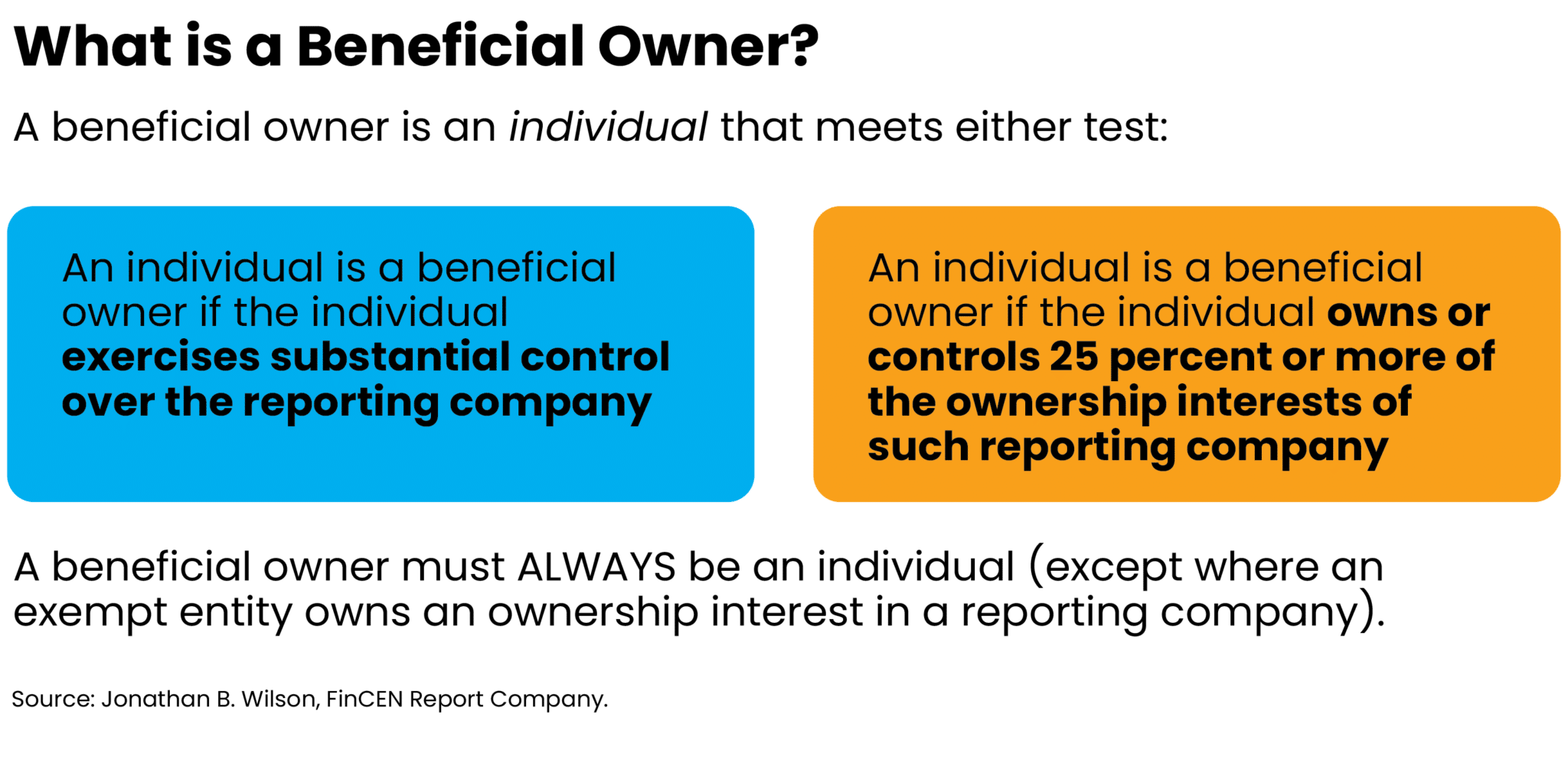

A Beneficial Owner

He pointed out that an individual qualifies as a beneficial owner if they directly, or indirectly, have a significant ownership stake in a company. That means this person either has a major influence on the reporting company’s decisions or operations; owns at least 25% of the company’s shares; or has a similar level of control over the company’s equity.

Wilson cautioned financial advisors and family office managers to be careful of how the ownership percentages are calculated and urged them to review the Calculation Rule, found in Section 1010.380(d)(2)(iii) of the law.

If the ownership percentage is not clear, advisors will have to apply the substantial control test to determine if a person qualifies as a beneficial owner. Noting that substantial control can be difficult to assess, he urged webinar participants to remember this is an anti-money laundering law.

“Think of it as a Tony Soprano rule,” he said, remembering the character in the U.S. crime drama television series “The Sopranos.” Soprano acted like an owner of the Italian restaurant in the series though he was not an owner, Wilson said. “Even if the person is not on the board or doesn’t own shares in the company, if they exercise enormous influence, they may meet the substantial control test and have to report,” he added.

There is no fee for submitting the BOI reports and electronic forms are available on FinCEN’s website. And while there is no annual reporting requirement, family offices managers will have to update the original filing when certain information changes. Financial advisors need to be aware of the 30-day amendment rule, by which specific changes in a beneficial owner’s’ data must be reported.

Reporting Details

The details that reporting companies need to include in their BOI report vary based on the date their business was established. Businesses registered or established after Jan. 1, 2024 must provide information regarding the business, its beneficial owners, and its company applicants — including owners’ and applicants’ (if applicable) names, addresses, birthdays and identification numbers (such as a license or passport number), and the jurisdiction of the documents. Yet businesses established before that date can omit information regarding company applicants.

All reporting companies must provide their legal name and trademarks, as well as their current U.S. address, which could be either the address of its main business site or, for foreign-based companies, their U.S. operational location. They will also need to provide a taxpayer identification number and specify the jurisdiction where they were formed or registered.

Based in Atlanta, FinCEN Report is an online filing service for business owners and compliance professionals affected by the Corporate Transparency Act.

Paula L. Green is a New York City-based freelance journalist with more than three decades of reporting and editing experience that spans coverage of international business and finance issues to murders and politics at the Jersey Shore to presidential press conferences in Argentina and Mexico. She can be contacted by plgreen12004@gmail.com.