Many clients tell their advisors they’re concerned about transferring their wealth to the next generation because their children or grandchildren are financially irresponsible. While good planning is necessary, it’s also very important to start teaching financial literacy at a young age. Rosanna Guardavaccaro, a financial planner with Shelton, Conn.-headquartered Barnum Financial Group and the author of the “Peter Saves” children’s book series on money, recently shared some thoughts with Rethinking65.

Jerilyn Klein: You’ve been a financial advisor for 20 years. How did you originally get interested in the industry?

Rosanna Guardavaccaro: I was attending Brooklyn College and an economics professor nominated me for an internship. I would be the first intern at Brooklyn College to begin at a financial planning firm. At that time, I was still committed to pursuing a career in accounting. A mentor told me to write a few things I enjoyed doing. Speaking, teaching and numbers. From that point on, I knew I had to switch paths and take the proper examinations to becoming a financial planner, and the rest is history.

Klein: What types of clients and specialties have you gravitated towards during your years in practice?

Guardavaccaro: I have gravitated toward clients who help their families and have solid relationships with friends. My clients love what they do and have a passion for it.

Klein: You recently joined Barnum Financial Group as a financial planner. What attracted you to Barnum and what type of work are you focusing on?

Guardavaccaro: Educating clients has always been number one for me. Financial literacy amongst adults is something that attracted me to Barnum. This is what they’re known for. Working in the field of finance, creating a holistic practice, where there is a need for many resources and support. Barnum had the resources my clients and I needed to continue in this space.

Klein: You’ve said that “education plus advocacy creates empowerment” is the mantra for your financial strategies practice, and that it’s also what drives your commitment to financial literacy for children and adults. Tell me about this commitment and what sparked it.

“Education, advocacy and empowerment are words I think about every day. When you are educating a client, you are helping and leading them to a decision that will impact their lives.”

Guardavaccaro: Education, advocacy and empowerment are words I think about every day. When you are educating a client, you are helping and leading them to a decision that will impact their lives. You are also giving them the power to make different decisions. Saving and investing allows them to make choices they might not have made if they didn’t save. Being educated also helps them generate the confidence to put a financial plan in place.

Klein: Among your clients, what are the biggest gaps you see in financial literacy and how do you help them improve this? How are the literacy gaps different for people nearing retirement vs. younger people?

Guardavaccaro: I realized people are not taught financial concepts in school. They learn other subjects and search for a career and passion to create income. But virtually no one is taught what to do with the income once earned. I think individuals near retirement are more educated because they realize the importance of it through their life experiences. As they approach their wealth distribution phase, the need to save and invest more increases because there is less time. I also see them encouraging their children to start early because they themselves would have wanted to do that knowing what they know now. For younger people, it is important to spend a bit more time on the education piece because it is harder for them to think ahead for the rest of their life. Discussing financial goals short, mid- and long-term is a conversation that is a must-have.

Klein: You’ve written three books in your “Peter Saves” series, which focuses on financial concepts for children. What inspired you to create these books and what do you hope they will achieve?

Guardavaccaro: My son Vito grew up listening to the financial topics I was teaching my clients. He came to me one day and said, “Mommy, I think I know what life insurance is; it’s when someone passes and goes to heaven and the money goes to their family.” In that moment, my two worlds came together. I knew I wanted to be part of an educational movement for financial literacy. I started the first book and as my son grew, so did the series. Vito helps me and gives me a lot of material to write about. It has become an amazing journey we take together.

Klein: When should clients begin teaching their children and grandchildren about money? What concepts can preschoolers understand? What about elementary school students? Preteens? Teens?

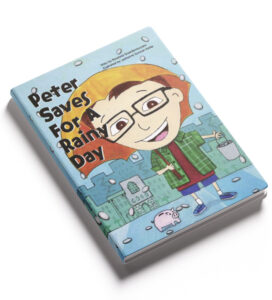

Guardavaccaro: The earlier the better. Even young children can understand financial concepts For example, the first book in the series, “Peter Saves for a Rainy Day,“ was created with pictures, colors and a story that give young children the ability to follow along. The pictures were all done by hand with acrylic paint.

