With its Grand Strand of 60 miles of beaches, 100 golf courses, professional theater and arts centers, four shopping/residential complexes, restaurants of all stripes, an airport four miles from downtown, balmy temperatures and a competitive cost of living, Myrtle Beach, S.C. stacks up as a desirable choice for an active retirement.

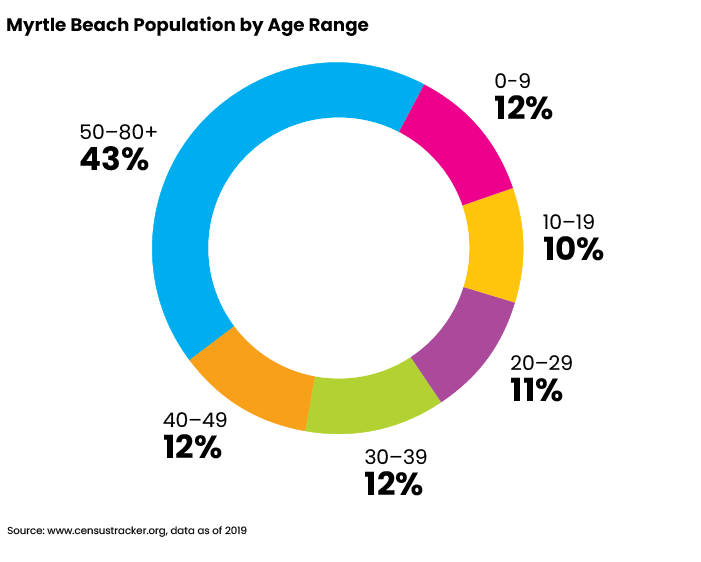

In its 2020-21 survey of 150 “best places” nationwide, U.S. News & World Report ranked Myrtle Beach No. 11 in best places to retire, and No. 1 in fastest growing places. About 24% of its permanent residents are aged 65 and older and 28.5% are aged 45 to 64. Myrtle Beach, incorporated as a town in 1938, has about 36,000 year-round residents; it draws about 15 million visitors annually. Its population has grown about 35% since the 2010 U.S. Census.

“It is growing and there is building going on every day, on the beach and inland, but it’s still a great place to be. You can get away from civilization pretty quick. In less than 30 minutes you can be in a beautiful spot on the Waccamaw River, enjoying nature,’’ says Joe Taylor, founder-owner of the independent advisory firm Oak Street Advisors in Myrtle Beach. His son Bryan Taylor, CFP, joined the firm in 2016 and he now operates its Mount Pleasant office.

“That’s how it works here: folks come here for a vacation and when the time comes, they remember how much they liked Myrtle Beach and they come back here to retire,’’ says Joe, who’s been local his whole life. He adds that Myrtle Beach is affordable for those with smaller nest eggs.

“How much you need to retire totally depends on your lifestyle,” he says. “We have clients with $250,000 portfolios; their home is paid for, they get Social Security and they can live a wonderful life.”

According to the ACCRA Cost of Living Index, housing costs in Myrtle Beach are about 55% cheaper than in central New Jersey and 22% less than in Harrisburg, Penn. Transplants from Akron, Ohio, can also figure on spending about 8% less on housing.

Housing options in and around Myrtle Beach are extensive. “You can purchase oceanfront condos for as little as $100,000, but those are really converted efficiency hotel units with less than 400- to 800-square feet of living space,” says Taylor. “Two-bedroom condos that a couple could actually live in will cost around $250,000 to $500,000.” A two-bedroom, two-bathroom apartment rental in metro Myrtle Beach is about $913 monthly, excluding utilities.

Most retirees to the Myrtle Beach area are spending $400,000 to $600,000 for housing, often in golf communities, says Taylor. Del Webb, a leading builder of active adult communities (for age 55 and up), has a development on the waterway with homes ranging from $300,000 to $700,000, he notes. Single-family homes in established inland neighborhoods are priced at a median $215,000.

Because most retirees sell a home before they move to the Myrtle Beach area, their mortgages are small compared to the price of the house they purchase, says Taylor, “and with interest rates at historic lows, their monthly expenses including housing costs are not exorbitant.”

Then again, an oceanfront home in the Myrtle Beach area will cost $1 million to $5 million, he says. “If all you have is portfolio income to support all of your lifestyle spending you would need $5 to $10 million in assets to support living in one of those,” says Taylor. He often works with retires to use portfolio assets to build an income bridge and delay claiming social security. “For most, delaying social security until age 70 and reaping the delayed retirement credits of about 8% per year makes financial sense,” he says.

Meanwhile, property taxes in Myrtle Beach “are really, really cheap compared to where our clients come from, “says Taylor. “We’re talking about $1,200 to $1,500 for a 2,500 square foot house.’’ Buyers who are 65 and older receive a Homestead Exemption of taxes on the first $50,000 in fair market value on their primary residence.

Of course, housing on or near the water will increase the cost of homeowners insurance because of possible flooding and storm damage — and South Carolina is one of the more expensive states for purchasing homeowners insurance. But health care and utility costs are lower in Myrtle Beach than in the Northeast and Midwest. Three hospital systems serve the Myrtle Beach area and a fourth is nearby.

Plenty of Activities

Residents 60 and older looking to stay engaged in learning may take tuition-free courses at Coastal Carolina University in Conway, a 12 mile drive from Myrtle Beach. Few of Taylor’s clients choose to work during retirement, but he knows retirees who work as golf-course rangers “just to get the free golf benefits and get themselves out of the house,” he says. “Being a seasonal service-oriented economy, there are opportunities for part-time work in the hospitality industry, but the pay and benefits are generally poor.”

Myrtle Beach offers plenty of things to do and its weather encourages outdoor activities: Temperatures range from the high 50s in January and February to the high 80s in July and August. Popular family attractions include the Family Kingdom Amusement Park, with about 40 rides; all-day passes are $25 and single rides are $1.15. Ninety-minute boat excursions on the Waccamaw River, narrated by a guide, cost $30 for adults, and $17 for children.

The Myrtle Beach area extends from Murrels Inlet in the south to Caswell Beach in the north. Murrels Inlet has a half-mile-long boardwalk overlooking the pristine marshes, and numerous seafood restaurants. If you prefer to cook your own, there’s Murrels Inlet Seafood.

Taylor says the best steak he’s ever had was at New York Prime in Myrtle Beach. A 16-ounce New York strip steak costs $58; a Caesar salad is $13, and a baked potato is $9.50. Don’t be surprised, though, by the city’s steeper 8% sales tax.

“You can be on the golf course, walk to the beaches, go out to eat,” says Taylor. “For a community this size, we have some of the best dining offerings you could ever ask for.’’

In a four-decade career in journalism, Eleanor O’Sullivan has reviewed many books on best practices for financial advisors, has written for Financial Advisor and the USA Today network, and was movie critic for the Asbury Park Press.