Contrary to popular belief, you cannot have it all. In business, there’s a saying in business, “You can have it good. You can have it fast. You can have it cheap. Choose any two.” When it comes to shopping for the best state for retirees, there are many considerations including, taxes, home prices, health care and estate taxes. There is no clear winner. There are tradeoffs to consider, and your clients can use your help.

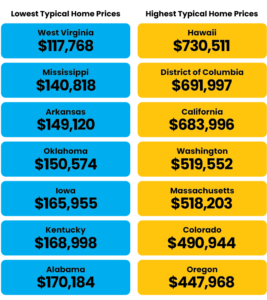

Home Prices by State

Let’s face it: Downsizing sounds great in principle, but most clients don’t want to live in a tiny space. They’d want at least a couple of bedrooms and another couple of bathrooms. According to The Ascent, a rating and review service published by The Motley Fool, the median home price in the U.S. (2Q2021) is $374,900. The Ascent report also looks at the typical home prices (not averages) in particular areas based on the Zillow Home Value Index. The chart below shows the seven states with lowest and highest typical values based on the ZHVI. Nationwide, the typical value is $293,349.

How does this influence decisions?

The logical approach: If a client can sell a larger home in an area with high home prices and relocate to an area where they can find a great, smaller house with one floor living, they will have freed up lots of equity. These funds (after paying applicable taxes) could be reinvested to produce retirement income.

The contrarian approach: The reality, though, is your client might move to a state with higher home prices in order to be close to their grown children. It’s good to be close to family. Senior living communities for “over 65s” are also springing up everywhere. Although average home prices might be high, an apartment or garden townhouse might make sense, especially if the area has quality medical care nearby.

Who made the move? A local retired couple in our part of Pennsylvania chose to relocate to a retirement community in Georgia. Proximity to family was a factor, but the decision involved real estate prices too. Part of the carrying costs of a house are the local property taxes and school taxes. They found a county with a valuable tax break for seniors: Homeowners over a certain age who don’t have children in the local school system are exempt from paying school taxes. That can be a substantial savings.

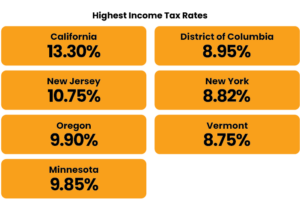

Income Tax Rates by State

That last chart was eye opening. Your clients figure they are good home shoppers who can find a good deal if they look hard enough. But they should also be paying attention to state income taxes, which could be a great leveling factor. The Tax Foundation is a good resource.

The logical place to start is the eight states with no income taxes and to avoid the states with the highest income taxes. When looking at the highest rates, let’s look at the marginal tax bracket in the next chart.

Your clients might also want to consider which states don’t tax Social Security income — obviously the eight states listed above with no state income tax. However, 24 states in total don’t tax Social Security. Here’s the full list.

Logical approach: Robert Kiyosaki, an American businessman and author, said, “It’s not how much money you make, but how much money you keep.” It’s part of a longer quote, and we’ll get to more of it later. Ideally, your clients will want to live in a state that lets them keep as much of their retirement income as they generate. You know the federal government is going to have its hand out as your clients take retirement plan distributions. Help them find a state that wants retirees living there and has designed its tax rates accordingly.

Contrarian approach: Suppose very little of your client’s income is earned income and their living expenses are covered by gradually liquidating their investment portfolio and taking long-term capital gains? A state with higher income taxes might not be bad if their tax exposure is small.

Who made the move? We knew a couple living on the Virginia side of Washington D.C. They chose to relocate to the area outside Nashville, Tenn. The absence of income taxes can be a powerful draw.

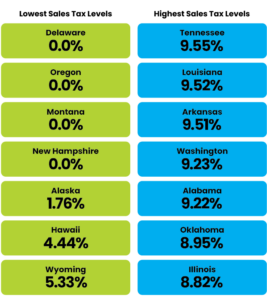

Sales Tax Rates by State

Sales tax can also be a consideration and, once again, the Tax Foundation comes to the rescue.

Logical approach: Sales tax is a consumption tax. It taxes what you spend, not what you earn. Most states don’t tax the essentials of life like groceries: Consumers are taxed when they eat out, but not when they prepare food at home. Some taxes are built into the product price. A good example is the taxes on gasoline. The federal government has an excise tax of 18.4 cents/gallon on gasoline and 24.4 cents/gallon on diesel. States then apply their own taxes. Pennsylvania adds about 58 cents/gallon. Arizona is down around 19 cents/gallon. This means the gallon of gas that costs about $3.30 at the pump in Pennsylvania includes about 76 cents in tax! Put another way, that’s about 30% in tax on top of the pre-tax price.

Contrarian approach: Perhaps your clients live simply, prepare meals at home and don’t shop a lot. Sales taxes shouldn’t greatly affect their decision where to live that much.

Who made the move? A financial advisor I knew in the Princeton, N.J., area decided to move his primary residence to his Florida property. More intriguing, he decided to focus his business on a specific niche market: Northern residents seeking to establish residency in an area with both a lower cost of living and lower taxes.

