After the Achieving a Better Life Experience Act (ABLE Act) was signed into law back in December 2014 — to create tax-free savings accounts for individuals with disabilities — families had to patiently wait a couple years for states to develop and start rolling out programs.

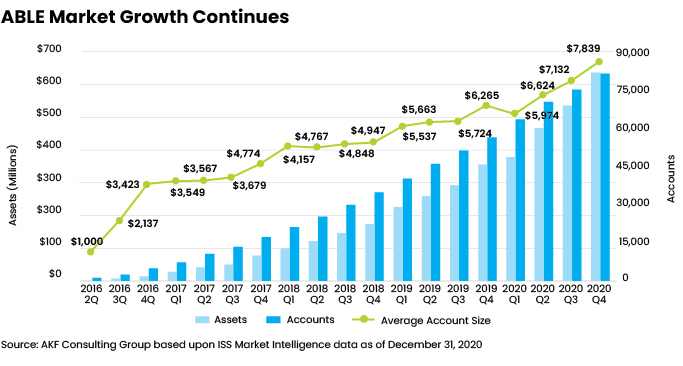

Today, 43 states and the District of Columbia offer ABLE Plans, which as of Dec. 31, had $643 million in assets under management across 82,019 accounts, according to ISS Market Intelligence and AKF Consulting, a strategic advisor to public administrators of ABLE, 529 college savings and state-run retirement programs.

As impressive as this growth has been, even during the COVID-19 pandemic, Andrea Feirstein, the founder and a managing director of AKF Consulting, which recently published an AKF Market Report on the ABLE market, tells me she is concerned that many people may be overlooking the important role that ABLE plans can play in helping provide for their children or other loved ones with special needs.

While parents in their 50s and 60s with moderate or higher income have probably already done special-needs planning for down the road, she says, “what I want people to understand, because I think they don’t right now, is that you can have a special needs trust and an ABLE account” without jeopardizing the special needs trust. “That’s the message that hasn’t gotten out as much,” she says — and financial advisors can help convey this.

The ABLE Act, which amends Section 529 of the Internal Revenue Code of 1986, makes tax-free 529A (ABLE) accounts available to save and pay for qualified disability expenses (QDEs) such as education, housing, transportation, employment training, assistive technology, health and wellness. Most plans offer debit or prepaid cards to make it easy to access ABLE funds.

Without an ABLE account, individuals with disabilities lose SSI (supplemental security income), Medicaid and other benefits when they accumulate more than $2,000 of countable resources — the limit since 1989. Countable resources include cash, investable assets and more. With an ABLE account, individuals may save up to $100,000 before SSI is suspended; their Medicaid benefits are retained even above this threshold.

The total allowable balance in an ABLE account varies by state and often exceeds $300,000. Keep in mind, though, when planning for clients, that the balance at a beneficiary’s death may be subject to “payback” to the state for Medicaid services received while the account was open.

Parents of adult children with disabilities may not be aware that ABLE accounts can be opened anytime before a beneficiary turns 65, as long as the age of onset of the qualifying disability was prior to the beneficiary’s 26th birthday. Adult beneficiaries may also open and manage their ABLE accounts if they are capable.

Feirstein also wants older adults, many of whom have children in their late 20s, 30s and 40s, to know about the proposed ABLE Age Adjustment Act, which aims to increase the age of onset for ABLE eligibility to just prior to 46. If enacted, the legislation — which has bipartisan sponsorship in the House and Senate — would increase the pool of eligible ABLE participants from 8 million to 14 million, estimates the National Disability Institute.

“Think about the number of people in their 40s or 30s who begin to experience or have some event that causes a disability in their life,” she says. “You could have early onset of dementia, you could have cancer, you could have so many different things.”

The allowable annual contribution for ABLE accounts is currently $15,000, and a third-party transfer to an ABLE account qualifies for the federal annual gift tax exclusion. Thanks to the Tax Cuts and Jobs Act of 2017, ABLE account beneficiaries who are employed are generally permitted to contribute up to an additional $12,760 a year, although that provision — and the ability to rollover a 529 college savings account into a 529A ABLE account — are scheduled to sunset in 2026.

Many ABLE plans are open to anyone nationwide, says Feirstein, but she suggests first checking out the options in one’s own state because the benefits and costs can vary. For example, certain states offer a particular tax benefit or other benefits for participating in just that state’s plan. Additionally, there can be an added fee if the individual chooses a plan not offered by the state in which the account owner/beneficiary resides.

This would be the case for account owners outside of an Ohio Partner State choosing the Ohio Stable plan. In this case, the management fee for an account is higher than what it would be if Ohio had a partner relationship with that state, she says.

According to the AKF Market Report, 16 states currently offer state tax benefits for ABLE contributions, 20 states and the District of Columbia don’t offer tax benefits, and the seven other states with ABLE plans don’t have state income tax. Feirstein would like to see more states offer tax benefits for ABLE plans (as 35 do for 529 college savings plans) because it would increase the appeal of contributing, she says.

ABLE plans are also beginning to do more outreach with national and local disability organizations and advocacy groups, says Feirstein. The National Disability Institute (NDI) has established the ABLE National Resource Center, an online resource.

Presently, all ABLE plans except one are direct-sold to participants. The nation’s one advisor-sold plan, AbleAmerica, is sponsored byVirginia529 and distributed by American Funds, a family of mutual funds from Capital Group. It’s open to eligible individuals in all 50 states. The average size of a direct-sold ABLE account is $7,779, compared with $12,789 for an advisor-sold account as of Dec. 31, according to ISS Market Intelligence.

“Advisors are critical to financial planning for people with disabilities,” says Feirstein, and can incorporate ABLE accounts into broad financial and estate plans. It’s also important to speak with a special-needs attorney.

Jerilyn Klein is editorial director of Rethinking65.

While parents in their 50s and 60s with moderate or higher income have probably already done special-needs planning for down the road, she says, “what I want people to understand, because I think they don’t right now, is that you can have a special needs trust and an ABLE account” without jeopardizing the special needs trust. “That’s the message that hasn’t gotten out as much,” she says — and financial advisors can help convey this.

While parents in their 50s and 60s with moderate or higher income have probably already done special-needs planning for down the road, she says, “what I want people to understand, because I think they don’t right now, is that you can have a special needs trust and an ABLE account” without jeopardizing the special needs trust. “That’s the message that hasn’t gotten out as much,” she says — and financial advisors can help convey this.