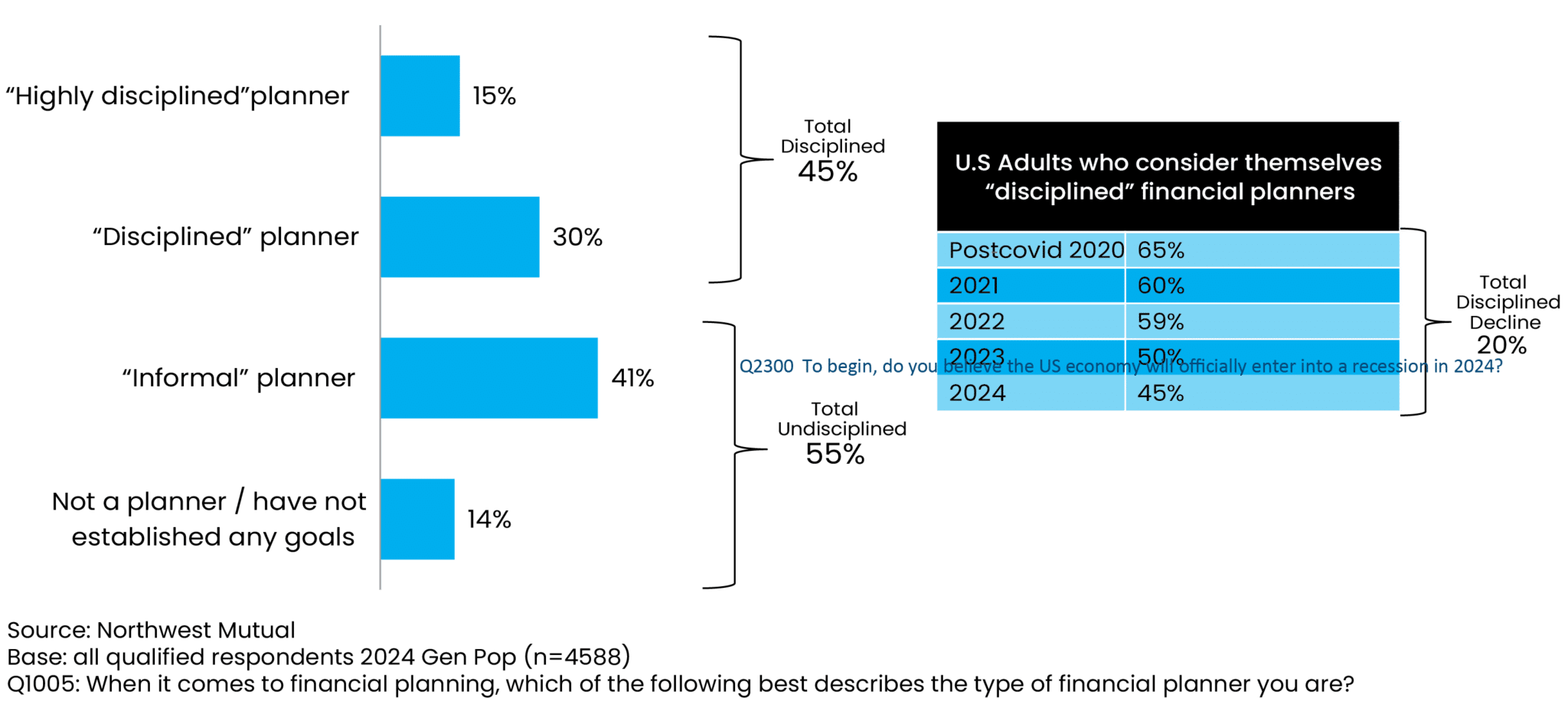

Despite an enhanced view of the country’s economy and record-high feelings of financial insecurity, the number of Americans whom consider themselves “disciplined” financial planners keeps declining from the pandemic era, a recent survey by Northwestern Mutual shows.

The Milwaukee company’s 2024 assessment of 4,500 adults shows only 45% perceive themselves as “disciplined,” down 20 points from the 65% who gave themselves this label when the pandemic emerged in 2020.

This year’s 45% figure is five points less than the 50% who chose this category in 2023 and down 19 points from 59% in 2022.

“People got their financial house in order during Covid,” said Stephen Schwartz, a wealth management advisor at Northwestern Mutual, during a March 7 presentation held in New York City to unveil the firm’s annual survey results. “We wish they had kept that up but they haven’t.”

