Is your business driven by your client base or does your business plan drive your client interactions?

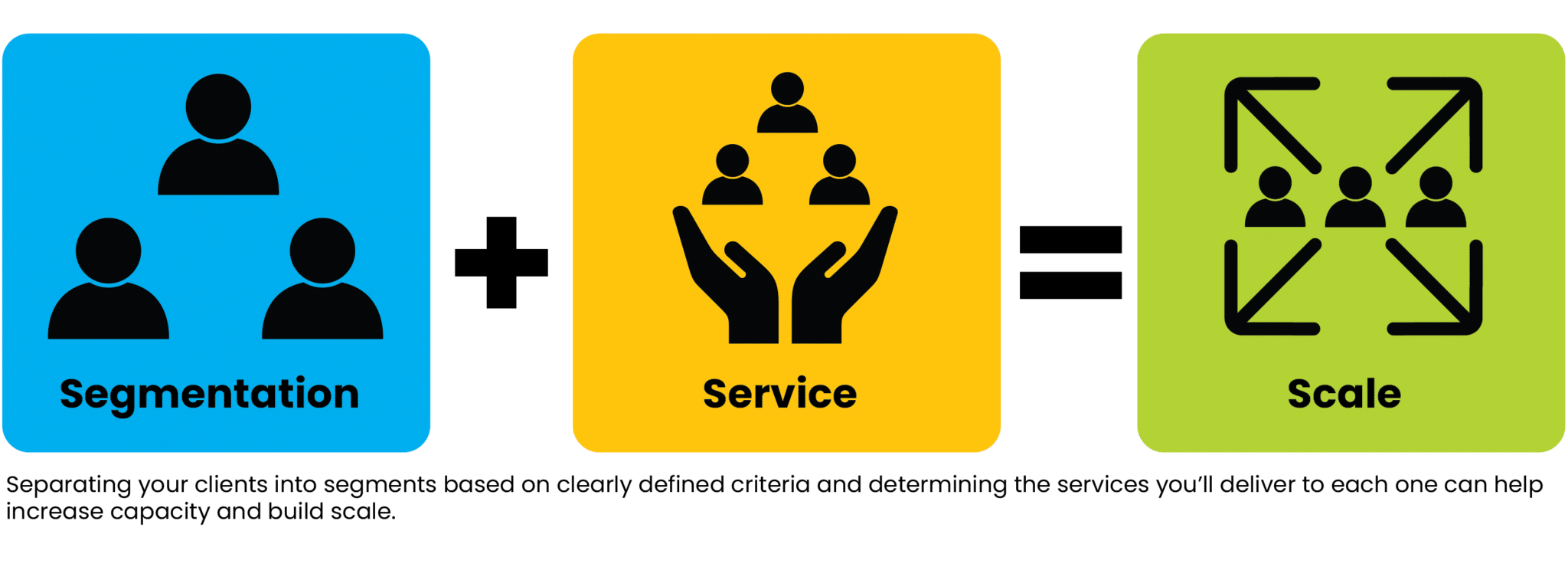

When advisors start out, they tend to bring on a wide variety of clients to get their business up and running. But as your business grows, your organization, services, and client base may need a more strategic approach to evolve along with your business. Building a model for client segmentation and service can help you focus on developing the right services for the right clients and create a business structure that will nurture your firm’s success and growth.

Examining Your Book of Business

The first step to establishing a model for client segmentation and service is understanding the structure of your current client base. Make the review both quantitative (e.g., assets under management and revenue generated) and qualitative (e.g., level of trust, coachability, and referral history).

Next, think about the services your clients use. Do they all receive the same services — say, financial planning, annual reviews, regular outreach, and invitations to client events? (Hint: If your answer is yes, change could be coming!)

