Editor’s note: This is the author’s fourth article in a six-part series for Rethinking65 on working with widows.

The second stage of widowhood, the grieving stage, can last up to a year or even two for some widows, but life continues to go on. Yet tasks she categorized as next tasks (see discussion on the Now, Next, Later Roadmap) cannot wait.

Three to six months following the death, she is still grieving and might hit a state of depression or denial where she doesn’t want to acknowledge the need for action. She might even seem distant and disengaged. Yet the clock is ticking and you, her financial advisor, can encourage her progress. Thoughtfulness and sensitivity to her concerns can help you determine how much pressure to apply. The roadmap you co-created can guide you in identifying what is next.

Life Insurance Policies

Now is the time to ask her to locate life insurance policies on her husband’s life so you can help her file claims. Although she will receive insurance proceeds, she does not need to decide how to spend or save the money right away. Explain that this decision is a later conversation requiring a solid, comprehensive plan and a responsible investment strategy.

While she could roll the funds into her bank account, it may not be federally insured if the amount is over $250,000. She could put the funds in a taxable account already open or she might need to open one. While you might want to create an investment plan to invest the money, she is not ready to absorb or evaluate your recommendations, so it is best to find a short-term solution until you can both agree on the right course of action.

Financial Strain

As you listen to her concerns, she may still be anxious about running out of money or living in poverty. While these concerns are often not relevant for affluent clients, statistical facts show widows suffer financial strain and actual financial loss upon death. Widows will see a decline in household income even if they are the primary earner. If the couple had been retired and received two Social Security checks, she will only receive one check in the future.

At the same time, many expenses such as the mortgage, utilities and maintenance will remain. Since her life expectancy is longer, a woman who is 65 needs to plan her finances so they can last at least another 21.6 years. You can help her with sophisticated planning later, but a simple analysis could assuage her fears while still grieving.

You can start working on more superficial aspects of what will later evolve into a complete comprehensive plan. The initial step in the planning process involves identifying current spending, perhaps creating a cash flow statement, and identifying available resources to create a net worth statement. These two documents are an excellent place to begin in assessing the financial strength of the current situation. The grieving widow will not be emotionally prepared to identify future goals, but this is a start to creating a plan.

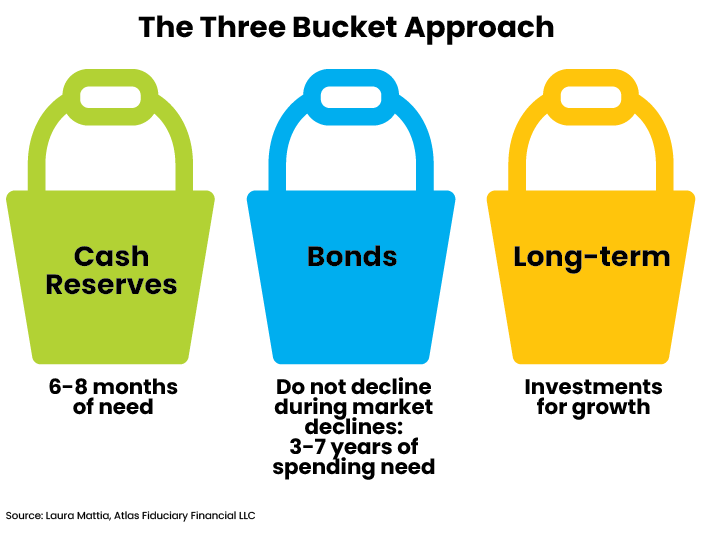

While financial advisors like to use pie charts to illustrate the asset allocation of financial assets, this might not be as comforting as using the three-bucket approach. Each bucket has a unique role and a unique purpose.