The company’s 2024 Planning & Progress Study, its sixteenth annual survey, was carried out online by the Harris Poll in January of this year among 4,588 U.S. adults 18 years of age or older. To bring the data in line with the actual proportions in the population, it was weighted where necessary by age, gender, race/ethnicity, region, education, martial status, household size, household income and propensity to be online.

Just over half, or 54% of the responding U.S. adults expect the country to enter a recession this year, a substantial drop from the two-thirds, or 67%, that anticipated a recession in 2023. The double-digit increases in optimism were consistent across four generations: Gen Z, Millennials, Gen X and Boomers+.

Feelings of Financial Anxiety

Feelings of Financial Anxiety

Yet at the same time, more people, 33% or one-third of the survey participants, feel insecure financially, up from 27% in 2023.

“This is the highest level of financial insecurity recorded in the 16 years of the survey,” said Christian Mitchell, executive vice president and chief customer officer at Northwestern Mutual.

Inflation is a major element behind the pervading sense of financial anxiety, along with other psychological reasons such as the ongoing dysfunction in the U.S. Congress in Washington D.C. and wars in the Ukraine and Mideast.

“This is coloring how they are feeling about their finances,” said Mitchell. In response to a question, he added that focus groups show people are also anxious about the changing climate’s impact on their financial security.

Regarding upcoming elections, the two executives see clients more concerned with their individual financial circumstances rather than future election outcomes.

“I’m getting divorced…what do I do? That is a question that is more likely now than “What about the upcoming elections,’” said Schwartz. Those saving over the next two to four decades generally show less concern with political races’ outcomes on their financial futures, he added.

Schwartz said the biggest pain point clients are experiencing financially right now center on housing. “It’s the higher interest rates and the lack of inventory. People feel they are married to their mortgages,” he said, adding there is a generation of consumers who have never experienced high inflation or high interest rates.

When asked which concerns could impact their finances most significantly this year, 57% of respondents put inflation at the top of their list. Government dysfunction ranked second on the list of concerns at 34% and the U.S. president election ranked third at 33%. Longer-term worries were a potential recession (24%), market volatility (15%) and geopolitical conflicts (14%).

Financial Strategy: Playing Defense or Offense

To counter these conditions and feelings, more people, or 42% of the respondents, are turning 2024 into a year of “playing defense” with their savings and investments by managing risk to protect their assets. On the other hand, 29% of respondents feel 2024 is a year to “play offense” by capitalizing on opportunities to grow their assets. Twenty-nine percent of respondents were unsure.

The game plan for the defensive players is mostly focused on cutting costs (56%) and building savings (51%). Younger generations score higher on adding a side hustle, with 46% of Gen Z and 43% of millennials opting for this possibility. About one in six millennials, or 16%, said they would seek a financial advisor this year and 15% would buy life insurance or increase their life insurance coverage.

Among high net-worth individuals, those with more than $1 million in investable assets, about 40% are moving into safe, high-yielding instruments like money market funds.

On the other hand, for those playing offense, the game plan is expanding their investments in the stock market (42%). Half (50%) of high-net work individuals are going with equity investments as are 52% of Gen Z respondents.

