Taxes and healthcare tend to be the largest expenses that most people will pay in retirement.

Through its Medicare program, Congress has created the rare circumstance where the two are linked. The problem is, many seniors forget to think about these income drainers in tandem, particularly because of the “shadow taxes” lurking in the dark.

Income taxes get most of the focus when it comes to tax planning, but they’re not the only cost calculated from a taxpayer’s annual tax filing. Once a taxpayer participates in Medicare, their tax return is a key component in determining their income-related monthly adjustment amount (IRMAA). Or put more simply, their Form 1040 determines how much their Medicare premiums will cost.

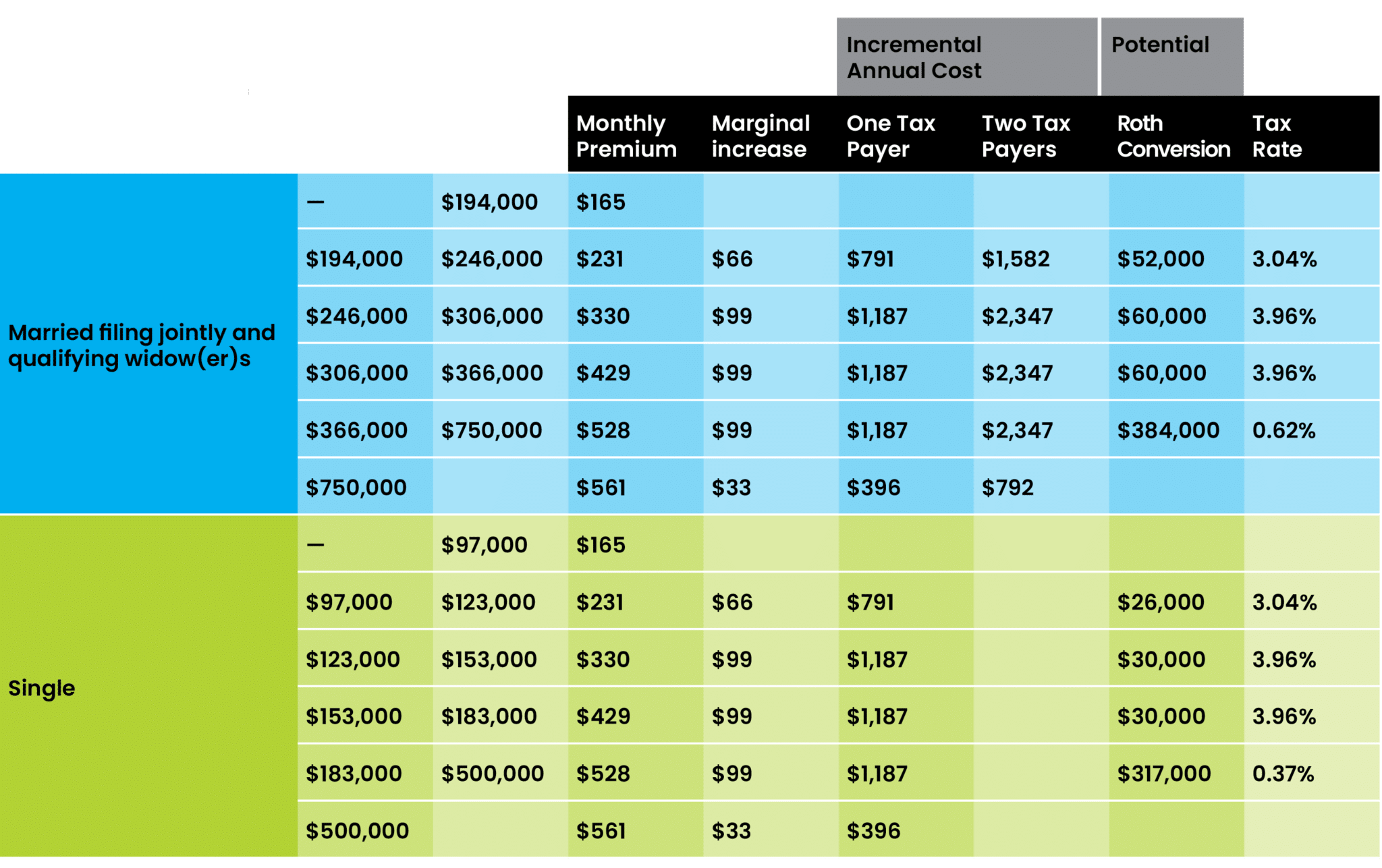

Medicare participants pay monthly Part B premiums (for doctor’s visits, preventative services and more) ranging between $164.90 and $560.50. While these numbers won’t show up on anywhere on their tax returns, each participant’s tax return is used to determine where they fall on that spectrum.

Specifically, a taxpayer’s modified adjusted gross income (MAGI) is used to determine which bracket they are in for establishing how much they will pay for Medicare Part B premiums (The same amount is used for Part D drug coverage premiums where applicable, but the dollar amounts of those premiums are significantly smaller and not our focus here). For most taxpayers, MAGI for purposes of IRMAA is simply adjusted gross income (AGI – line 11 of IRS Form 1040) plus tax-exempt interest (line 2a of IRS From 1040)

How much does the next $1,000 of income cost in taxes?

Advisors can add a lot of value by addressing this question, which essentially involves comparing a client’s marginal tax rate to the IRMAA brackets.

