While the concept of investing organized around environmental, social and governance (ESG) principles has become more broadly known in the last five or so years, the basic principle of socially responsible investing has been around, in one form or another, for at least 70 years.

By the 1950s and ’60s, electrical and mine workers unions invested a portion of their pension funds in affordable housing and health facilities for American workers. Various movements of the 1960s and ’70s, including the inaugural Earth Day, organized by Wisconsin senator Gaylord Nelson in April 1970, fueled growing interest in social and environmental causes and, in turn, ESG.

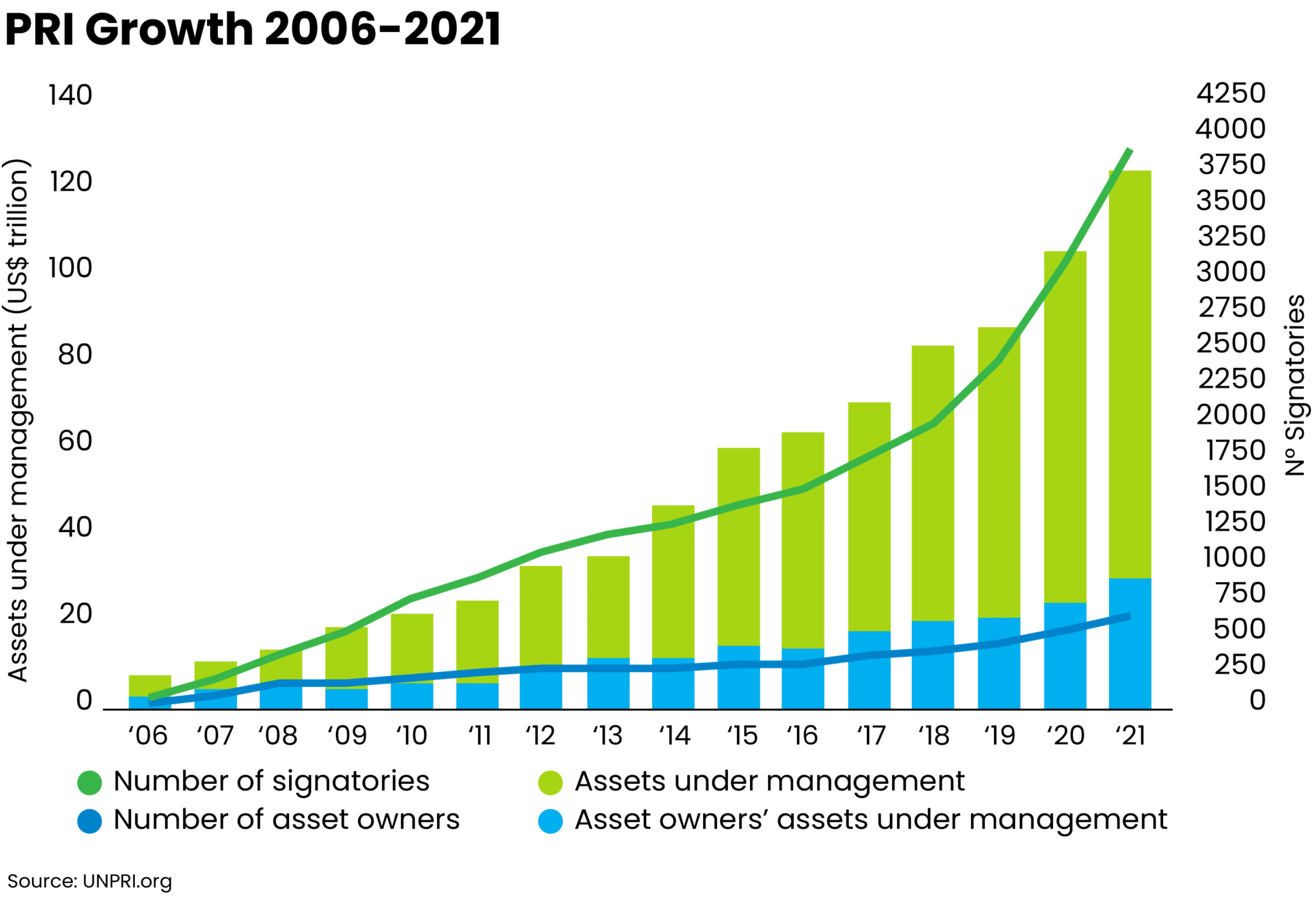

In 2006, the United Nations launched its “Principles for Responsible Investment,” developed by institutional investors who committed to incorporate ESG principles into their investment analysis, decision-making, policies and practices. From the initial 63 investment companies with $6.5 trillion in AUM, the number of signatories grew to nearly 4,000 over the next 15 years, comprising more than $120 trillion in AUM.

To date, emphasis on ESG and related principles appears to be proceeding more rapidly in corporations than among investors, though both trends are on the rise. According to the 2022 sustainability action report from Deloitte, 57% of corporate executives report implementation of working groups tasked with focusing strategic attention on ESG; an additional 42% report plans to form such groups. These figures compare with 21% reported implementation in 2021: a 171% increase.

