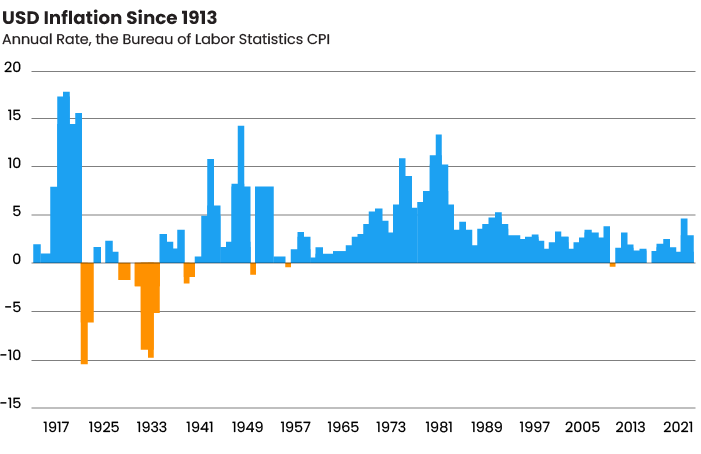

That question might make me sound like an alarmist, but we owe it to our clients to consider this possibility. Inflation is now higher than it’s been in 40 years, and most current retirees remember long gas lines, stagflation and Paul Volcker. A look at the annual rate of inflation since 1913 shows how unstable prices were before the 1990s.Let’s look at how advisors should consider investment allocations for higher inflation and discuss other ways to help improve outcomes for retirement income strategies.

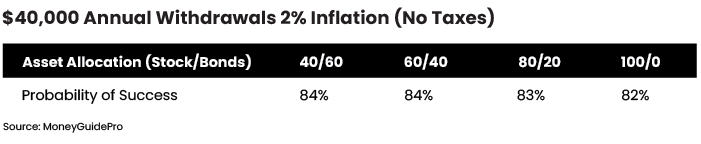

Using the 4% withdrawal rule, most investment allocations work when inflation is only 2%. Here are the results from a Monte Carlo simulation from MoneyGuidePro, assuming a $1 million portfolio and $40,000 annual withdrawals (increased for inflation) over 30 years.

At low inflation, allocations from 40% stocks to 100% stocks all produce a probability of success of 82%-84%. A result of 75%-90% is considered in the confidence zone. At 2% inflation, even a 60% allocation to bonds can work because the projected return for bonds is 3.05%. (Granted that is not the current rate on an intermediate bond index, but rates are expected to rise, giving room for a better 30-year projected return.) While higher equity allocations offer a larger expected return, they also introduce more sequence of returns risk. So, the probability of success does not increase with a higher equity allocation.

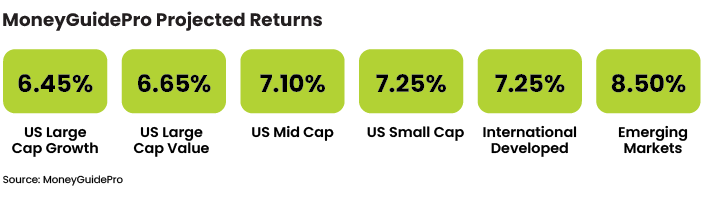

Today’s projected returns are much lower than historical. MoneyGuidePro offers both historical and projected returns. The results in this article are using the projected returns, as calculated by Harold Evensky for MoneyGuidePro. Not surprisingly, as inflation rises, bonds fare worse than stocks. The higher expected returns of equities are needed to allow for retirement income to keep up with higher inflation.

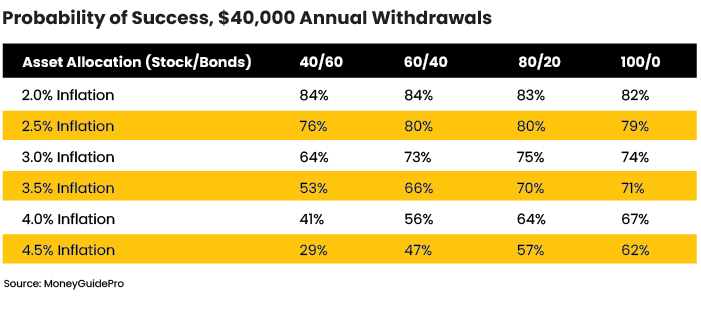

A 40/60 portfolio has an 84% probability of success at 2% inflation, but this falls to 29% at 4.5% inflation. Compare that to the 100% equity allocation, which has an 82% probability at 2% inflation and still has a 62% probability at 4.5%.

For advisors planning for today’s retirees, you should consider carefully how inflation could impact a portfolio’s ability to provide sustainable withdrawals. At the 2% inflation we’ve enjoyed in recent years, asset allocation did not make much of a difference to the sustainability of income. And while no one can predict with certainty what inflation will actually be over the next 30 years, it may be worth considering if increasing your allocation to equities may be necessary for higher inflation ahead. Perhaps 80/20 should be the new 60/40 for retirees.

Although equities improved the probability of success, we should note that at 3.5% and higher inflation, no allocation had a score above 74%. With a confidence zone of 75-90%, these are less than ideal outcomes. This suggests that we may want to either start with a lower withdrawal rate than 4% or have in place a flexible withdrawal strategy that adjusts income based on returns.

