Key takeaways

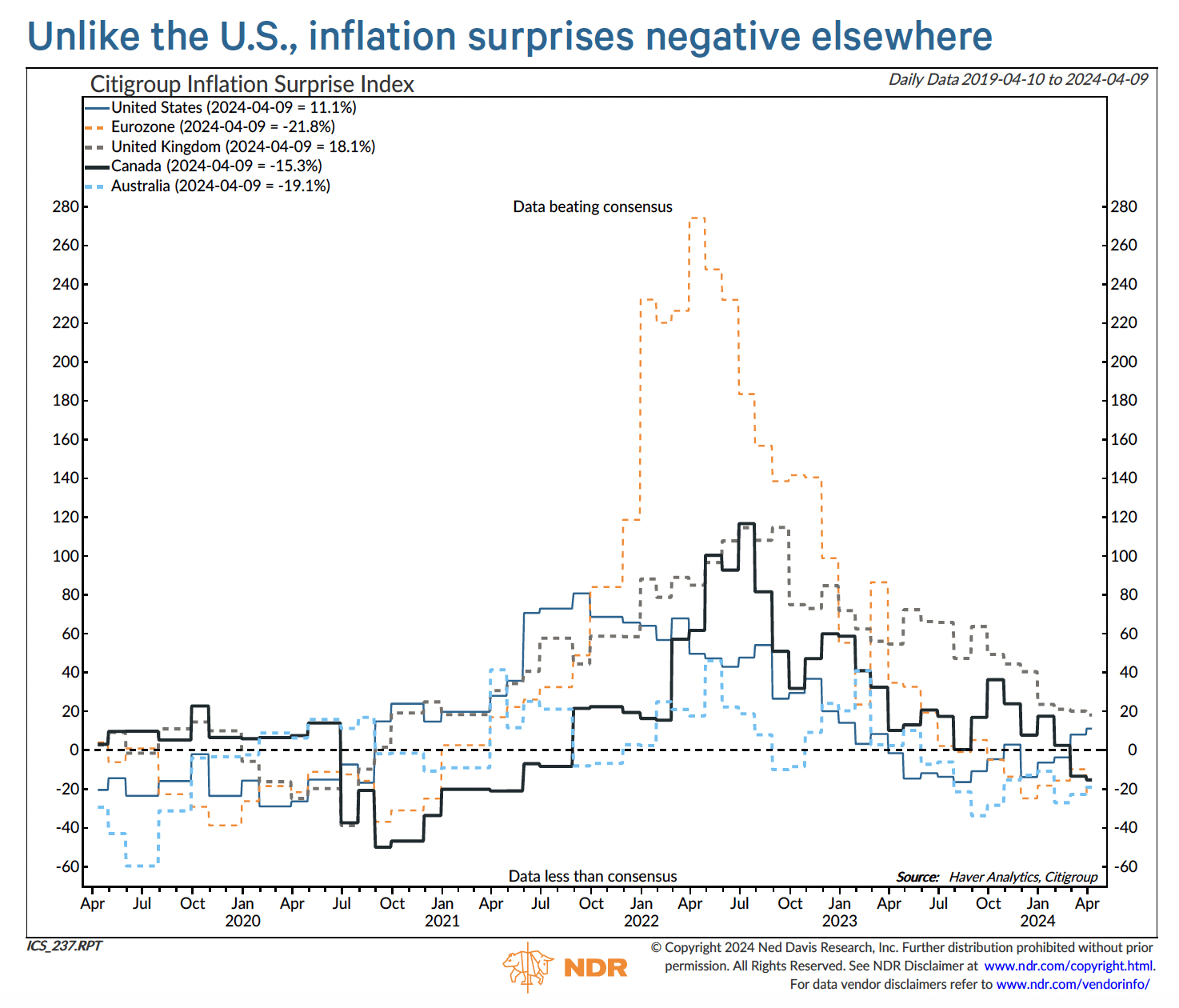

- While U.S. inflation is accelerating, elsewhere in the world it’s surprising to the downside, suggesting other major central banks could cut rates first.