Preschoolers can understand what it means to save for a rainy day. “When something new happens that we may not have expected — like a sudden rainstorm or anything we didn’t predict — it is nice to have money sitting safely in the bank for us. When the unexpected happens, such as something breaking or needing to be fixed, then families need money to pay for it.”

Elementary school students can understand budgeting. When someone earns money, where does it go? The first book illustrates a budget diagram showing the major expenses. Elementary students also can understand the difference between a need and a want. A need is something we cannot live without, like shelter, water and food. A want is something we desire — a skateboard, video game or vacation. You can do a mini-budgeting exercise where needs are on one side and wants on another. In my second book, I also introduce a savings and spending concept, by illustrating a blue and red piggy bank. The blue piggy bank is for savings (rainy day fund) and the red for spending (needs and wants). At that age, children can even grasp where the savings can be placed in different vehicles. Mainly broad definitions to plant the seed.

Elementary school students can understand budgeting. When someone earns money, where does it go? The first book illustrates a budget diagram showing the major expenses. Elementary students also can understand the difference between a need and a want. A need is something we cannot live without, like shelter, water and food. A want is something we desire — a skateboard, video game or vacation. You can do a mini-budgeting exercise where needs are on one side and wants on another. In my second book, I also introduce a savings and spending concept, by illustrating a blue and red piggy bank. The blue piggy bank is for savings (rainy day fund) and the red for spending (needs and wants). At that age, children can even grasp where the savings can be placed in different vehicles. Mainly broad definitions to plant the seed.

Pre-teens can dig a bit more into the details of spending and savings by giving examples of how to earn, such as an allowance or a job. We do a cash flow/budgeting exercise in greater detail where the children will recognize needs and wants as a review along with some grown-up expenses. The charity concept can be introduced to them as well.

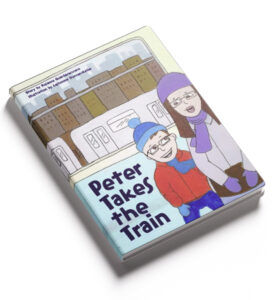

In my third book, “Peter Moves to the Big City,” I introduce a third piggy bank, which is pink. I think children should be taught to give back at an early age, including families in need. The book looks at financial goals and what that could mean for them. We write about saving money being a journey and that it takes time to get to your goal. For teens, a discussion around credit card debt highlights the difference between credit and debit cards. Teens can start to understand the different vehicles one can save in to achieve their goals. They also can start to understand financial balance — checkbooks and how to balance them, including the new newer ways to pay expenses and deposit checks.

Even though all this may sound overwhelming, children are like adults — they are just smaller. They absorb a lot. And don’t forget, in math class some of these preteens are learning algebra and some teens are learning precalculus.

Klein: What kind of activities can parents and grandparents engage in with children of different ages to teach them about money and to bond with them? Should allowances be part of the picture, and what types of accounts should children have to learn how to manage their own money?

Guardavaccaro: I think budgeting exercises are important. They help children and young adults visualize what an expense really means and if it’s a need and a want. One exercise could include drawing a diagram about credit card debt and the difference with debit cards. Using color when describing different financial concepts and ways to save will help children and teens retain the information. And, explaining that saving and investing is a journey and doesn’t happen right away but with time. An important day is physically going to the bank with the children and having them deposit their allowance in a custodian account. Another nice event is allowing children to do mobile deposits when they receive gifts for birthdays or holidays.

Klein: You donate the profits from you books to charitable organizations that help children. Can you tell me about these organizations and why they’re important to you?

Guardavaccaro: I thought it was important to give back to the children. When Vito was little, his beautiful little cousin passed away from a brain tumor. It was a very sad thing. We witnessed the family go through such heartache. We decided to donate the proceeds to the Olivia Boccuzzi Foundation to help scientists who are actively researching cures for pediatric brain tumors.

Rosanna Guardavaccaro is a financial planner at Barnum Financial Group and can be reached at 917-559-6530 or at RGuardavaccaro@barnumfg.com. Her firm offers securities and investment advisory services through qualified registered representatives of MML Investors Services, LLC.