Creating a Strategy for Client Segmentation

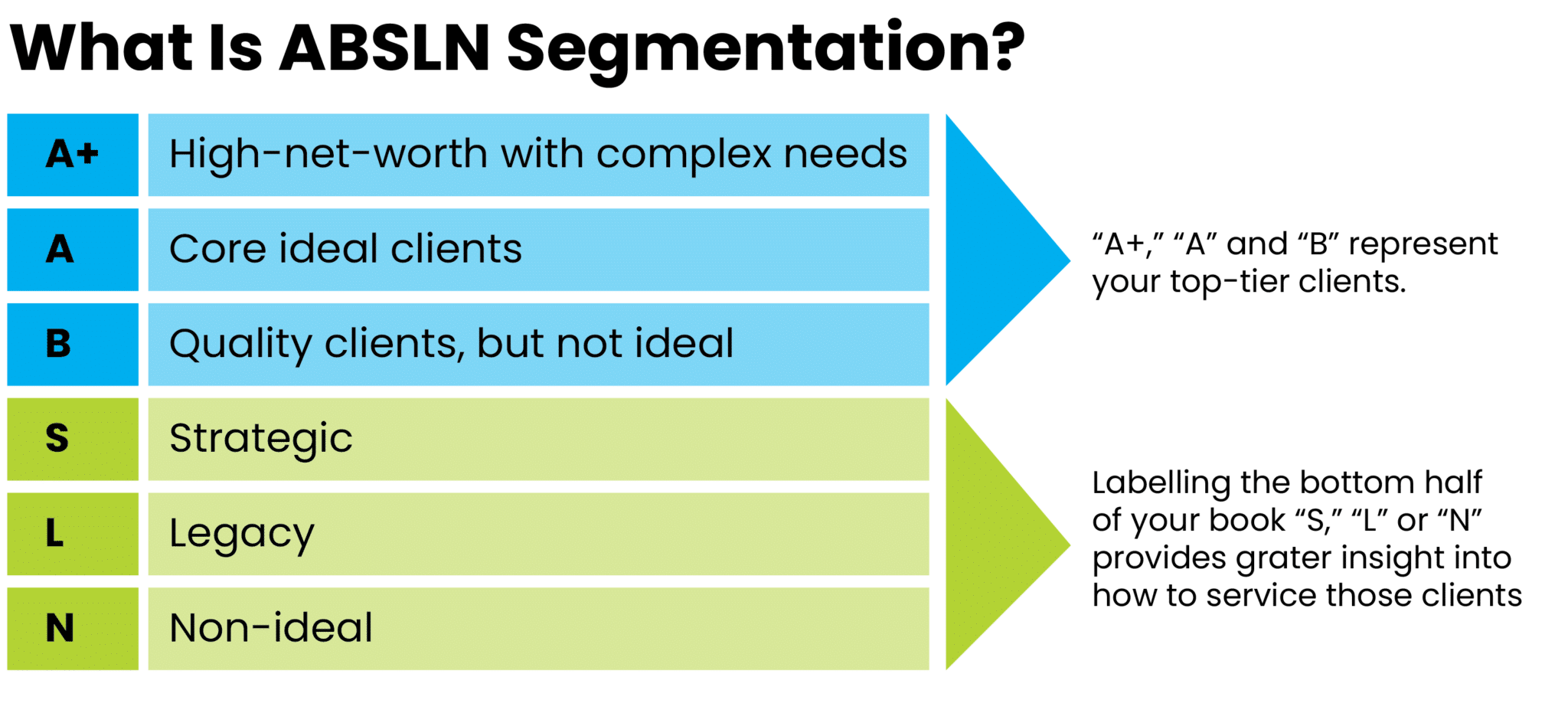

Once you understand the details of your current client breakdown, you can start categorizing your clients and services. You may be familiar with the segmentation approach that places clients into categories labeled “A,” “B,” “C,” or “D” based on either revenue or AUM. This quantitative approach helps identify your most profitable clients, but chances are, you already know those clients well. What about the rest of your book? Our Business Consulting team often recommends a more holistic segmentation method called the “ABSLN” method.

With the ABSLN segmentation method, you still identify your top clients as “A+,” “A,” or “B” based on the revenue they generate for your firm. And for the other tiers, you’ll use qualitative criteria to place clients into segments labeled “S,” “L,” or “N.”

S/Strategic: Individuals in this tier have the potential to become top clients. Consider young, high earners with strong savings and business owners with illiquid wealth.

L/Legacy: These clients may have a legacy relationship that justifies providing continued service — for example, A client’s children, widows or widowers, or personal friends.

N/Non-ideal: These clients don’t fit into any other segments. Consider continuing to offer service, transferring them to a junior advisor, or discontinuing your relationship.

Using ABSLN segmentation gives you deeper insight into the categories of clients currently in your book so you can align services properly.

Partnering Segmentation with Services

Once you’ve completed your client segmentation, you can build your service model and identify the type and frequency of services you’ll deliver to each segment.

Consider these factors:

Service-level suitability

Create service levels that deliver a consistently outstanding experience for clients but allow you to focus the right amount of time on A and B clients.

Profit potential

Prioritize your time to focus on segments that generate significant revenue and allot less time to those that don’t.

Long-term suitability

Determine the time required to deliver services, being sure to factor in time for business development and practice management activities.

Outsourcing options

The right firm partner can suggest options for delegating certain tasks. Look for a partner that can optimize efficiency through a range of outsourced business solutions.

Client book assessment

Identify the clients that don’t fit in these segments and, if possible, transition them to an advisor who might be a better fit.