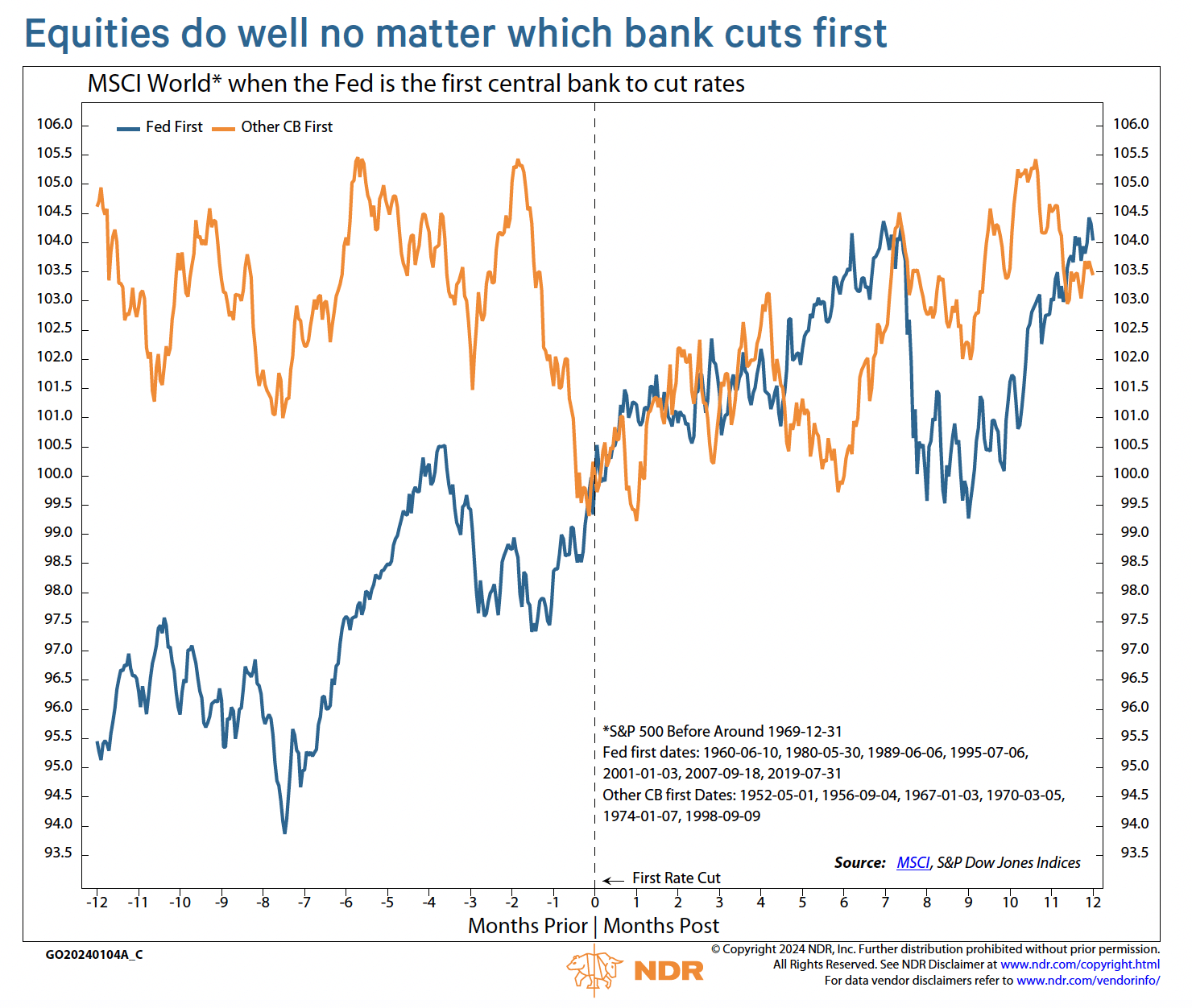

- The good news is that equities still rise and the dollar tends to weaken in these instances, as long as the Fed eventually follows.

- A more worrisome development would be if the Fed increases rates while other parts of the world are easing policy.

Inflation paths have changed

At the beginning of the year, the Fed appeared to be on a clear path to easing policy. Inflation data was coming in less than anticipated, with markets pricing in around 150 bp of rate cuts this year.

But a few ugly inflation reports since then, including this latest one for March, coupled with a stronger-than-expected labor market, has reduced some clarity on the Fed’s path.

