In Laura McDowell’s family, money and investing really were not topics of conversation for her parents, an educator and a warehouse manager. But they did pass on a strong work ethic.

“I worked from the ripe old age of eight,” the one-time vocal studies major and intern for the United Nations office on the Status of Women recalled.

And that ethic has served her well in her career in finance, McDowell told the audience for “Enhancing Her Client Experience: Strategies for the Women’s Wealth Evolution.”

McDowell, a CFP, CIMA and AIF, is now the Western Regional Director-RIA Channel for Charles Schwab & Co., Inc.

In the webinar presented by the National Association of Personal Financial Advisors, she spoke on a topic she is passionate about – encouraging financial advisors to seek out more female clients, and to find the best ways to engage with them and help them reach their life goals.

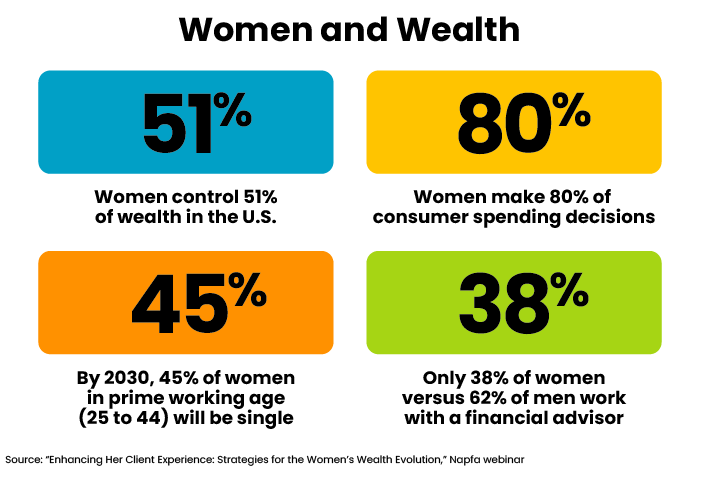

Setting the stage for this discussion were some statistics from McDowell about women and wealth: Women control 51% of personal income in the U.S. They make 80% of consumer spending decisions. And by 2030, 45% of women in prime working age (25 to 44) will be single. [Editor’s note: 49% of U.S. women 65 and older are currently single, according to Pew Research.]

So McDowell urges financial advisors to make a dedicated effort to attract more women as clients. Only 38% of women versus 62% of men work with a financial advisor, she noted. And surveys of the values men and women seek from investing also show a divergence. Men tend to be less risk averse, for example, she said.

Engaging Successfully with Female Clients

She offered some suggestions for financial advisors to consider:

Adjust your “cognitive framework” in dealing with women clients. Women respond to a welcoming, relatable conversation and have a more “values-based” framework about investing compared with male clients.

Women attach as much weight to process, service and connection with their advisor as they do to returns, she said. For example, storytelling and sharing experiences are good ways to make this connection. A client who may have been widowed could relate to an advisor who has some experience with personal loss, for example.

Women are busy. Most describe themselves as “time-poor” rather than poor in finances, McDowell said. So offer practical ways to meet — maybe after dinner when they have more downtime or meet at their place of business.

Women expect expert leadership. “Draw on all your planning and portfolio skills,” McDowell said.

In approaching ways to expand your base of women clients, McDowell said visualization helps. “Think about your ideal female client. Give her a name, an occupation, personality traits.” Advisors should think of the person’s demographics and their stage of life as part of how to “Choose Your Who,” the title of one of the segments of her talk.

In consultations, the client responds better to discussing “holistic” rather than transactional services. Uncovering the client’s key needs is part of this practice. It might be more valuable to consider your female clients in terms of life stage rather than finances, for example, because women tend to experience similar situations at various points in their lives regardless of wealth.

“It might be more valuable to consider your female clients in terms of life stage rather than finances, for example, because women tend to experience similar situations at various points in their lives regardless of wealth.”

– Laura McDowell, Charles Schwab & Co.

Another idea to encourage bonding with female clients is to create education sessions geared to their needs. Even something as small as offering a meaningful, personal gift such as a book can cement a shared bond, she said.

Presenting Your Services

McDowell suggested making an online search of “financial advisors near me.”

“You should come up first,” she said, and financial advisors should work on their websites to optimize their online presence.

The content on your website should make prospective women clients feel comfortable. Use images that reflect the women you serve and be inclusive and gender balanced. Don’t assume all women have a husband or children. Frame questions in a way that is open-ended and that leads to a more expansive conversation rather than assuming a set of circumstances for a new client.

Making a relationship with a client work takes insight into your own body language, McDowell said. When advising a married couple, do you primarily make eye contact with the husband? If so, make a conscious effort to look at both partners — and speak to both partners.

In a segment called “Work Your Book,” McDowell advised that in finding clients “warm introductions” work best. Women are most open to referrals from their friends or other professionals — and are more willing to pass on referrals after good experiences with professionals.

She related an instance in her own life in which she and her husband refinanced their home recently. The professional helping them put her name first on the paperwork.

“In five years my name was always second,” McDowell said, even when she often bore the most responsibility in handling taxes, a house purchase and other financial decisions. “Putting my name first really mattered,” she said. And she has now referred that person to several acquaintances.

Heidi Tennant, Napfa’s senior coordinator of membership and education, included some on-the-spot polling of participants about how financial advisors might view their clients. Most of this ad hoc polling reflected general trends. Pat – did she poll webinar participants?

For example, when it came to service, a majority indicated poor service would cause a female client to change advisors, rather than poor financial performance alone.

And McDowell said general statistics bear that out. She said they show 56% of women see poor service or a lack of communication as a reason to change advisors, compared with 33% who would leave for poor financial performance.

Investment Strategies

The title of McDowell’s final segment, “Planning Her Portfolio”, was an opportunity to emphasize how fulfilling personal goals is a statistical priority for women investors.

“Learn the values that power her life,” McDowell said of female clients.

Women often have environmental and social goals and are among the most generous to charities, all of which play into investment needs.

Focus on conversations in terms of progress toward these goals, she advised.

Risk is another area that needs to be addressed — and the risk of not taking enough risk.

Women tend to be more risk-averse than men, as was made clear, and McDowell said she is no different.

“I hate thinking about losing money. But I love calculated risk,” she said.

Afraid of heights, but still an adventurous vacationer, McDowell said she does her research, takes risk into account and moves ahead when she feels she’s likely to safely experience a challenge such as ziplining on her vacation.

Financial planning requires a similar mindset.

“Educate your clients,” she advises, and they too can benefit from a degree of risk they are comfortable with to achieve their life goals.

Patricia McDaniel is a freelance writer and editor and former journalist with Gannett’s New Jersey newspapers. She can be reached at pmcd5353@gmail.com.