The first bucket is her cash or cash equivalents, and it includes six to eight months’ worth of living expenses. A balance of $100,000 would cover six months of living expenses and $40,000 for emergencies, always available regardless of market volatility. A balance of $300,000 invested in laddered individual bonds is another source of funds to cover her needs. And then she has another $600,000 invested in the market poised for long-term growth. Some advisors like to create a fourth bucket with $25,000 put aside to take the grandchildren to Disney World when she is feeling up to it. Reviewing the availability of her money can provide security without examining the details of the asset allocation.

Social Security, VA and Employer Benefits

The widow has two years following death to apply for the Social Security death benefit. When she feels up to it, have her call the Social Security Administration or visit the office to collect the $255 death benefit. The death benefit is a one-time payment and is different than the survivor benefits.

In addition to the death benefit, the survivor benefits allow widows age 60 or older (age 50 or older, if they are disabled) to receive a percentage of the deceased spouse’s Social Security benefits. Her benefit will be reduced permanently for each month she claims before her full retirement age. While your client may be inclined to begin receiving benefits as early as she can, you need to ensure she understands the consequences later in life.

“A widow who has a retirement benefit based on her own earnings has several options.”

A widow who has a retirement benefit based on her own earnings has several options. One option is to claim her own smaller retirement benefit at 62 and then switch to the larger survivor benefit at 66 or 67. This way she creates an income stream at 62, while increasing the size of her survivor benefit. It doesn’t make sense to wait to take the survivor benefit past full retirement age since survivor benefits do not earn delayed retirement credits. But a widow whose retirement benefit at 70 will be larger than the survivor benefit should take the survivor benefit early, perhaps at 60 or 62, and let her own benefit grow, boosted by delayed retirement credits.

Delayed retirement credits are an 8% per year increase in benefits from full retirement age to age 70. You will want to help her decide when to begin taking this benefit as part of the comprehensive plan; however, if the deceased was already collecting Social Security benefits, the widow will likely receive checks. Instruct her not to cash them since she may need to return them to the government.

If her spouse served in the military, have her contact Veteran Affairs to determine eligibility for survivor benefits. Have her contact her spouse’s employer to inquire whether he had a term life insurance policy as part of an employer-sponsored benefits package. Often spouses are unaware a policy exists. Remember, some of these tasks may seem simple, but while grieving, she is still overwhelmed and would appreciate your assistance as you make the calls with her.

As a new widow, Janice (age 62) knew deciding when to file for Social Security would have a lasting impact over her lifetime. She could file for benefits right away and receive reduced benefits or delay her benefits until she is 70 and receives 32% more than the full benefit. Janice decided to delay her benefit and instead filed for survivor benefits immediately to bridge the years to age 70, leaving her own benefits to accrue delayed credits. Not only did she receive extra needed income during the difficult transition, but she was able to strengthen her long-term position with a higher benefit for her older age.

Disclaiming Assets

If you have not talked to her estate attorney, it could be time to discuss disclaiming assets. If the widow is in a higher tax bracket and has sufficient funds, her attorney may encourage her to refuse or “disclaim” assets. She will need to decide to disclaim within nine months of the spouse’s death if that is an appropriate strategy.

Even if she has the funds, the advantages of a disclaiming approach may not make sense now because of the SECURE Act passed in 2020. The law no longer allows non-spouse IRA beneficiaries to stretch distributions over their lifetimes, which in the past delayed tax payments for decades. Instead, the law requires the money to be distributed and taxed within 10 years, creating a faster liquidation and more significant tax bills for the children.

On the other hand, the surviving spouse can still “stretch” IRA accounts resulting in a longer distribution period than the children or grandchildren. Your assistance in analyzing the family’s overall tax situation might alter the decision. Even more critical is the widow’s overall financial situation.

Your guidance on the long-term impact could reveal that giving up assets too early in widowhood might create problems later. You will need to make assumptions around her future goals, perhaps comparing various scenarios and applying probability analysis to determine if she has excess resources. You will want to feel confident the refused assets are truly surplus and there will be no regrets in the future.

Laura Mattia Ph.D., MBA, CFP, is the CEO and a senior fee-only planner with Atlas Fiduciary Financial LLC in Sarasota, Fla.