On the other hand, in many other parts of the developed world, such as the Eurozone, Canada, and Australia, inflation has been surprising to the downside. Upside surprises remain positive in the U.K., but much less so compared to recent months.

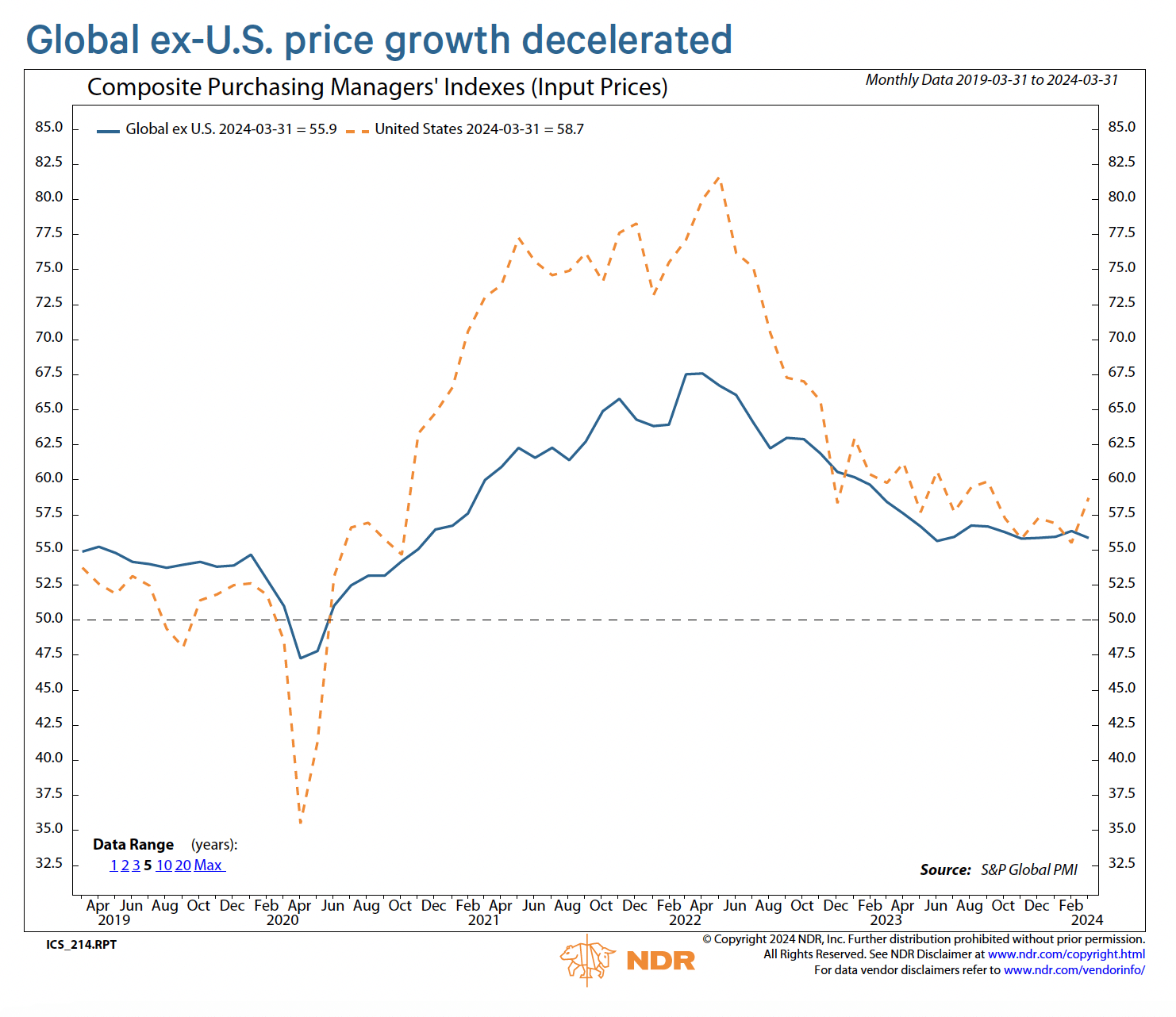

This disparity in the inflation trend was also evident in the latest global PMIs, which saw global input and output price growth pick up markedly in the U.S., but slow on aggregate in the rest of the world.