Cost of Healthcare

Healthcare has been one of the fastest rising costs. It has exceeded the rate of inflation for years. Which states have the highest and lowest average costs for health insurance? This research comes from ValuePenguin and looks at monthly costs for a 40-year-old by state. As a baseline, the national average they quote for 2022 is $541/month.

Logical approach: This is a major factor. Generally speaking, these costs don’t go down. They just get bigger and bigger. You might be living on a fixed income, while healthcare costs gallop ahead. You want to live in a state where these expenses are much lower.

Contrarian approach: If you have a good insurance agent who is proactive, they can shop around for good Medicare supplemental and drug plans.

Who made this move? One of our friends is a New York City-based financial advisor transitioning into retirement. He and his wife decided to buy a house in Virginia, near a university with a medical school. The move helps them get away from the high healthcare costs of New York, yet they’re only a short distance from high-quality healthcare.

Quality of Healthcare by State

Healthcare is a big expense, but regardless of cost, if you need it, you want it to be good. The chart below shows how U.S. News & World Report ranked healthcare by quality.

Logical approach: Years ago, UBS published a report that discussed the three stages of retirement. In the final stage, UBS assumed a retiree is likely to contract an illness that ultimately proves fatal. People thinking about this final stage may accept living in a place with high medical costs if they know they can get first-rate medical care when they need it. This implies living in a high tax state in the Northeast because the area has many of the best hospitals.

Contrarian approach: Even if a state ranks low in the healthcare tables, there’s usually good medical care available somewhere! The medical schools usually have a teaching hospital. The state capitol or the largest city usually has a substantial medical facility. If you choose to live in a state with a lower cost of living, try to live near a city with a major hospital.

Who made the move? Years ago, I had clients who live full time in St. Maarten in the Caribbean. It was a great life, but as the couple got older, they moved to a brownstone in Brooklyn, N.Y. The reason was the wife developed medical issues. The quality of specialist doctors and healthcare was far better in New York City compared to the Caribbean.

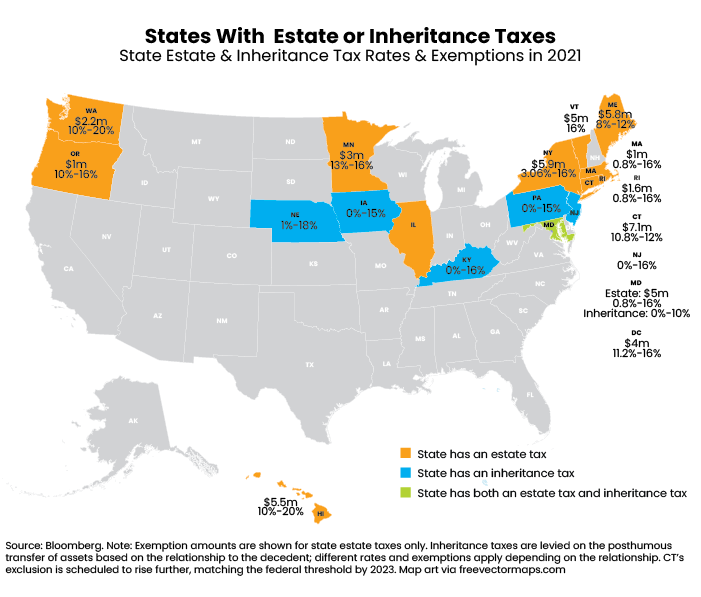

Estate Taxes at the State Level

Let’s look at one final category. Most estates are not subject to federal estate taxes. (The federal exemption is rising to $12.06 million for individuals and $24.12 million for married couples in 2022.) But some states do have estate and inheritance taxes, with Maryland the only state that has both.

Logical approach: Your client has money and expects to be making lots more. Let’s get back to Robert Kiyosaki’s quote. He’s the guy who said, “It’s not how much money you make, but how much money you keep.” That’s only half the quote. Here’s the rest of what he says matters: “How hard it works for you and how many generations you keep it for.”

The working hard part isn’t difficult to address. Clients can find good financial advisors, CPAs and financial planners in every state. “How many generations you keep it for” requires minimizing estate taxes. That’s difficult, because it’s a moving target. The federal and state governments can change the rules. In addition to planning, the most someone can probably do is avoid the high estate tax states and settle in the states with no or low estate taxes.

Contrarian approach: If your clients feel their retirement assets will carry them through retirement and they will only leave a small residual, then estate taxes aren’t a big concern.

Who made this move: Friends of ours who are active in the local community own homes in several states. They added another, in Wyoming. The tax treatment both during their lifetimes and beyond made it the sensible choice.

Conclusion

The choice of where your clients (and you) decide to retire depends on many factors. Placing them in priority order is the prudent way to make a decision. Talk with friends. Think about fellow retirees and where they ultimately settled. You will tend to find Florida, North Carolina and Arizona are common destinations.

Bryce Sanders is president of Perceptive Business Solutions Inc. He provides HNW client acquisition training for the financial services industry. His book, “Captivating the Wealthy Investor” is available on Amazon.