In 2023, the 22% tax bracket for couples who are married filing jointly ends at $190,750. This means that if your client has $190,250 in income and adds an extra $1,000 through a Roth conversion, for example, $500 of that income would be in the 22% bracket and only $500 would be in the 24% bracket. Crossing the line into the 24% bracket does not suddenly make all of their income subject to 24% taxes. In this case, that $1,000 of additional income would cost them $230 of taxes. Now let’s compare that to IRMAA brackets.

Medicare’s all-or-nothing increase

If both spouses in this example are on Medicare, their combined monthly premiums will be at least $329.80 ($164.90 per person, for a total $3,957.60 per year). That bracket ends when the couple’s MAGI exceeds $194,000. However, unlike the income tax brackets that change the amount per dollar of income that a person pays in taxes, the IRMAA brackets are all or nothing.

If our fictitious clients had $193,500 of income before completing a $1,000 Roth conversion, they would now be over the threshold and incur the entire additional premium cost of that next bracket.

The next bracket pushes their monthly premiums up by about $66 each, for a combined total increase of $1,582 a year. This means an extra $1,000 of income cost them $1,582 in additional “shadow” taxes for Medicare on top of $240 of federal income tax ($1,000 x 0.24). In other words, it cost the couple $1,822 to make $1,000 ($240 + $1,582). Although this might seem like an extreme example, it illustrates why it’s so important to pay attention to the details.

This is where the expression, “in for a penny, in for a pound” comes from. In contrast to income tax, which increases for each additional dollar of taxable income, Medicare premiums only change at the IRMAA threshold. At $194,001 the Medicare premium goes up and will not change again until the next threshold (currently expected to be $246,000). In other words, as soon as you cross a threshold you’ve already “paid” for the entire range, so may as well use it.

Charitable exception

Most people understandably are interested in ways to lower their taxes, including shadow taxes like IRMAA. Since MAGI is pulled directly from Form 1040, similar logic applies to lowering MAGI as would apply to lowering taxable income, with one exception: Donor-advised funds (DAF) have no impact on MAGI. This may feel obvious if you are well versed in tax law, but it gets missed all the time.

A DAF may still be a great planning tool for taxpayers who are charitably inclined to help reduce their income tax burden, but it’s important to understand that it will not impact MAGI. For taxpayers over age 70 ½, qualified charitable distributions (QCDs) are an alternative giving strategy that will both reduce taxable income and MAGI.

The confusion might come from the fact that qualified charitable distributions (QCDs) have the added bonus of being deducted from income before MAGI is determined, but this is not true for donor-advised fund (DAF) contributions. DAF contributions are a deduction on Schedule A, which reduces taxable income, but not adjusted gross income or modified adjusted gross income.

Roth conversions and IRMAA

If taxpayers get all of their tax planning advice from the news, social media or, even worse, TikTok, they could easily be under the impression that IRMAA puts a hard stop to any Roth conversions. This simply is not the case.

Yes, IRMAA can add to the cost of completing a Roth conversion but it should be a consideration, not a roadblock. What most commonly gets left out of the discussion on “IRMAA is the death of Roth conversions” is the actual dollar amounts we are talking about. So, let’s do the math.

The key to focus on is the additional cost of the Roth conversion if it pushes a taxpayer into a new IRMAA bracket. We’ve included the math in the table below, but let’s walk through a specific example.

For a couple that is married filing jointly and earning $194,000, the next dollar of income will push them into a new IRMAA bracket and cost them an additional $1,582 in premiums for the year. We discussed that marginal increase above. However, that bracket can hold an additional $51,999 of income before the next bracket is tripped. So whether this couple bring in another $1 of income or the full $52,000, their Medicare premium increase will be the same.

Maximizing the bracket (being “in for a pound”) means that a $52,000 Roth conversion would cost an additional $1,582 beyond the income tax ($11,440 at 22%), or increase the total “tax rate” (income tax and IRMAA premiums) on the conversion by 3 percentage points. We already know that the 22% bracket will rise to 25% (3 percentage points) in 2026, so the income tax portion of a future distribution goes up before IRMAA is even considered. Which makes the argument to go ahead and do the conversion a lot simpler.

This is assuming that before the conversion we hadn’t tripped any IRMAA brackets. If before the conversion the client was already at $194,001 of MAGI, then the $1,582 in premiums has already kicked in and IRMAA is not impacted at all by the next $51,999 of Roth conversions. In that case it is strictly back to your overall strategy with the client based on their expectations for tax rates increasing in the future and their tax tolerance for dealing with some of that unknown now.

By reviewing the table, you can see that there is a real cost to each bracket but it is not prohibitive. Just like converting to a Roth can lower required minimum distributions (RMDs) and therefore lower marginal tax rates in the future, that same reduction in income can help a client stay in lower IRMAA brackets in the future as well.

IRMAA might feel scary and unknown, but taking the time to understand what’s involved is yet another way you can help clients. You can help them understand their tax position now and what it will likely be in the future. Most important, you can show them if there are actions they can take to make sure they stop tipping the IRS over the lifetime of their wealth.

Roth conversions (and all tax planning) should be applied to specific client situations. It’s also crucial to have real data and to make informed recommendations, including when IRMAA is involved.

Steven Jarvis, CPA, MBA, is cofounder ofRetirement Tax Services,which offers year-round tax services to financial advisors and their clients. Retirement Tax Services will host “The 2023 Next Level Tax Planning Summit” on Sept. 27-29 in Las Vegas (virtual option also available).