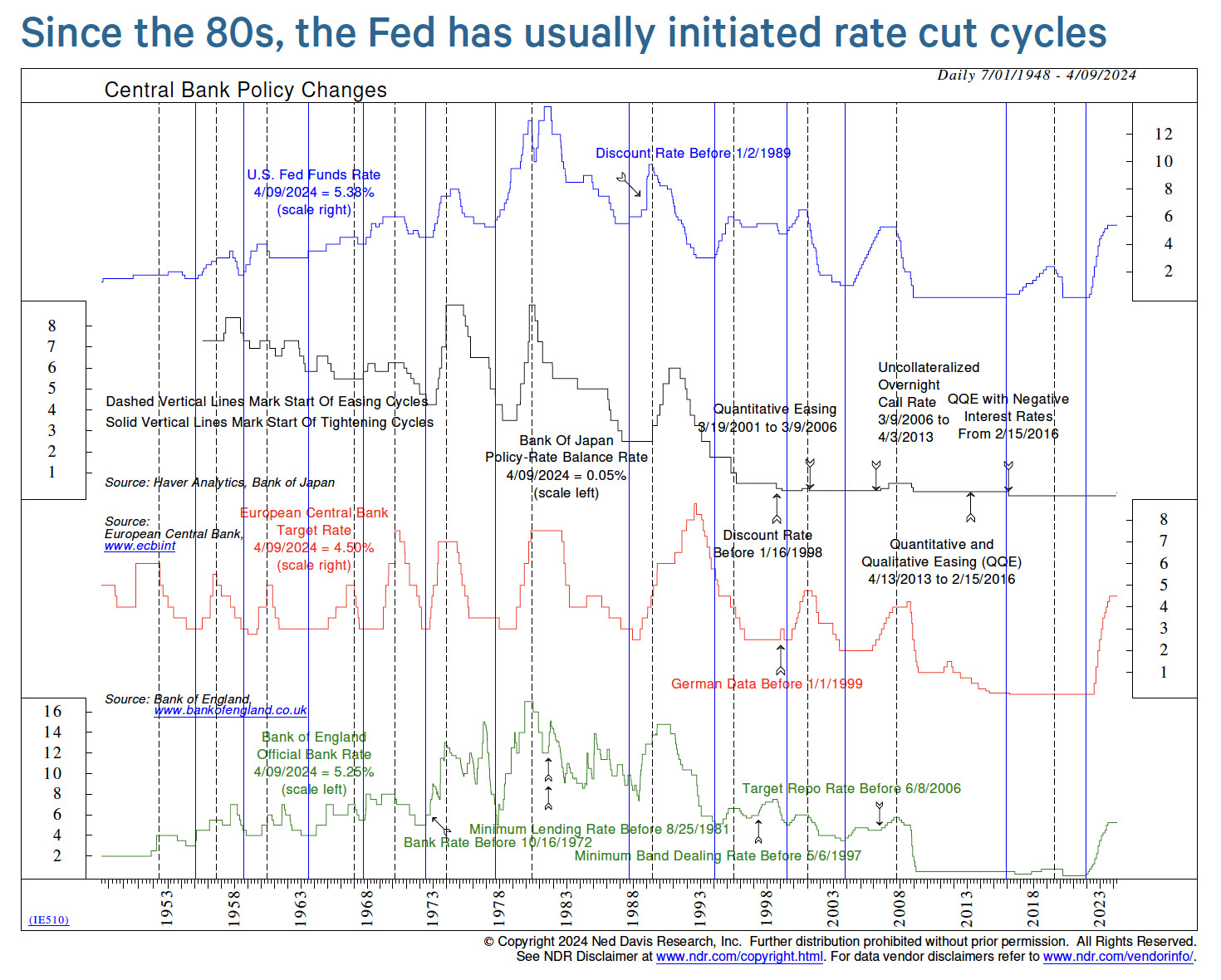

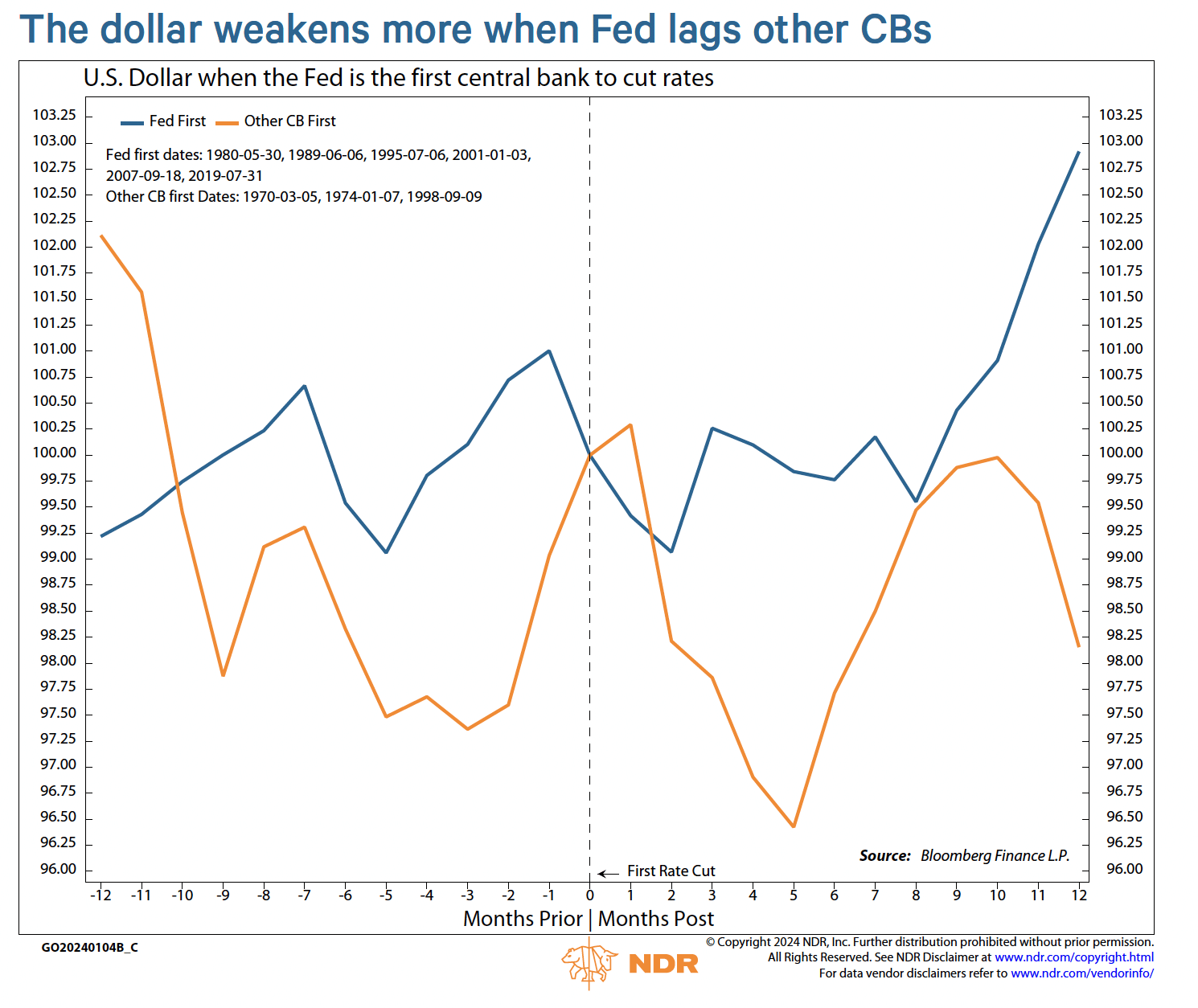

Not the usual leader

While we still expect the Fed to ease policy this year, the other major developed market central banks may do so before the Fed. In recent history, this has been highly unusual. Since the early 1980s, the Fed has led all but one (in 1998) of the easing cycles among major developed market central banks. The good news is that equities still rise and the dollar tends to weaken in these instances, as long as the Fed eventually follows.

A more worrisome development would be if the Fed increases rates while other parts

of the world are easing policy. This is even a more unusual circumstance. However, we

did see this happen in 2015. In that case, we saw the dollar strengthen and equity markets down a year later.

