There is perhaps no better illustration of the power of wealth planning than when we conceive new ways to help clients meet their life goals.

At our firm, a married couple recently presented us with a challenge: The “Smiths” were ready to retire and had not performed planning for their $50 million estate. The bulk of their assets were concentrated in appreciated, income-producing real estate. These elderly clients relied on the income from the properties to support their lifestyle.

The Smiths were reluctant to simply divide the properties among their heirs that included children and grandchildren. The couple feared their family would lack the expertise to manage the properties and perhaps quarrel over them.

We worked with the Smiths and identified their priorities: Simplify the estate by divesting the properties, diversify their portfolio, receive an income stream, and leave a maximum of $5 million to each of their six children. Diversifying their holdings would mean realizing substantial gains and depreciation recapture. They were averse to the income-tax consequences of selling and expressed interest in philanthropy to the extent that it could mitigate income taxes.

An Attractive Vehicle

Our team at Robertson Stephens recommended that the Smiths utilize a type of charitable remainder trust known as a CRUT (short for charitable remainder unitrust). This irrevocable trust pays an income stream to the grantor or a beneficiary of the grantor’s choosing, and then passes the remaining assets to a charity at the end of the trust’s term. For the CRUT to obtain charitable status, the remaining assets must be equivalent to the charitable deduction taken and 10% of the initial funding amount.

The CRUT was an attractive vehicle for our clients because the assets are designated for future charitable giving and produce annual income. The Smiths determined the percentage of the trust’s fair market value to receive as an annual distribution.

Distributions to the income beneficiaries of the CRUT are taxed on a “worst-in, first-out” basis. This means that the CRUT first distributes ordinary income, then capital gains, then other income, and finally principal.

For real estate owners, spreading out the realization of capital gains is key — especially because some gains can be taxed at less favorable rates due to deprecation re-capture. The benefit here would be twofold: deferral of capital gains tax and an income tax deduction.

Our team worked backwards to determine the value of property that should be donated to the CRUT. Donations of appreciated property qualify for a charitable deduction but are limited to 30% of the clients’ annual adjusted gross income (AGI). Federal tax rules allow clients to carry the charitable deduction forward for five years. Using the Smiths’ 2020 AGI, we calculated that five years’ worth of charitable deductions totaled approximately $1.3 million.