On the other hand, investors, according to a 2022 Gallup survey, while displaying broad-based interest in ESG (48%), appear to be somewhat slower in deploying funds accordingly, with only about 10% reporting actual investment in ESG-related funds. By contrast, a 2022 study by Capital Group found that some 89% of investors factored ESG concerns into their investment strategies. (This may reflect a greater presence of institutional investors than represented in the Gallup survey.)

What about the numbers?

As fiduciaries charged with guiding clients toward suitable financial outcomes, of course, advisors must balance attention to ESG with actual investment performance. Given the rapid rise in the numbers of financial entities involved with ESG over the past few years, there’s little doubt that more opportunities for ESG investing exist now than ever before. But how can you evaluate the success of these investments? Is there a reliable measure?

That’s a valid question. Some advisors point to the relatively higher expense ratios. Other advisors question the reliability of available metrics, suspecting they may be biased against certain industry sectors such as fossil fuels. Others point out that portfolio performance may be impacted by how ESG principles are interpreted and applied to investment strategy. So, even if an investor values ESG principles, over-reliance on a company’s ESG scores may be a concern.

What about your clients?

Given the rising attention given to ESG, you may already have clients asking about it and its place—if any—in their portfolios. On the other hand, the political climate — no pun intended — around ESG in recent years has certainly become more fraught, with certain terms (“climate change,” “social justice” or “sustainability,” for example) becoming trigger words for some that can generate more heat than light.

In other words, the approach you choose to take around discussing ESG with your clients should be tempered by knowledge and consideration of your clients, their goals, and their beliefs and priorities (all of which should be familiar territory for fiduciary advisors).

For example, you may find that younger clients are more interested in ESG than those who are older (though usual caveats about stereotypes clearly apply). Clients with careers in certain industries may be more sensitive to these considerations than others, both positively and negatively. As with almost every other aspect of investment advising, ESG is not a one-size-fits-all concept; applying it in advising your clients involves individualized attention to each situation.

The Upside

So, what advantages might accrue from incorporating ESG principles in a particular client’s portfolio design? Are the real-world benefits sufficient to justify the effort?

Risk mitigation. Many proponents of ESG suggest that when companies strive to operate more sustainably and responsibly, they are less vulnerable to various risks. Environmental disasters like the BP oil spill and the Exxon Valdez, or regulatory risks like those contributing to the Enron debacle, are less likely to arise when companies make a good-faith effort to employ good environmental, social and governance practices.

Potentially competitive returns. According to research conducted by MSCI, ESG-focused investments can provide returns in line with or, in some cases, superior to more traditional approaches. The study found that three major factors contributed to potentially superior performance: higher profitability, lower “tail risk,” and lower systemic risk (and see also the first factor above).

Diversification. Depending on a client’s other holdings, focusing a portion of holdings on investments with an ESG emphasis can spread risk better.

Longer-term perspective. The nature of ESG tends to favor companies that favor longer-term sustainability over short-term considerations. This may be a better match for certain clients’ overall financial strategies.

The Downside

Of course, any fair analysis must also consider the potential pitfalls of a given approach. What are the things to watch out for as you discuss ESG investing with your clients?

Lack of standardized metrics. While various organizations rate corporations and funds for their ESG practices, each has slightly different methods and standards. This makes it difficult for advisors and others to apply a consistent metric to investing decisions.

Limited investment choices. If investors screen out every company or fund that doesn’t fully meet their ESG rating standards, they may actually be limiting their ability to adequately diversify. This, of course, can lead to concentration risks.

“Greenwashing.” Some companies may overstate their ESG efforts in order to appear more “green” or “sustainable” than they really are. In fact, some companies have fallen under regulatory scrutiny or outright sanctions because of such misleading practices.

Higher investment costs. Certain ESG funds may charge higher management and other fees than comparable funds using more traditional selection criteria. Higher fees can, of course, lead to lower overall portfolio returns.

What do you say?

How should you funnel all this into how you advise clients? Obviously, you must first decide your own stance on ESG and its impacts on financial viability and performance. Then, you must distill your position into a concise statement that communicates clearly, without “insider” jargon. If you believe in the value of ESG for investors and can communicate your reasoning effectively to clients, they will be able to make an informed decision that takes their own values and priorities into account.

Next, remember that your message should be framed with and founded in hard data. This is especially important for investors who are wary of greenwashing or similar attempts to unfairly characterize the ESG ecosystem, either too positively or too negatively.

Finally, it’s essential to understand the effect and implications of ESG on various investment themes. Is your client concerned about the long-term viability of our planet? Are they particularly attentive to ethical issues around hiring, promotion, and diversity in a company’s leadership? Are they worried that particular technologies being touted as “sustainable” may be unproven and more subject to risk? Knowing what is most important or concerning to your client will enable you to position the discussion around ESG in a way that both supports your client’s goals and advances their understanding of the issues.

You don’t need to become an activist or evangelist for or against ESG. But regardless of where your opinions lie, this topic is not going away any time soon. The more prepared you are to discuss it intelligently and dispassionately with your clients, the better for your practice — and your clients.

Gretchen Halpin is co-founder of Beyond AUM, a growth, marketing and technology agency that specializes in serving financial advisory firms. A strategic visionary with over 25 years of leadership and marketing experience, including a history of starting and growing successful companies, Halpin pioneers the strategy and growth initiatives that drive success across every aspect of business while ensuring that decisions are aligned with her clients’ overall mission.