Inflation surprises have turned positive in the U.S., according to the Citigroup Inflation Surprise Index. Meanwhile, inflation surprises are negative or have become less positive among most other major developed economies.

The March global PMI report saw both the input and output prices indexes accelerate in March. However, the gain was led by the U.S., as shown in the chart at left. Excluding the U.S., global inflation growth eased.

The Fed has initiated almost all rate-cut cycles (except for 1998) since the early 1980s.

Prior to that, the lead in rate hike cycles was more varied, occasionally led by the Bank of

England or the Bundesbank.

As shown in the chart below, equities have on average been up by around the same

amount a year after a first rate cut whether the Fed or another central bank initiated the

cycle.

The dollar tends to fall when the Fed embarks on a rate-cut cycle whether the Fed

goes first or another central bank. However, the decline has tended to be even larger a

year later when the Fed has lagged other central banks.

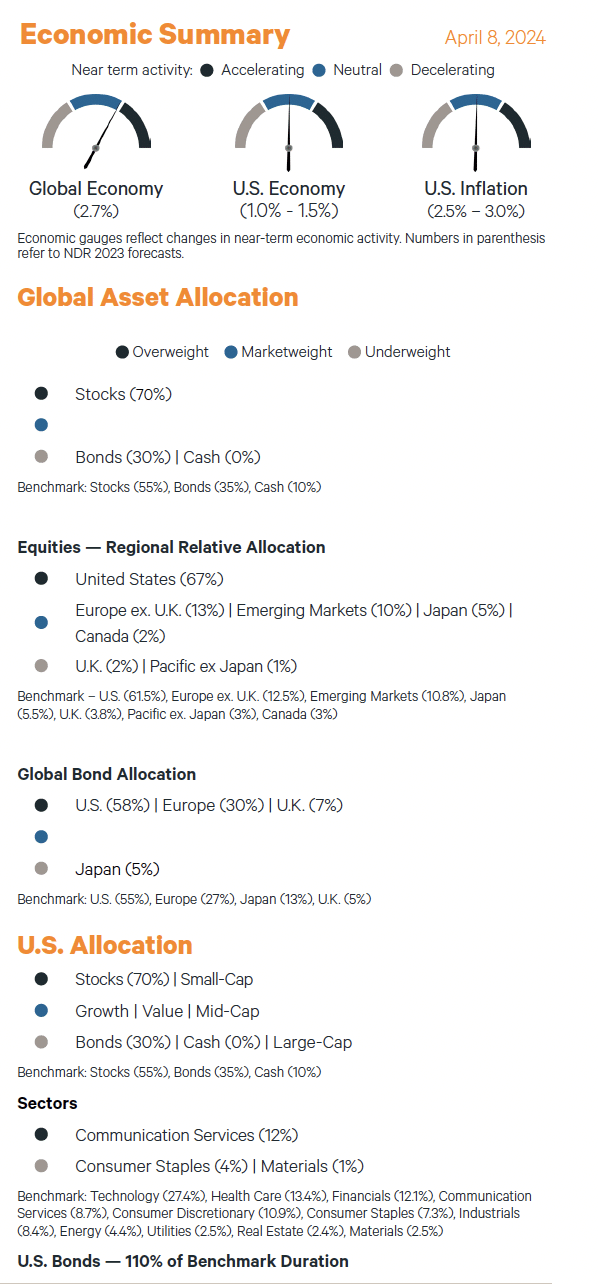

For global asset allocation, NDR recommends an overweight allocation to stocks and underweight allocations to bonds and cash. Our recommendations are in-line with our Global Balanced Account Model.

Equity Allocation

U.S.

Our U.S. asset allocation recommendation is 70% stocks (15% overweight), 30% bonds (5% underweight), and 0% cash (10% underweight). On an absolute basis, we are overweight the S&P 500. The technical deterioration during the July – October correction has been replaced with some of the strongest breadth readings this cycle. We favor small-caps over large-caps and are neutral on Growth versus Value.

INTERNATIONAL

We are overweight the U.S., underweight the U.K. and Pacific ex. Japan, and marketweight on all other regions.

Macro

ECONOMY

The global economy has shown notable resilience, with recession chances waning. Risks include monetary and fiscal policy uncertainty, sticky inflation, and easing Chinese growth.

