Demand for financial advice is growing, largely because most employers over the past 20 years have flipped their responsibility for pension savings to their employees.

Corporations have moved their pension programs from defined-benefit to defined-contribution plans, leaving employees on their own to make investment decisions, said Gregory Calnon, global head of multi-asset solutions for Goldman Sachs Asset Management (GSAM).

“Plan participants are dealing with very high market volatility, higher inflation than usual, potentially lower investment returns, and, thankfully, longer life expectancies,” Calnon said. “But that is a challenging mix for individuals to have to navigate.”

He and other experts spoke at GSAM’s recent webinar, “Navigating the Financial Vortex.”

Gen X, the first generation fully affected by reliance on defined-contribution pensions, like 401(k)s, most often reported being very unprepared to retire, according to GSAM’s annual retirement survey, which was released in mid-October.

Baby boomers felt almost as poorly prepared, the survey showed. Those two generations comprise ages 42 to 76.

Shorter runway

Events have “shortened the retirement runway” for many boomers, said Michael Moran, GSAM senior pension strategist.

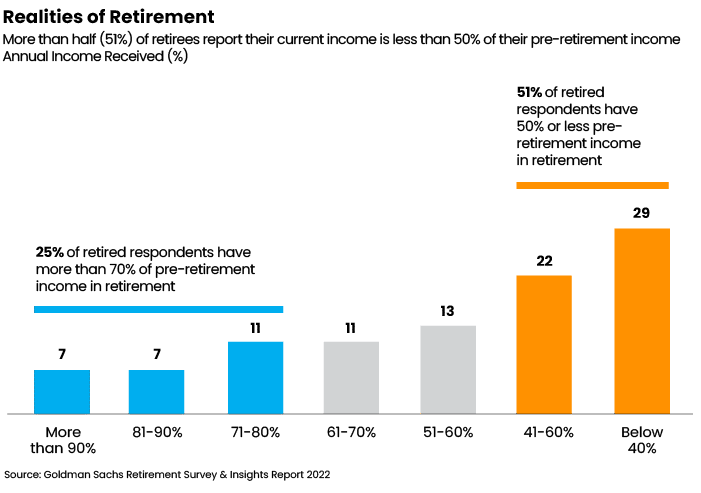

The survey found more than half of working boomers and Gen Xers aren’t saving enough for retirement, and about half of the retired boomers had to leave the workforce earlier than planned and now live on less than 50% of their last regular paycheck.

It was Gen X and millennials, ages 26 to 57, who the survey found put the highest value on personal investment advice.

“The first lesson (of the survey) is not only do employees need help, but they’re looking to their employers for that help,” Moran said. “Employer programs to help employees save for retirement is not a nice-to-have; it’s a need-to-have … especially in a world where workers no longer have that protection in a defined-benefits pension plan.”

The second lesson, he said, is that the added stress that this financial burden puts on employees causes higher absenteeism and lower productivity.

The 58% of all workers who reported being stressed by investment decisions spiked to 65% for Gen X, ages 42 to 57, among the 967 workers in the survey.

Keys to the financial car

With employers shifting investment decisions to workers, more people are looking at their entire portfolios for both appreciation and income generation, said Joe Duran, head of Goldman Sachs Personal Financial Management.

“You have to think of every individual like they are running their own pension plan,” he said.

“It has been very hard for people to have enough saved to generate replacement income, especially with interest rates where they were two years ago,” Duran said.

But now, “for first time since the 1930s, a 60/40 portfolio has gone down both in the equity and the fixed income, which is very rare, about 3% of the time,” he said.

Because fixed income has done so poorly, almost everyone with a 60/40 portfolio is now looking at a 20% decline, he said.

Clients near retirement may need to look at choices besides investing.

For example, clients near retirement could work an extra 18 months to get their portfolios back to where they were, Duran said. Retired clients could do the same by reducing spending by 10% for four years, he said.

People need financial advisors “to walk you through, so you don’t make any panic moves, because you’re not a pension plan. You’re an individual, with all kinds of unforeseen circumstances,” Duran said.

“The most important thing is to make sure your emotions don’t overwhelm calm and objective decision-making,” Duran said.

Reality check

Current market conditions aren’t the only reason to look at investment assumptions and projections, Moran said.

Another finding in this year’s survey was that most millennials and Gen Zs expect to retire at age 60 to 64, and some even before age 60. Although many baby boomers retired earlier than they had anticipated and before the traditional age 65, most were forced into early retirement by layoffs, health problems including Covid-19, and family caregiver demands — reasons outside their control. Gen Xers still expect to retire in their mid- to late-60s.

“There needs to be a … reality check in terms of when you think you actually are going to retire,” Moran said.

Despite current economic challenges, the younger generations surveyed were notably optimistic that their retirement plans were in good shape.

Retirement readiness changes over time, and life events force recalibration, Moran said.

“As life goes on, more financial priorities come into play,” he said. “As life happens outside of your control, you have to be able to adjust your savings strategy.”

Duran agreed: “You don’t know what you don’t know … until you’re at that vortex” of tutoring, sports, parent care and other obligations. Almost everyone is at a point where they are going to have to give up on one dream they had or sacrifice it in some way.”

Understanding how you’re going to do that is the trick, “especially if you’re in a relationship,” he said. “My wife and I have been married for over 30 years, and we each have different opinions about what that right way is.

“Working with an objective advisor will help you to balance the tradeoffs, because there will be tradeoffs in almost all circumstances, because you can’t have it all,” Duran said. Investing advice “has to be personal, because everyone is different in what they prioritize.”

Retirees have fewer choices, beyond reduced spending or taking on part-time jobs. But, for workers, small matters of timing — for travel, home-buying or adding to the family — can have big effect, the experts said.

“I wish that the younger generations weren’t so optimistic, because that’s when they have the biggest window to make the biggest impact on their choices for the future,” Duran said.

Bottom lines

Discipline to the fundamentals is even more important in today’s less predictable economy.

Duran said he advises working clients to “max out the easiest savings that you can.” That means to contribute at least as much as the employers’ match to a 401(k).

“The reality is that once you have children and a spouse, things become more predicable about what the future looks like to make reasonably good assumptions about future liabilities,” he said. “Any chance to expand your asset options is a bonus at any age.”

The purpose of a financial plan isn’t to conform religiously but to give clarity of purpose, Duran said.

“Even though that plan will be wrong the day it’s written, because you cannot predict the future, it gives you some sense of action you should take … and gives you some sense of control, which is important to every individual.”

Linda Hildebrand is a longtime newspaper editor and consumer-action reporter.

It was Gen X and millennials, ages 26 to 57, who the survey found put the highest value on personal investment advice.

It was Gen X and millennials, ages 26 to 57, who the survey found put the highest value on personal investment advice.