Persistent gaps in financial well-being between Americans identifying as White and those identifying as Black or Hispanic extend beyond inequalities in income, says a new report.

The Employee Benefit Research Institute (EBRI) on June 10 released the report, “2021 Retirement Confidence Survey: A Closer Look at Black and Hispanic Americans,” which further analyzed some of the findings in its 31st annual RCS survey. Craig Copeland, Ph.D., of EBRI, and Lisa Greenwald of Greenwald Research wrote the report.

Regardless of race or ethnicity, the authors found, confidence in having enough money to live comfortably in retirement increases with income. For example, in the upper income group, 86% of White, 84% of Black and 85% of Hispanic Americans said they were confident about their retirement prospects.

EBRI’s RCS survey consider upper income to be $75,000 or more, middle income to be $35,000 to $74,999, and low income to be below $35,000.

The report included several specific findings illustrating that overall, Black and Hispanic Americans face significantly greater difficulties planning for and dealing with retirement than do White Americans.

“Black and Hispanic Americans reported disproportionately lower financial resources, and how they feel about retirement and financial security is clearly impacted by having less resources,” the analysis noted.

For example, Black and Hispanic Americans tended to have less accumulated wealth than White Americans, even among those in the same income group. Among those with upper income, 56% of White Americans had $250,000 or more in assets (not including primary residence or defined benefit plans), compared with 39% of both Black and Hispanic Americans. In the middle-income group, 26% of White Americans had $250,000 or more in assets, compared with 8% of Hispanic Americans and 4% of Black Americans.

In the lower-income group, 58% of Black Americans and 47% of Hispanic Americans reported savings of less than $1,000, compared with 38% of White Americans. Among middle-income respondents, 32% of Black Americans had savings of less than $1,000 vs. 13% of White Americans and 18% of Hispanic Americans.

Black and Hispanic people were also more likely to see debt as a problem. “In the upper-income group, 62% of Black Americans and 58% of Hispanic Americans considered debt a problem compared with 37% of White Americans,” the report said. “Debt being considered a problem among Black and Hispanic Americans had no significant differences across gender, marital status, and whether they were U.S. born.”

Retirement

The survey found that 26% of White Americans are retired, compared with only 18% of Black and Hispanic Americans. Many in all three groups found themselves retiring earlier than expected. White retirees cited having the money available to do so most frequently as the reason, while Black and Hispanic retirees most often named health problems and disabilities for retiring early. Furthermore, 53% of Black and Hispanic retirees reported retiring earlier than planned, compared with 46% of White retirees.

The survey also uncovered attitudinal differences between the groups. Regarding reasons for delaying retirement savings, Hispanic and Black Americans were more likely than their White counterparts to agree with the statement, “It is more important to help friends and family now than to save for your own retirement.” This was true among all income groups.

Working With Financial Advisors

Black and Hispanic Americans were also far less likely to engage the services of financial advisors. Among White retirees, 41% reported working with a financial advisor, compared with 17% of Black retirees, and 27% of Hispanic retirees.

However, 15% of Black retirees and 14% of Hispanic retirees without advisors said they would consider working with one in the future. That compared with only 8% of White retirees. Similar trends were found among Americans still working.

Among the three groups, those with higher income were more likely to engage a professional financial advisor. Overall, 45% of people with $75,000 or more work with a professional advisor, including 46% of White, 41% of Black and 50% of Hispanic respondents.

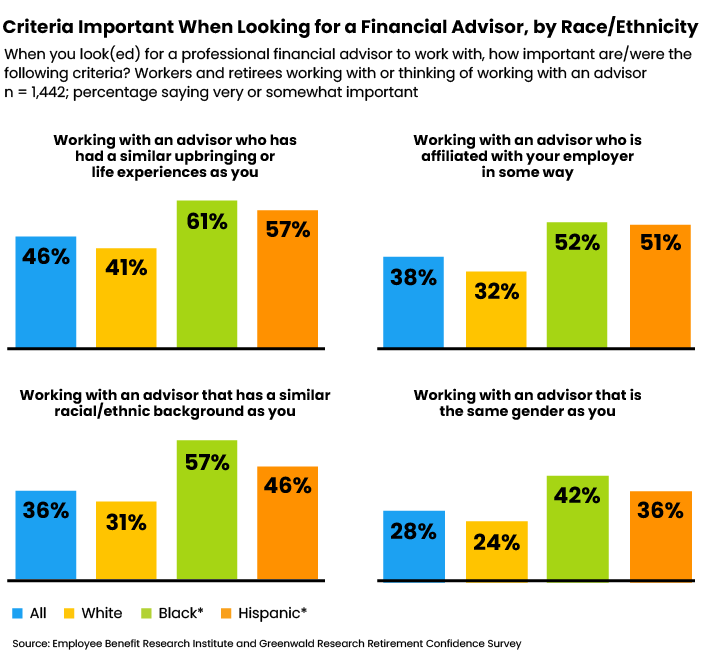

Another attitudinal difference among the three groups was the importance of cultural commonality with their financial advisor.

Black and Hispanic Americans were significantly more likely than White Americans to agree or strongly agree that it was important to work with an advisor who:

• Has had a similar upbringing or life experiences as you.

• Is affiliated with your employer in some way.

• Has a similar racial/ethnic background to you.

• Is the same gender as you.

EBRI worked on the Retirement Confidence Survey with Greenwald Research. The total survey participants numbered 3,017 Americans, including 1,507 workers and 1,510 retirees. The Retirement Confidence Survey is the longest-running survey of its kind, measuring worker and retiree confidence about retirement.

This year’s survey was sponsored by a broad array of banks, investment and insurance companies, and consumer and business groups. They include AARP, Aon, Ariel Investments, Ayco, Bank of America, BlackRock, Capital Group, Columbia Threadneedle, Empower Retirement, Fidelity Investments, FINRA Foundation, J.P. Morgan, Legal & General Investment Management America (LGIMA), Mercer, Mutual of America, Nationwide Financial, New York Life, PIMCO, Principal Financial Group, Prudential, PGIM, Retirement Clearinghouse, T. Rowe Price, Segal, U.S. Chamber of Commerce, and Wells Fargo.

EBRI worked on the Retirement Confidence Survey with Greenwald Research. The total survey participants numbered 3,017 Americans, including 1,507 workers and 1,510 retirees. The Retirement Confidence Survey is the longest-running survey of its kind, measuring worker and retiree confidence about retirement.

EBRI worked on the Retirement Confidence Survey with Greenwald Research. The total survey participants numbered 3,017 Americans, including 1,507 workers and 1,510 retirees. The Retirement Confidence Survey is the longest-running survey of its kind, measuring worker and retiree confidence about retirement.