FIXED INCOME

We raised our exposure to 110% of benchmark duration, and recommend curve steepeners. We are overweight MBS and underweight CMBS and ABS. We are marketweight everything else.

GOLD

We are currently bullish.

DOLLAR

We are currently bearish.

Alejandra Grindal is chief economist and Patrick Ayers is senior analyst for Ned Davis Research Group.

Founded in 1980, Ned Davis Research Group is a leading independent research firm with clients around the globe. With a range of products and services utilizing a 360° methodology, we deliver award-winning solutions to the world’s leading investment management companies. Our clients include professionals from global investment firms, banks, insurance companies, mutual funds, hedge funds, pension and endowment funds, and registered investment advisors.

Important Information and Disclaimers

NDR (Ned Davis Research) uses the weight of the evidence and a 360-degree approach to build up to market insights. When we say “evidence,” we mean processing millions of data series to fuel a historical perspective, build proprietary indicators and models, and calm investors in a world full of bull/bear news hype and hysteria. We believe that no client is too big or too small to benefit from NDR’s insights.

The data and analysis contained in NDR’s publications are provided “as is” and without warranty of any kind, either expressed or implied. The information is based on data believed to be reliable, but it is not guaranteed. NDR DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE.

NDR’s reports reflect opinions of our analysts as of the date of each report, and they will not necessarily be updated as views or information change. All opinions expressed therein are subject to change without notice, and you should always obtain current information and perform due diligence before trading. NDR or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed in NDR’s publications and may purchase or sell such securities without notice.

NDR uses and has historically used various methods to evaluate investments which may, at times, produce contradictory recommendations with respect to the same securities. When evaluating the results of prior NDR recommendations or NDR performance rankings, one should also consider that NDR may modify the methods it uses to evaluate investment opportunities from time to time, that model results do not impute or show the compounded adverse effect of transaction costs or management fees or reflect actual investment results, that other less successful recommendations made by NDR are not included with these model performance reports, that some model results do not reflect actual historical recommendations, and that investment models are necessarily constructed with the benefit of hindsight. Unless specifically noted on a chart, report, or other device, all performance measures are purely hypothetical, and are the results of back-tested methodologies using data and analysis over time periods that pre-dated the creation of the analysis and do not reflect tax consequences, execution, commissions, and other trading costs. For these and for many other reasons, the performance of NDR’s past recommendations and model results are not a guarantee of future results.

Using any graph, chart, formula, model, or other device to assist in deciding which securities to trade or when to trade them presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves continuously or on any particular occasion. In addition, market participants using such devices can impact the market in a way that changes the effectiveness of such devices. NDR believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision and suggests that all market participants consider differing viewpoints and use a weight of the evidence approach that fits their investment needs. Any particular piece of content or commentary may or may not be representative of the NDR House View, and may not align with any of the other content or commentary that is provided in the service. Performance measures on any chart or report are not intended to represent the performance of an investment account or portfolio, as some formulas or models may have superior or inferior results over differing time periods based upon macro-economic or investment market regimes. NDR generally provides a full history of a formula or model’s hypothetical performance, which often reflects an “all in” investment of the represented market or security during “buy”, “bullish”, or similar recommendations. This approach is not indicative of the intended usage of the recommendation in a client’s portfolio, and for this reason NDR does not typically display returns as would be commonly stated when reporting portfolio performance. Clients seeking the usage of any NDR content in a simulated portfolio back-test should contact their account representative to discuss testing that NDR can perform using the client’s specific risk tolerances, fees, and other constraints.

NDR’s reports are not intended to be the primary basis for investment decisions and are not designed to meet the particular investment needs of any investor. The reports do not address the suitability of any particular investment for any particular investor. The reports do not address the tax consequences of securities, investments, or strategies, and investors should consult their tax advisors before making investment decisions. Investors should seek professional advice before making investment decisions. The reports are not an offer or the solicitation of an offer to buy or to sell a security. Further distribution prohibited without prior permission. Full terms of service, including copyrights, terms of use, and disclaimers are available at https://www.ndr.com/web/ndr/terms-of-service. Copyright 2024 (c) Ned Davis Research, Inc. All rights reserved.