Five Ways to Improve Income Under Inflation

1. Social Security. With Social Security providing annual Cost of Living Adjustments (COLAs), it may be preferable for investors anticipating higher inflation rates to defer starting SS benefits to receive a higher monthly amount. Delayed Retirement Credits are 8% a year, plus the Primary Insurance Amount (PIA) is increased for COLAs. Spending down low-yielding assets to defer Social Security can improve the probability of success.

2. Inflation and Bonds. TIPS (Treasury Inflation Protected Securities) have seen strong interest in the past year and have performed much better than regular Treasuries. Unfortunately, TIPS are priced at negative real yields. For example, the iShares TIPS ETF (TIP) presently has a yield of -1.12%, meaning the return will be 1.12% less than inflation. That might be better than regular treasuries, if inflation proves higher than expected. However, you are guaranteed to not keep up with inflation, which is disappointing for a bond that was supposed to maintain your purchasing power.

Today, a better solution than TIPS might be I-Series US Savings Bonds. I-Series allow investors to receive all of the return of the CPI, not the negative real return of TIPS. Unfortunately, there are challenges with I-Series, including an annual purchase limit of $10,000 a person. They can only be purchased from TreasuryDirect.gov and cannot be held in a brokerage account or IRA. Still, for investors who want to have their bonds be guaranteed to keep up with inflation, replacing $10,000 a year of nominal bonds with I-Series may be appealing. Couples, of course, can purchase $10,000 each.

Additionally, long-dated TIPS carry interest rate risk — the premiums above par today can erode as rates rise, creating losses in bond price. Not so with I-Series, which are purchased and redeemed at par. I-Series bonds adjust their coupon every six months and accrue interest for up to 30 years. Investors can sell anytime after 12 months, but will incur a penalty of the previous 90 days’ interest if they sell before five years.

3. Focus on total return, not yield. Many retirees think that the best way to create income is through high-yield strategies or dividend-paying stocks. And while many companies do provide a rising dividend yield, income-oriented portfolios can be less diversified and introduce additional risks to investors. Often, these portfolios underperform a diversified, low-cost, index portfolio over a period of years. Instead, advisors might want to tilt equity allocations towards areas of higher expected returns. While many have enjoyed excellent returns from having a home bias, U.S. stocks are much more expensive than international and growth is more expensive than value.

By considering expected returns, we look forward at valuations rather than backward at returns. Evensky created the long-term projections below based on his calculation of the equity risk premium and the current risk-free rate. He uses the Capital Asset Pricing Model, or CAPM. The calculation of average returns is based on what might happen over many years.

A total world stock index today has 59% US stocks and 41% international. This is up from 55/45 in just two years. A portfolio with less than 41% in international has a home bias, which may underperform if you consider the projected returns.

4. Don’t Increase Withdrawals. In theory, clients need to increase spending annually to keep up with inflation. In practice, none of my clients do this. Most of my clients either take fixed monthly withdrawals (i.e. $3,000 a month) or they just take their RMD each year. None have asked me to increase their withdrawals by 6.8% for 2022 because of the most recent CPI numbers.

I don’t mean to suggest this is a permanent solution — most will need more income at some point. Still, advisors should consider how much of the retiree’s income is subject to inflation (food, utilities, etc.), versus how much is fixed (mortgage). Also, how much is discretionary versus required spending? A client who is living on $1,500 a month probably has very little discretionary spending and will need to adjust for inflation. A client who is taking $15,000 a month in withdrawals may have significant discretionary spending and be quite comfortable with not increasing their income for inflation each year.

5. Rising Equity Glidepath. Most retirement income plans assume annual rebalancing to maintain a target asset allocation. While this has benefits of maintaining a set risk profile and buying low/selling high, rebalancing may be better for asset accumulation than retirement income.

An alternative to annual rebalancing is the rising equity glidepath, where retirees hold on to stocks and sell bonds to meet their income requirements. This allows retirees to enter retirement conservatively, perhaps only 30%-50% in stocks. This can reduce sequence of returns risk because they will not need to sell any stocks for 10, 15 or more years. During that time, the equities may have the chance to double or more.

While it is certainly unconventional to suggest that an 80-year-old move up to 70%, 80% or more in equities, does the rising equity glidepath work? According to research by Wade Pfau and Michael Kitces, “rising equity glide paths appear to maximize the likelihood of success and sustainable income, and reduce the magnitude of shortfalls when they occur.” While they held inflation as a constant in their study, a rising equity glidepath may offer a smoother retirement income outcome than entering retirement with a high equity allocation and rebalancing annually.

While no one knows future inflation rates, advisors creating retirement income plans should consider its impact on sustainable withdrawals. Monte Carlo analysis suggests that higher equity allocations have a higher probability of success than bond-heavy portfolios under higher inflation. Of course, equities introduce more volatility, and a high allocation to equities may be unappealing to many investors. Planning for inflation, advisors can consider increasing equity allocations, starting with lower or flexible withdrawal rates, and implementing the five ideas we discussed.

Scott Stratton, CFP, CFA, is the managing member of Good Life Wealth Management, a Registered Investment Advisor in Little Rock, Arkansas. You can reach Scott at Scott@GoodLifeWealth.com.