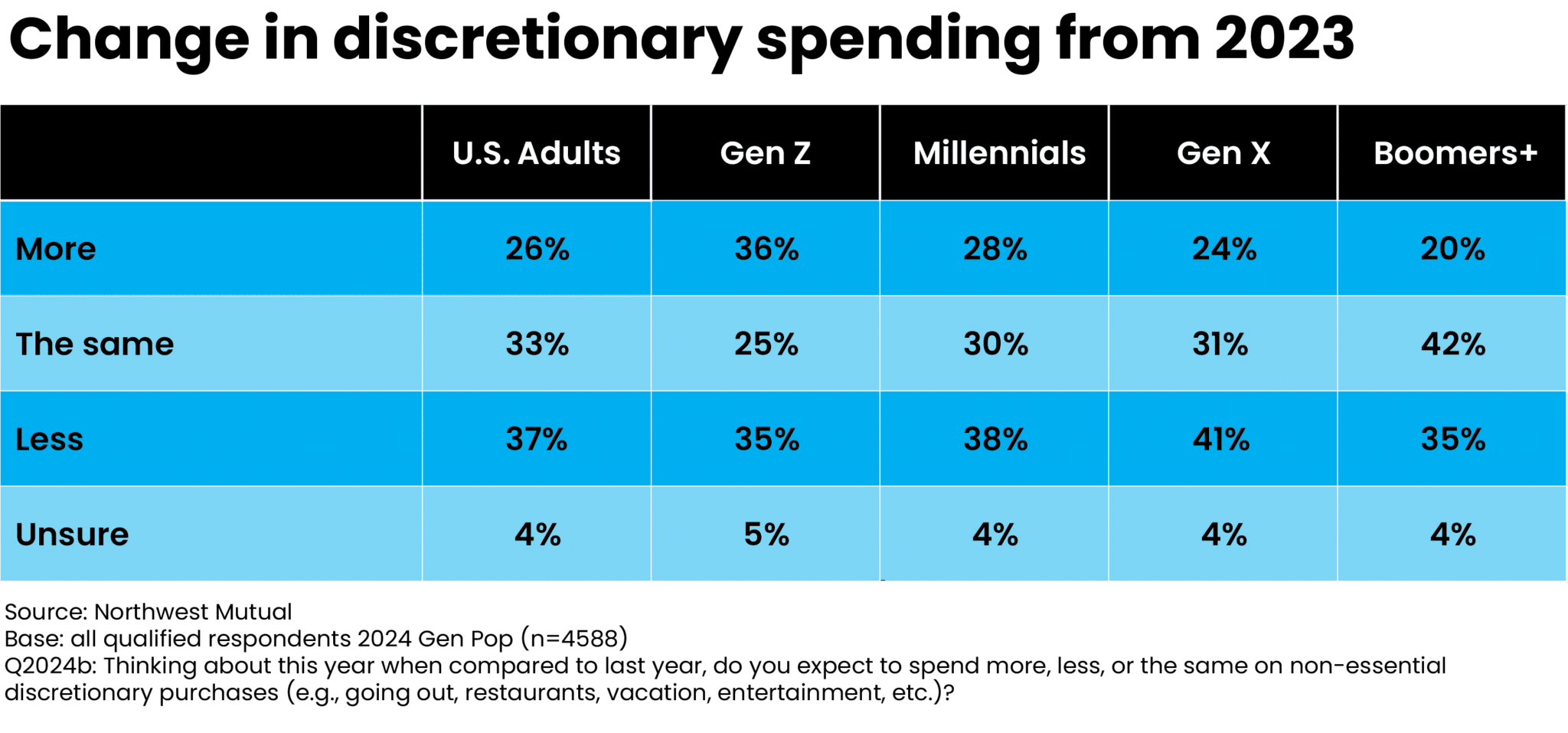

Discretionary Spending Remains Strong

Yet despite this heightened sense of financial insecurity, many Americans don’t expect to pull back significantly on discretionary spending, such as restaurants, vacations and entertainment, this year.

The study indicates that 59% of adults say they will spend the same, or more, on these purchases in 2024, compared with 2023. Just under four in 10, or 37% of the respondents, said they will spend less. Gen Z respondents are the most likely to increase non-essential spending while Gen X are the most likely generation to be tightening their belts.

Mitchell noted that since the pandemic era Americans less than 40 years of age have seen their wealth rise at a faster rate than other age groups, such as through stimulus checks, pauses in student loan payments and automatic enrollment in retirement programs. So they feel comfortable spending and investing, he added.

Mitchell noted that since the pandemic era Americans less than 40 years of age have seen their wealth rise at a faster rate than other age groups, such as through stimulus checks, pauses in student loan payments and automatic enrollment in retirement programs. So they feel comfortable spending and investing, he added.

In response to a question, Schwartz said the issue of wealth transfer, as the boomer generation get ready to transfer their wealth to younger generation has not yet emerged in a significant way. Added Mitchell, “I think we are just at the tip of the wealth transfers from boomers.”

The Northwestern executives questioned whether clients — and financial advisors — are aware of the major tax law changes that will impact the transfer of wealth at the end of 2025.

The 2017 Tax Cuts and Jobs Act (TCJA) nearly doubled the lifetime estate and gift tax exemption from its previous levels. For 2024, the exemption stands at $13.61 million per person and $27.22 million for a married couple. Starting Jan. 1, 2026, if the act sunsets as planned, the current lifetime estate and gift tax exemption will be cut in half, and adjusted for inflation. That means approximately $7.5 million per individual and $14.5 million for a married couple, depending on inflation over the next few years.

“Estate attorneys have a lot of work to do,” said Schwartz.

Paula L. Green is a New York City-based freelance journalist with more than three decades of reporting and editing experience that spans coverage of international business and finance issues to murders and politics at the Jersey Shore to presidential press conferences in Argentina and Mexico. She can be contacted by plgreen12004@gmail.com.