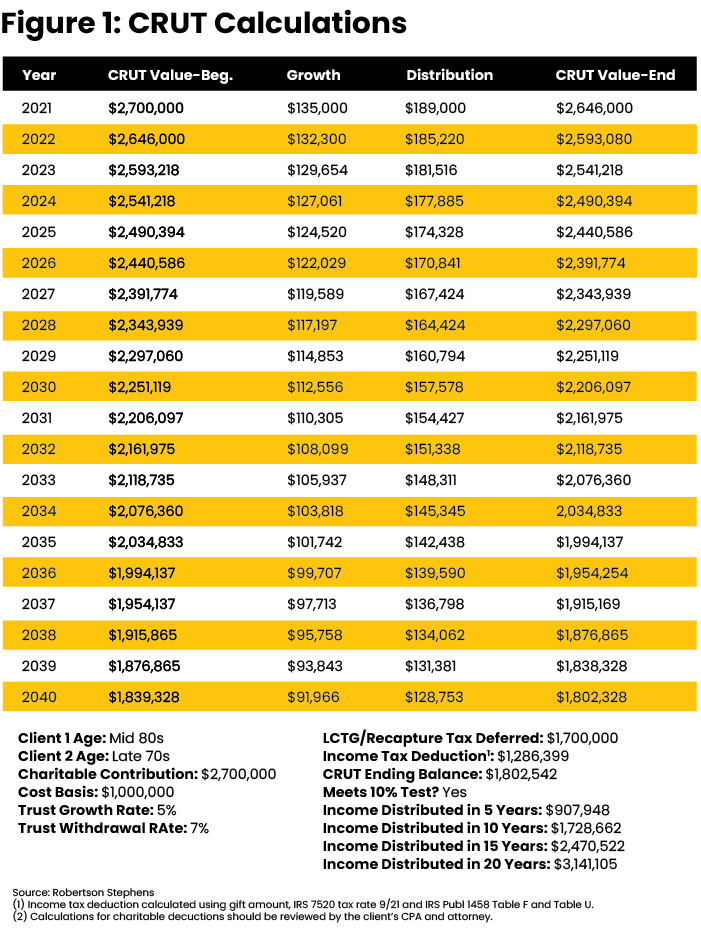

We prepared estimates for the Smiths and asked their accountant and attorney to review. Our model projected a two-life CRUT with the following characteristics: a transfer of appreciated real estate valued at $2.7 million with a $1 million cost basis, a payout rate of 7%, and assumed an investment growth rate of 5% within the trust.

The value of the Smith’s charitable deduction was approximately $1.3 million, which they could spread over five years while receiving roughly $900k in income from the CRUT (Table 1). During the first five years of the CRUT term, the Smith’s income from the trust would be covered by their charitable deduction. Additionally, $1.7 million in capital gains and depreciation recapture would be spread out over the term of the trust.

To determine which properties were the best candidates to transfer to the CRUT, we considered several factors such as outstanding debt, depreciation subject to recapture, net income, and the client’s preference for holding rather than selling the properties.

An encumbered property is not recommended for a CRUT because debt-financed income could be classified as unrelated business taxable income (UBTI), which incurs a 100% excise tax in charitable trusts. Therefore, we eliminated any properties from the list that carried a loan.

Next, we evaluated depreciation recapture. Depreciation on real estate may be recaptured as ordinary income though it depends on the type of property. Since income would be taxable to Smiths over time, depreciation recapture could be spread out. Therefore, a property that would have recapture upon sale could still be a good candidate for a CRUT. We did not eliminate properties purely based on recapture.

The Smiths have been using the income from their real estate portfolio for their living expenses. They understood that the CRUT could make up for some of that income once the properties are sold within the trust and the proceeds are reinvested. However, they wanted to retain several of the highest-income properties to fund their lifestyle. Therefore, we eliminated properties from consideration that produced the highest net income. Lastly, we considered the couple’s preference for which properties they would like to hold and manage.

A common type of CRUT used for appreciated real estate is a FLIP CRUT, for which the trustee is not forced to make a trust distribution unless there is actual trust income. We recommended a FLIP CRUT to the Smiths and suggested three properties to transfer into trust: A beachfront condo in Miami, a multifamily apartment in Chicago and a five-bedroom vacation home in Galveston, Texas. Follow-up involves coordinating with their accountant and attorney, selecting a trustee, and managing the investments of the CRUT once the properties are sold inside it.

By funding a CRUT with appreciated real estate, the Smiths sought to reduce the complexity of their estate, mitigate income taxes, and provide an income stream that would last after the properties were sold. Furthermore, by making a bequest to charity, they hoped to leave an additional legacy.

For clients who are direct real estate investors and want to divest and diversify their assets, the CRUT offers tax mitigation, income distributions, flexibility, and opportunity to donate to charity. Many variables must be considered to achieve the most beneficial solution. The illustration above may not be representative of the experience of other clients and is no guarantee of future performance or success. We recommend working with an experienced team consisting of a planner, a CPA and an attorney.

Mallon FitzPatrick, CFP, is a principal and managing director at Robertson Stephens and heads the firm’s financial planning center. Alicia Denton, CFP, is an associate wealth planner at Robertson Stephens. For more information about Mallon, Alicia or Robertson Stephens, please visit www.rscapital.com or email info@rscapital.com. Advisory services are offered through Robertson Stephens Wealth Management LLC. Opinions presented are those of the author and not necessarily Robertson Stephens.Please read Important Disclosures.