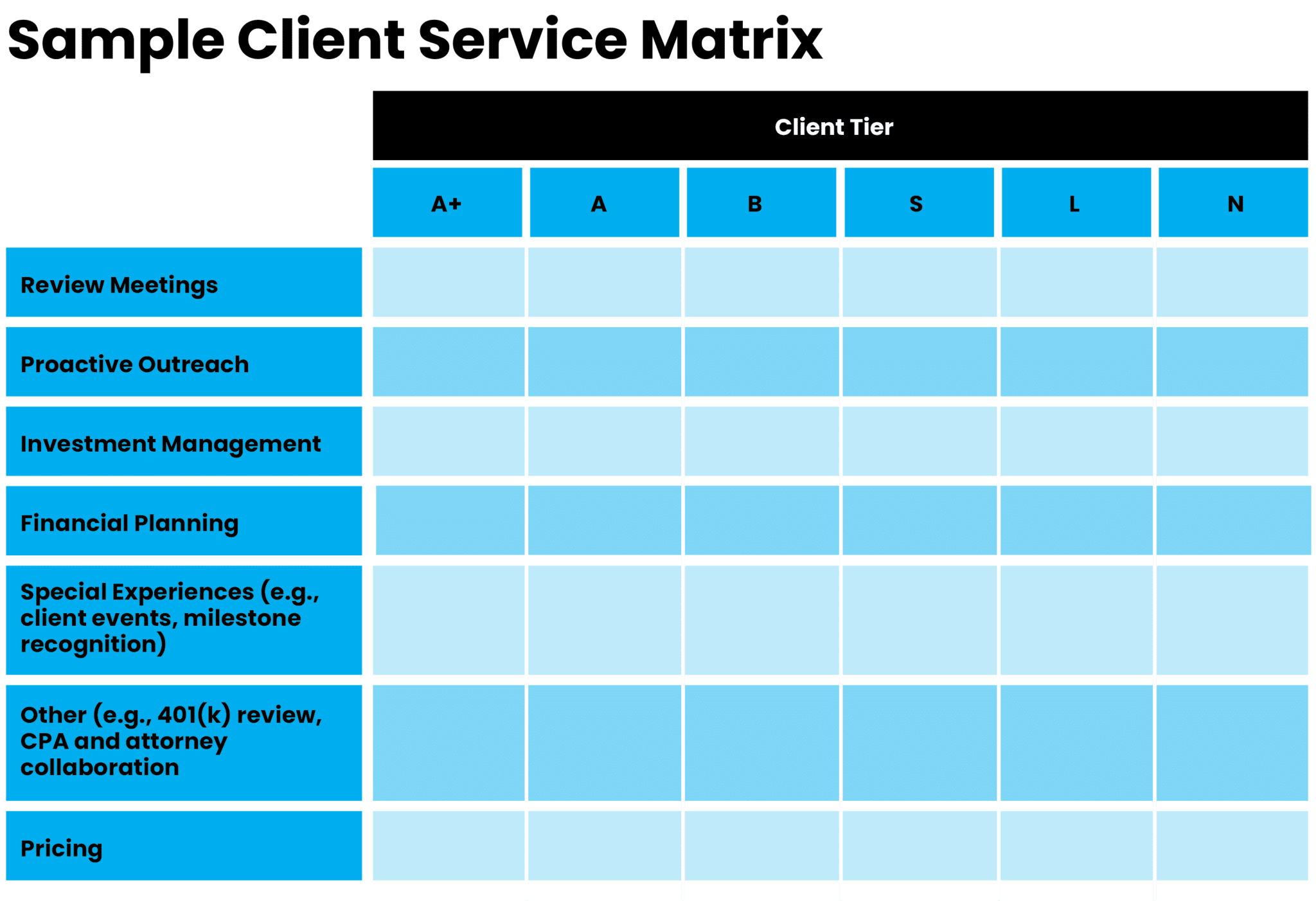

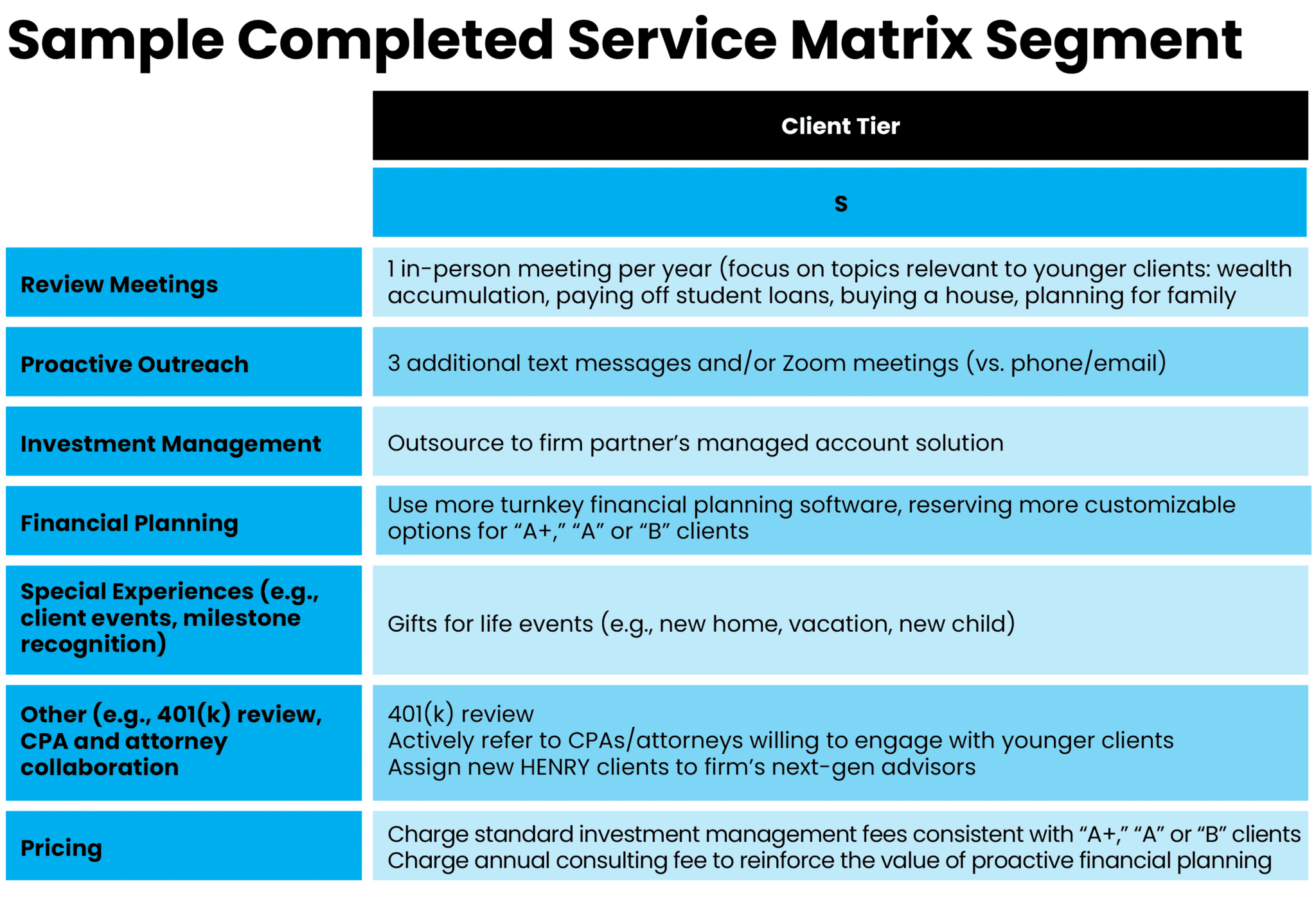

You can document your results in a structure similar to the chart below, with services on the left and service tiers on the right. If the amount of time spent delivering service in each client category doesn’t align with the average revenue the category earns, you may need to adjust.

Consider the following:

Do you need to revise any business processes or workflows?

Example: If you meet with B clients less often, consider adjusting your scheduling process.

What training could help team members adapt to process changes?

Example: Your team should understand how to onboard clients at all tier levels.

How will you communicate the new model to affected clients?

Example: If you’re outsourcing investment management for your “strategic” clients, be ready to share why you feel it’s the right move for them.

How will you manage future business development and referrals that don’t quite fit your new model?

Example: Establish referral relationships with other advisors who might be a better fit in these situations.

How will you communicate your new approach to your firm?

Example: Depending on your CRM system, you may be able to set up workflows to reflect changes in each client’s record.

By connecting each area of the business with your new service model, you’ll position yourself better to attract aligned clients and scale your business.

Ready for a Change?

Intentionally establishing a model for client segmentation and service helps you control the direction of your business growth. And strategizing ahead of time lets you focus your energy where you need it most. You’ll be able to manage more relationships and support increased revenue with fewer resources, which means more and better-supported clients as well as higher income for your business.

This post originally appeared on Insights, a blog authored by subject matter experts at Commonwealth Financial Network®, Member FINRA/SIPC, a Registered Investment Adviser.

With the ABSLN segmentation method, you still identify your top clients as “A+,” “A,” or “B” based on the revenue they generate for your firm. And for the other tiers, you’ll use qualitative criteria to place clients into segments labeled “S,” “L,” or “N.”

With the ABSLN segmentation method, you still identify your top clients as “A+,” “A,” or “B” based on the revenue they generate for your firm. And for the other tiers, you’ll use qualitative criteria to place clients into segments labeled “S,” “L,” or “N.”